|

市場調査レポート

商品コード

1716513

住宅用低電圧開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Low Voltage Residential Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 住宅用低電圧開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

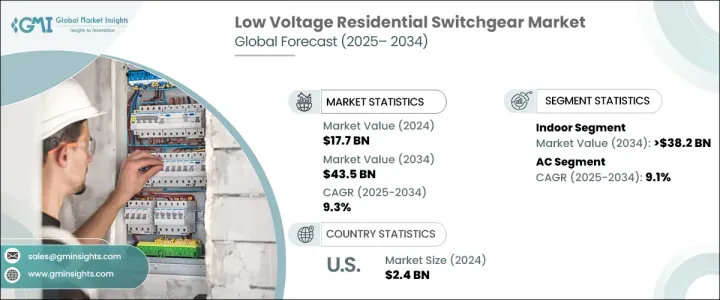

住宅用低電圧開閉装置の世界市場規模は2024年に177億米ドルとなり、2025年から2034年にかけてCAGR 9.3%で成長すると予測されています。

同市場は、急速な都市化、電力消費の増加、スマートホーム技術の普及により、着実な成長を遂げています。世界中で生活水準が向上するにつれて、住宅建設活動は増加傾向にあり、効率的で信頼性が高く安全な配電システムへの需要が高まっています。特に新興経済諸国では都市の拡大が著しく、住宅インフラにおける低圧配電盤のニーズが高まっています。IoT対応システムやエネルギー効率の高いソリューションを備えたスマートホームに対する消費者の嗜好が高まっていることも、需要をさらに後押ししています。

リアルタイムの監視、自動制御、安全性の強化を提供するスマート・スイッチギアは、最新の住宅用電気設備に不可欠な要素になりつつあります。さらに、持続可能性と省エネルギーへの注目の高まりが、家庭でのスマート電力管理システムの採用率上昇につながり、市場規模の拡大に寄与しています。再生可能エネルギーの利用や省エネルギーを推進する政府の取り組みも、市場成長の推進に重要な役割を果たしています。消費者がより安全で効率的なソリューションを求める中、先進的な住宅用低電圧開閉装置の需要は増加の一途をたどっており、長期的な市場拡大を確実なものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 177億米ドル |

| 予測金額 | 435億米ドル |

| CAGR | 9.3% |

屋内分野は、スマートホーム技術やエネルギー効率の高い電気システムの採用が増加していることから、2034年までに382億米ドルの売上が見込まれています。IoT対応の屋内スイッチギヤに対する需要の高まりは、エネルギー管理に対する消費者の意識の高まりと、住宅空間における安全性と自動化の強化の必要性によって後押しされています。省エネルギーを支援し、発電における再生可能エネルギー源の利用を促進する政府の規制は、このセグメントの成長をさらに加速させています。コンパクトな設計、通信機能の向上、安全機構の強化といった高度な機能により、最新の屋内用開閉器は公益事業、商業、住宅用途で好まれています。

交流セグメントの住宅用低電圧開閉装置市場は、2034年までCAGR 9.1%で成長すると予測されます。長距離送電の効率性から、配電と送電において交流(AC)電力が引き続き優位を占めていることが、この成長を後押ししています。欧州では、送電におけるギャップの特定と対処を目的としたインフラ評価が進行中であり、市場に新たな機会を生み出しています。住宅環境では、信頼性が高く効率的な電気システムに対するニーズが高まっており、シームレスな配電を確保し、混乱を最小限に抑える高度な開閉器ソリューションに対する需要が高まっています。

米国の住宅用低電圧開閉装置市場は、2024年に24億米ドルを創出しました。エアコンや電気暖房機など、エネルギー集約型の家電製品の使用が増加していることが、より高度なACベースのスイッチギヤの必要性を高めています。家庭におけるスマート機器や自動化システムの普及が進むにつれて、回路保護、過負荷管理、電圧制御が重視されるようになっています。住宅での電力消費が増加し続ける中、市場は運用効率を高め、家庭用電気システムの安全性を確保するインテリジェントで適応性の高いスイッチギアシステムへとシフトしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:設置別、2021年~2034年

- 主要動向

- 屋内

- 屋外

第6章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- CHINT Group

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

The Global Low Voltage Residential Switchgear Market was valued at USD 17.7 billion in 2024 and is projected to grow at a CAGR of 9.3% between 2025 and 2034. The market is witnessing steady growth due to rapid urbanization, increasing electricity consumption, and the widespread integration of smart home technologies. As living standards improve worldwide, residential construction activity is on the rise, driving the demand for efficient, reliable, and safe electrical distribution systems. Developing economies, in particular, are experiencing significant urban expansion, leading to a growing need for low voltage switchgear in residential infrastructures. The growing consumer preference for smart homes equipped with IoT-enabled systems and energy-efficient solutions is further fueling the demand.

Smart switchgear, offering real-time monitoring, automated control, and enhanced safety, is becoming an essential component of modern residential electrical setups. Additionally, the increasing focus on sustainability and energy conservation has led to higher adoption of smart power management systems in households, contributing to the expanding market size. Government initiatives promoting the use of renewable energy and energy-saving practices are also playing a crucial role in driving market growth. As consumers seek safer and more efficient solutions, the demand for advanced low voltage residential switchgear continues to rise, ensuring long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.7 Billion |

| Forecast Value | $43.5 Billion |

| CAGR | 9.3% |

The indoor segment is expected to generate USD 38.2 billion by 2034, driven by the increasing adoption of smart home technologies and energy-efficient electrical systems. The rising demand for IoT-enabled indoor switchgear is being fueled by growing consumer awareness about energy management and the need for enhanced safety and automation in residential spaces. Government regulations supporting energy conservation and promoting the use of renewable energy sources in power generation are further accelerating the growth of this segment. Advanced features such as compact designs, improved communication capabilities, and enhanced safety mechanisms make modern indoor switchgear a preferred choice for utility, commercial, and residential applications.

The low voltage residential switchgear market in the AC segment is projected to grow at a 9.1% CAGR through 2034. The continued dominance of alternating current (AC) power in electricity distribution and transmission, owing to its efficiency in long-distance power transfer, is fueling this growth. In Europe, ongoing infrastructure assessments aimed at identifying and addressing gaps in electricity transmission are creating new opportunities for the market. The rising need for reliable and efficient electrical systems in residential settings is propelling the demand for advanced switchgear solutions that ensure seamless power distribution and minimize disruptions.

The U.S. low voltage residential switchgear market generated USD 2.4 billion in 2024. The increasing use of energy-intensive household appliances, including air conditioners and electric heating units, is driving the need for more sophisticated AC-based switchgear. With the rising prevalence of smart devices and automated systems in homes, there is a growing emphasis on circuit protection, overload management, and voltage control. As residential power consumption continues to increase, the market is shifting towards intelligent and adaptive switchgear systems that enhance operational efficiency and ensure the safety of household electrical systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Installation 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Indoor

- 5.3 Outdoor

Chapter 6 Market Size and Forecast, By Current 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Bharat Heavy Electricals

- 8.3 CG Power and Industrial Solutions

- 8.4 CHINT Group

- 8.5 Eaton

- 8.6 Fuji Electric

- 8.7 General Electric

- 8.8 HD Hyundai Electric

- 8.9 Hitachi

- 8.10 Hyosung Heavy Industries

- 8.11 Lucy Group

- 8.12 Mitsubishi Electric

- 8.13 Ormazabal

- 8.14 Schneider Electric

- 8.15 Siemens

- 8.16 Skema

- 8.17 Toshiba