|

市場調査レポート

商品コード

1721524

AIガバナンス市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測AI Governance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| AIガバナンス市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月11日

発行: Global Market Insights Inc.

ページ情報: 英文 172 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

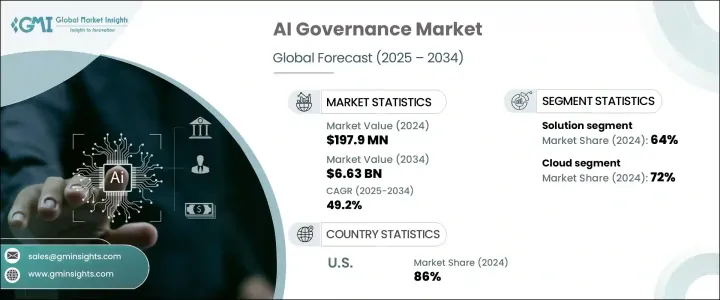

AIガバナンスの世界市場規模は、2024年に1億9,790万米ドルとなり、CAGR 49.2%で成長し、2034年には66億3,000万米ドルに達すると予測されています。

さまざまな分野で人工知能が急速に導入される中、企業は機密データの保護やAIを活用したシステムの管理維持といった課題の増加に直面しています。AIが中核的なビジネス機能に影響を与え続ける中、データの誤用、モデルの偏り、不正アクセスなどのリスクから保護するためのガバナンスフレームワークの必要性がより急務となっています。AIガバナンスは、倫理基準の遵守、透明性の維持、インテリジェントシステム全体における責任ある意思決定の実現において、極めて重要な役割を果たします。

AI主導のツールは、不正検知や自動脅威分析などのアプリケーションを通じてデジタル・インフラの安全確保に役立つ一方で、その複雑性の増大により厳格な監視が求められています。規制の隙間や倫理違反の可能性は、積極的に対処しなければならない脆弱性を生み出します。AIシステムの完全性に対する懸念が高まる中、企業はリスクを検出するだけでなく、アルゴリズムのパフォーマンス、バイアスの緩和、データの正確性に関するリアルタイムの洞察を提供できるガバナンス・ソリューションを導入することの重要性を認識しつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億9,790万米ドル |

| 予測金額 | 66億3,000万米ドル |

| CAGR | 49.2% |

高度なサイバー攻撃が増加し、多くの場合、国家主体によって支援されているため、強固なAIガバナンス構造を実装する緊急性が高まっています。また、組織はAIを活用した侵入テストを開始し、実際の攻撃をシミュレートして内部の弱点を検出するようになっています。しかし、強固なガバナンス・プロトコルがなければ、こうした高度な防御戦略には偏りやコンプライアンス・エラーが生じるリスクがあります。AIガバナンスは、倫理、説明責任、アカウンタビリティといったサイバーセキュリティの中核となる原則との整合性を確保し、組織がAIの導入において可視性と制御性を維持できるよう支援します。

市場セグメンテーションでは、コンポーネントはソリューションとサービスに分けられます。2024年には、ソリューションセグメントが市場をリードし、世界シェアの約64%を占め、予測期間を通じて48%以上のCAGRで成長するとみられています。これらのプラットフォームは、ポリシーの策定、実施、監視を統合し、AIシステムを効率的に管理するための一元的なフレームワークを提供します。また、高度な解釈可能性ツールを使用して、トレーニングデータとアルゴリズムのバイアスの検出と削減をサポートします。これらのソリューションは、AIが生成したアウトプットを開発者と監査人の両方にとって理解しやすく、追跡可能にするよう設計された技術を通じて、説明可能性を重視しています。

導入に関しては、AIガバナンス市場はクラウド型とオンプレミス型に区分されます。2024年には、クラウドセグメントが市場の約72%を占め、2025年から2034年にかけて49.5%以上のCAGRを記録すると予測されています。クラウドホスト型プラットフォームが好まれるようになったのは、その拡張性、アクセス性、既存のワークフローへの統合のしやすさに起因しています。クラウドベースのAIガバナンスツールは、コンプライアンス・タスクの自動化、リアルタイムのポリシー実施、AIモニタリングの合理化に役立ちます。また、クラウドプロバイダーは、機密性の高いAIデータを外部の脅威から保護するために、暗号化、アクセス制御、ID管理などの堅牢なセキュリティ機能を提供しています。

組織規模別では、市場は大企業と中小企業に分類されます。大企業は、多様な業務部門に幅広くAIを導入しているため、2024年にはこの分野を支配しています。これらの企業は通常、社内外の枠組みにおける統合、コンプライアンス、説明責任を監督する専任のAIガバナンスチームに投資しています。彼らは、倫理的なAIの実践を標準化する上で極めて重要な役割を果たし、システムが責任を持って展開され、世界な規制の指令に沿ったものであることを保証します。パフォーマンス監視からリスク軽減に至るまで、大企業はAI導入全体の整合性を維持するためのガバナンス構造に依存しています。

地域別では、北米が2024年の主要市場として浮上し、米国だけで約7,500万米ドルの貢献があり、北米シェアの約86%を占めています。この地域の成長は、進化する規制フレームワークとAI倫理に対する一般市民の意識に支えられ、業界全体でAI導入が増加したことが主な要因です。この地域の企業は、透明性、監査機能、国内外の基準への準拠を優先するガバナンス・ツールに多額の投資を行っています。

AIガバナンスランドスケープを形成する主要企業には、キャップジェミニ、IBM、アルファベット、Meta Platforms、NTTデータ、マイクロソフト、オラクル、SAP、パランティア・テクノロジーズ、SASインスティテュートなどがあります。これらのベンダーは、AIモデル監視の自動化、MLOpsへのガバナンスの統合、セクター固有のコンプライアンスニーズに合わせたフレームワークの開発に注力しています。また、規制当局と協力し、世界市場で倫理的かつ責任あるAIの利用をサポートするガバナンスモデルを共同開発しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- プラットフォームプロバイダー

- ソフトウェアプロバイダー

- サービスプロバイダー

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界的にサイバーセキュリティイベントの発生率が高め

- 倫理的なハッキングと侵入テストへの関心の高まり

- データセキュリティとプライバシーに関する懸念の高まり

- 倫理的なAIとIoT技術の統合

- 業界の潜在的リスク&課題

- 高い実装コストとリソース要件

- 標準化されたAIガバナンスフレームワークの欠如

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソリューション

- プラットフォーム

- ソフトウェアツール

- サービス

- コンサルティング

- 統合

- サポートとメンテナンス

第6章 市場推計・予測:展開モード別、2021-2034

- 主要動向

- クラウド

- オンプレミス

第7章 市場推計・予測:組織規模別、2021-2034

- 主要動向

- 大企業

- 中小企業

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- BFSI

- 政府と防衛

- ヘルスケアとライフサイエンス

- メディア&エンターテイメント

- IT・通信

- 自動車

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Alphabet

- BigID

- Capgemini

- Dataiku

- Deloitte

- EY(Ernst &Young)

- FICO

- H2O.ai

- IBM

- KPMG

- Meta Platforms

- Microsoft

- NTT DATA

- Oracle

- Palantir Technologies

- PWC

- SAP

- SAS Institute

- Stefanini

- Teradata

The Global AI Governance Market was valued at USD 197.9 million in 2024 and is estimated to grow at a CAGR of 49.2% to reach USD 6.63 billion by 2034. With the rapid adoption of artificial intelligence across various sectors, organizations are facing increasing challenges in protecting sensitive data and maintaining control over AI-powered systems. As AI continues to influence core business functions, the need for governance frameworks becomes more urgent to safeguard against risks such as data misuse, model bias, and unauthorized access. AI governance plays a crucial role in ensuring compliance with ethical standards, maintaining transparency, and enabling responsible decision-making across intelligent systems.

While AI-driven tools help secure digital infrastructures through applications like fraud detection and automated threat analysis, their growing complexity demands rigorous oversight. Regulatory gaps and the potential for ethical breaches create vulnerabilities that must be addressed proactively. With mounting concerns over the integrity of AI systems, businesses are recognizing the importance of deploying governance solutions that can not only detect risks but also provide real-time insights into algorithm performance, bias mitigation, and data accuracy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $197.9 Million |

| Forecast Value | $6.63 Billion |

| CAGR | 49.2% |

The increase in sophisticated cyberattacks, often backed by state actors, has amplified the urgency to implement strong AI governance structures. Organizations are also beginning to leverage AI-enabled penetration testing, simulating real-world attacks to detect internal weaknesses. However, without solid governance protocols, these advanced defense strategies risk introducing bias and compliance errors. AI governance ensures alignment with core cybersecurity principles like ethics, explainability, and accountability, helping organizations maintain visibility and control in AI deployments.

In terms of market segmentation, the component landscape is divided into solutions and services. In 2024, the solution segment led the market, accounting for nearly 64% of the global share, and is set to grow at over 48% CAGR through the forecast period. These platforms integrate policy formulation, implementation, and monitoring, offering a centralized framework for managing AI systems effectively. They also support the detection and reduction of bias in training data and algorithms using advanced interpretability tools. These solutions emphasize explainability through technologies designed to make AI-generated outputs understandable and traceable for both developers and auditors.

When it comes to deployment, the AI governance market is segmented into cloud and on-premises models. In 2024, the cloud segment captured approximately 72% of the market and is projected to register a CAGR of over 49.5% between 2025 and 2034. The growing preference for cloud-hosted platforms stems from their scalability, accessibility, and ease of integration into existing workflows. Cloud-based AI governance tools help automate compliance tasks, enable real-time policy enforcement, and streamline AI monitoring efforts. Cloud providers also offer robust security features, including encryption, access controls, and identity management to protect sensitive AI data from external threats.

By organization size, the market is classified into large enterprises and SMEs. Large enterprises dominated the space in 2024 due to their broader AI adoption across diverse operational units. These businesses typically invest in dedicated AI governance teams that oversee integration, compliance, and accountability within internal and external frameworks. They play a pivotal role in standardizing ethical AI practices, ensuring systems are deployed responsibly and aligned with global regulatory mandates. From performance monitoring to risk mitigation, large organizations rely on governance structures to maintain integrity across AI deployments.

Regionally, North America emerged as a leading market in 2024, with the United States alone contributing nearly USD 75 million, representing around 86% of the North American share. The regional growth is largely driven by increased AI deployment across industries, supported by evolving regulatory frameworks and public awareness of AI ethics. Businesses in this region are investing heavily in governance tools that prioritize transparency, auditing capabilities, and compliance with local and international standards.

Key companies shaping the AI governance landscape include Capgemini, IBM, Alphabet, Meta Platforms, NTT DATA, Microsoft, Oracle, SAP, Palantir Technologies, and SAS Institute. These vendors are focusing on automating AI model oversight, integrating governance into MLOps, and developing tailored frameworks to match sector-specific compliance needs. They are also collaborating with regulatory authorities to co-create governance models that support ethical and responsible AI use across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Platform providers

- 3.2.2 Software providers

- 3.2.3 Service providers

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 High rate of cybersecurity events globally

- 3.8.1.2 Proliferating interest towards ethical hacking and penetration testing

- 3.8.1.3 Growing data security and privacy concerns

- 3.8.1.4 Integration of ethical AI and IoT technology

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High implementation costs & resource requirements

- 3.8.2.2 Lack of standardized AI governance frameworks

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Platform

- 5.2.2 Software tools

- 5.3 Service

- 5.3.1 Consulting

- 5.3.2 Integration

- 5.3.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprise

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Government & defense

- 8.4 Healthcare & life sciences

- 8.5 Media & entertainment

- 8.6 IT & telecommunication

- 8.7 Automotive

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alphabet

- 10.2 BigID

- 10.3 Capgemini

- 10.4 Dataiku

- 10.5 Deloitte

- 10.6 EY (Ernst & Young)

- 10.7 FICO

- 10.8 H2O.ai

- 10.9 IBM

- 10.10 KPMG

- 10.11 Meta Platforms

- 10.12 Microsoft

- 10.13 NTT DATA

- 10.14 Oracle

- 10.15 Palantir Technologies

- 10.16 PWC

- 10.17 SAP

- 10.18 SAS Institute

- 10.19 Stefanini

- 10.20 Teradata