|

市場調査レポート

商品コード

1708241

自動車用サーマルシステム向けポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Pump for Thermal System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用サーマルシステム向けポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 181 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

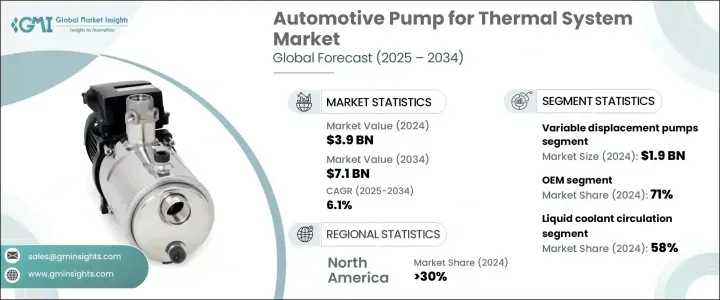

自動車用サーマルシステム向けポンプの世界市場は2024年に39億米ドルと評価され、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。

自動車産業が電気自動車(EV)やハイブリッド電気自動車(HEV)にシフトするにつれ、効率的な熱管理システムの需要が高まっています。これらのシステムは、EVの性能に不可欠なバッテリーやパワーエレクトロニクスなど、さまざまな車両部品の温度を最適に保つために極めて重要です。これらのサーマル・システムは、温度の安定性を維持することで自動車の機能性とバッテリーの寿命を向上させるのに役立つため、高度な冷却ソリューションの需要が伸びています。

この市場を牽引する重要な要因は、エンジンや排気システムから発生する廃熱を回収するための熱エネルギー回収システム(TERS)の台頭です。これらのシステムは全体的なエネルギー効率を向上させ、自動車用ポンプの需要をさらに押し上げます。これらのポンプは、冷却水をシステム内で循環させたり、加熱された液体エネルギーを伝達して補助機能を作動させたり、走行性能を高めたりすることで、重要な役割を果たしています。これらのポンプは、EVやHEVを含む最新の自動車の開発に不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 6.1% |

同市場はポンプの種類によって区分され、遠心ポンプ、容積式ポンプ、可変容量ポンプが主なカテゴリーです。可変容量ポンプは、2024年に市場の19億米ドルを占め、予測期間中に大きな成長が見込まれています。これらのポンプは、複雑な熱システムにおける柔軟性と応答性の高さで好まれ、高性能運転や寒冷地や交通量の多い状況など、さまざまな運転条件下でより優れた制御を提供します。

同市場はまた、販売チャネル別にOEMセグメントとアフターマーケットセグメントに分けられます。2024年には、OEMセグメントが71%と圧倒的な市場シェアを占めています。OEMは、交換部品やアフターマーケット用ポンプを流通させるために、eコマースを含む消費者直販プラットフォームを利用しています。このアプローチは、市場へのリーチを向上させるだけでなく、顧客サポートとフィードバックを強化します。

冷媒タイプ別では、市場は油性冷媒、液体冷媒循環式冷媒、空気式冷媒に区分されます。2024年には、電気自動車やハイブリッド車における効率的なバッテリー温度管理に対する需要の高まりにより、液体クーラント循環セグメントが58%と大半のシェアを占めています。

自動車用サーマルシステム向けポンプ市場はさらに推進力タイプ別に分類され、2024年には内燃(IC)エンジン分野が最大のシェアを占める。熱管理はターボチャージャーエンジンにおいて特に重要であり、オーバーヒートを防ぎ性能を長持ちさせるためには効果的な冷却システムが必要となります。

北米では米国が市場を独占し、同地域は2024年の世界市場シェアの30%以上を占めています。EVにおける熱管理システムの需要は、バッテリー技術の進歩やエネルギー効率の高い自動車の推進により増加しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品サプライヤー

- ポンプ組立業者

- サービスプロバイダー

- 技術プロバイダー

- 最終用途

- 利益率分析

- コスト内訳分析

- テクノロジーとイノベーションの展望

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 電気自動車とハイブリッド車の需要増加

- 熱エネルギー回収システムの採用拡大

- アフターマーケットと買い替え需要の拡大

- 自律走行車とコネクテッドカーの成長

- 業界の潜在的リスク&課題

- 高度なポンプ技術の高コスト

- 先進サーマルポンプの改造の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ポンプ別、2021年~2034年

- 主要動向

- 渦巻きポンプ

- 電動ウォーターポンプ

- 機械式ウォーターポンプ

- 容積式ポンプ

- 歯車ポンプ

- ベーンポンプ

- ピストンポンプ

- スクリューポンプ

- 可変容量ポンプ

第6章 市場推計・予測:ワット別、2021年~2034年

- 主要動向

- 50W未満

- 50W-100W

- 100W-500W

- 500W以上

第7章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ICE

- BEV

- PHEV

- HEV

第8章 市場推計・予測:冷媒別、2021年~2034年

- 主要動向

- オイルベース

- 液体クーラント循環(LCC)

- 空気ベース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aisin

- BorgWarner

- Bosch(Robert Bosch)

- Continental

- Denso

- Eberspaecher

- Fluid-o-Tech

- Grayson

- Hanon Systems

- Hitachi Astemo

- Infineon Technologies

- Johnson Electric Holdings Limited

- MAHLE

- Marelli

- Modine

- Nidec Corporation

- Rheinmetall AG

- Schaeffler

- Valeo

- ZF

The Global Automotive Pump for Thermal System Market, valued at USD 3.9 billion in 2024, is projected to grow at a CAGR of 6.1% from 2025 to 2034. As the automotive industry shifts towards electric vehicles (EVs) and hybrid electric vehicles (HEVs), the demand for efficient thermal management systems is rising. These systems are crucial for maintaining optimal temperatures in various vehicle components, including batteries and power electronics, which are critical to EV performance. The demand for advanced cooling solutions is growing as these thermal systems help enhance vehicle functionality and battery life by maintaining temperature stability.

A significant factor driving this market is the rise of thermal energy recovery systems (TERS), which are used to capture waste heat produced by engine or exhaust systems. These systems improve overall energy efficiency and further boost the demand for automotive pumps. These pumps play a vital role by circulating coolant through the system, transferring heated liquid energy to operate auxiliary features, or enhancing driving performance. They are essential in the development of modern vehicles, including EVs and HEVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6.1% |

The market is segmented based on pump type, with centrifugal pumps, positive displacement pumps, and variable displacement pumps being the main categories. Variable displacement pumps accounted for USD 1.9 billion of the market in 2024 and are expected to show significant growth over the forecast period. These pumps are preferred for their flexibility and responsiveness in complex thermal systems, where they provide better control under varying driving conditions, such as high-performance driving or in cold weather and heavy traffic situations.

The market is also divided by sales channel into OEM and aftermarket segments. In 2024, the OEM segment held a dominant market share of 71%. OEMs use direct-to-consumer platforms, including e-commerce, to distribute replacement parts and aftermarket pumps. This approach not only improves their market reach but also enhances customer support and feedback.

By refrigerant type, the market is segmented into oil-based, liquid coolant circulation, and air-based refrigerants. The liquid coolant circulation segment held a majority share of 58% in 2024, driven by the growing demand for efficient battery temperature management in electric and hybrid vehicles.

The automotive pump for thermal system market is further categorized by propulsion type, with the internal combustion (IC) engine segment holding the largest share in 2024. Thermal management is particularly crucial in turbocharged engines, where effective cooling systems are required to prevent overheating and ensure long-lasting performance.

In North America, the market was dominated by the U.S., with the region accounting for over 30% of the global market share in 2024. The demand for thermal management systems in EVs is increasing due to advancements in battery technology and the push for more energy-efficient vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Pump assemblers

- 3.2.4 Service provider

- 3.2.5 Technology provider

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for electric and hybrid vehicles

- 3.8.1.2 Growing adoption of thermal energy recovery systems

- 3.8.1.3 Expansion of aftermarket and replacement demand

- 3.8.1.4 Growth of autonomous and connected vehicles

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced pump technologies

- 3.8.2.2 Complexity in retrofitting advanced thermal pumps

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Centrifugal pumps

- 5.2.1 Electric water pump

- 5.2.2 Mechanical water pump

- 5.3 Positive displacement pumps

- 5.3.1 Gear pump

- 5.3.2 Vane pump

- 5.3.3 Piston pump

- 5.3.4 Screw pump

- 5.4 Variable displacement pumps

Chapter 6 Market Estimates & Forecast, By Watt, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Below 50 W

- 6.3 50W – 100W

- 6.4 100W – 500W

- 6.5 Above 500W

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 BEV

- 7.4 PHEV

- 7.5 HEV

Chapter 8 Market Estimates & Forecast, By Refrigerant, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 Oil-based

- 8.3 Liquid Coolant Circulation (LCC)

- 8.4 Air-based

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 BorgWarner

- 10.3 Bosch (Robert Bosch)

- 10.4 Continental

- 10.5 Denso

- 10.6 Eberspaecher

- 10.7 Fluid-o-Tech

- 10.8 Grayson

- 10.9 Hanon Systems

- 10.10 Hitachi Astemo

- 10.11 Infineon Technologies

- 10.12 Johnson Electric Holdings Limited

- 10.13 MAHLE

- 10.14 Marelli

- 10.15 Modine

- 10.16 Nidec Corporation

- 10.17 Rheinmetall AG

- 10.18 Schaeffler

- 10.19 Valeo

- 10.20 ZF