|

市場調査レポート

商品コード

1708219

ティーパッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Tea Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ティーパッケージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月25日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

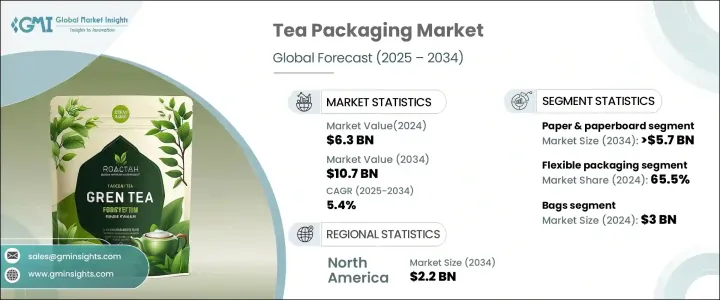

世界のティーパッケージング市場は2024年に63億米ドルとなり、2025年から2034年にかけてCAGR 5.4%で成長すると予測されています。

この成長には、世界の茶消費の増加、レディ・トゥ・ドリンクの選択肢の急速な拡大、高級茶製品に対する需要の増加が寄与しています。茶は依然として世界で2番目に多く消費されている飲料であるため、包装メーカーは費用対効果を維持しながら鮮度と香りを保つ革新的で高品質なソリューションの開発を常に迫られています。現代の茶消費者は持続可能性を優先しており、生分解性素材やリサイクル可能な素材を使用したパッケージへのニーズが高まっています。こうした環境嗜好に沿ったブランドは、環境に優しいパッケージング・ソリューションを採用することで競争力を高めています。

さらに、オーガニックティーやスペシャルティーティーの人気の高まりは、製品の高品質な性質を反映したプレミアムパッケージングへの需要を加速させています。リシーラブルオプション、湿気バリア、光保護を組み込んだパッケージデザインは、製品の寿命を保証し、消費者の体験を向上させる標準機能となりつつあります。世界の茶消費動向がより健康的なライフスタイルを志向し、特殊飲料への関心が高まるにつれ、先進的で持続可能なパッケージングソリューションへのニーズが市場の大幅な成長を促進すると予想されます。さらに、eコマースの台頭により、製品の完全性を維持しながら輸送の厳しさに耐えることができる、頑丈で魅力的かつ機能的な包装のニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 63億米ドル |

| 予測金額 | 107億米ドル |

| CAGR | 5.4% |

ティーパッケージング市場は、プラスチック、紙・板紙、金属、その他を含む素材別に分類されます。紙・板紙部門は、生分解性でリサイクル可能なパッケージへの嗜好の高まりにより、2034年までに57億米ドルを創出すると予測されています。多くの紅茶ブランドは、その軽量性、堆肥化可能性、リサイクル可能性から、紙ベースの包装にシフトしています。プレミアムブランドやスペシャルティブランドもまた、環境に優しいブランドイメージに沿い、持続可能な慣行に対する消費者の期待に応えるため、細工された板紙カートンを採用しています。環境への影響に対する消費者の意識が高まる中、堆肥化可能で再利用可能な包装オプションを提供するブランドは、顧客ロイヤルティと市場での差別化を高めています。

フレキシブル包装は、その軽量性、費用対効果、茶葉の鮮度を保つ優れた能力により、2024年の市場シェアは65.5%と圧倒的です。ラミネートフィルム、パウチ、リシーラブルバッグで作られることが多いこのタイプの包装は、湿気、酸素、光に対して卓越した保護を提供し、茶葉が長期間品質を維持することを保証します。利便性と賞味期限の延長に対する需要が高まるにつれ、特にレディ・トゥ・ドリンクや特殊な茶向けに、フレキシブルなパッケージングソリューションの人気が高まっています。

北米のティーパッケージング市場は、プレミアムティーやオーガニックティー製品の人気の高まりと、持続可能なパッケージングソリューションの重視の高まりに後押しされ、2034年までに22億米ドルに達すると予想されています。米国市場だけを見ても、茶の消費量の増加、高級オーガニック製品へのシフト、環境に配慮した包装への嗜好の高まりによって、2034年には19億米ドルに成長すると予測されています。消費者が鮮度と信頼性を維持したスペシャルティ茶を求める中、製品の品質を効果的に保つパッケージング・ソリューションへのニーズはかつてないほど高まっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 茶消費量の増加

- 持続可能な包装への需要の高まり

- 茶製品のプレミアム化

- eコマースの拡大

- レディ・トゥ・ドリンク(RTD)ティーの人気上昇

- 業界の潜在的リスク&課題

- 持続可能性と環境への懸念

- 原材料コストの変動

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- プラスチック

- 紙・板紙

- 金属

- その他

第6章 市場推計・予測:包装タイプ別、2021年~2034年

- 主要動向

- 軟包装

- 硬包装

第7章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 袋

- パウチ

- スティックパック&小袋

- 瓶・容器

- 箱・カートン

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor plc

- Berry Global Inc.

- Constantia Flexibles

- Coveris

- Duropack Limited

- Huhtamaki

- Mondi

- Printpack

- ProAmpac

- Sappi

- Sonoco Products Company

- SPG-Pack

- Sprinpak

- Swisspac Packaging

- Transcontinental Inc.

- WestRock Company

- Winpak LTD.

The Global Tea Packaging Market was valued at USD 6.3 billion in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. This growth is fueled by the rising global consumption of tea, the rapid expansion of ready-to-drink options, and the increasing demand for premium tea products. As tea remains the second most widely consumed beverage globally, packaging manufacturers are under constant pressure to develop innovative and high-quality solutions that preserve freshness and aroma while maintaining cost-effectiveness. Modern tea consumers prioritize sustainability, driving the need for packaging made from biodegradable and recyclable materials. Brands that align with these environmental preferences are gaining a competitive edge by adopting eco-friendly packaging solutions.

Additionally, the growing popularity of organic and specialty teas is accelerating the demand for premium packaging that reflects the high-quality nature of the product. Packaging designs that incorporate resealable options, moisture barriers, and light protection are becoming standard features, ensuring product longevity and enhancing the consumer experience. As global tea consumption trends point toward healthier lifestyles and increased interest in specialty beverages, the need for advanced and sustainable packaging solutions is expected to drive substantial market growth. Moreover, the rise of e-commerce has increased the need for sturdy, attractive, and functional packaging capable of withstanding the rigors of shipping while maintaining product integrity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.3 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 5.4% |

The tea packaging market is categorized by materials, including plastic, paper and paperboard, metal, and others. The paper and paperboard segment is expected to generate USD 5.7 billion by 2034, driven by the increasing preference for biodegradable and recyclable packaging. Many tea brands are shifting toward paper-based packaging due to its lightweight, compostable, and recyclable nature. Premium and specialty brands are also embracing crafted paperboard cartons to align with their environmentally friendly brand image and meet consumer expectations for sustainable practices. As consumer awareness around environmental impact grows, brands that offer compostable and reusable packaging options are experiencing higher customer loyalty and market differentiation.

Flexible packaging held a dominant 65.5% market share in 2024 due to its lightweight nature, cost-effectiveness, and superior ability to preserve the freshness of tea. This type of packaging, often made from laminated films, pouches, and resealable bags, provides exceptional protection against moisture, oxygen, and light, ensuring the tea maintains its quality for extended periods. As the demand for convenience and longer shelf life grows, flexible packaging solutions are becoming increasingly popular, especially for ready-to-drink and specialty teas.

The North America Tea Packaging Market is expected to reach USD 2.2 billion by 2034, propelled by the rising popularity of premium and organic tea products and a growing emphasis on sustainable packaging solutions. The U.S. market alone is forecasted to grow to USD 1.9 billion by 2034, driven by increased tea consumption, a shift toward higher-end organic products, and an ongoing preference for eco-conscious packaging. As consumers demand specialty teas that maintain freshness and authenticity, the need for packaging solutions that effectively preserve product quality has never been higher.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising tea consumption

- 3.2.1.2 Growing demand for sustainable packaging

- 3.2.1.3 Premiumization of tea products

- 3.2.1.4 Expansion of e-commerce

- 3.2.1.5 Rising popularity of ready-to-drink (RTD) teas

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sustainability and environmental concerns

- 3.2.2.2 Fluctuating raw material costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2021 – 2034 ($ Mn & Kilo Tons)

- 6.1 Key trends

- 6.2 Flexible packaging

- 6.3 Rigid packaging

Chapter 7 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn & Kilo Tons)

- 7.1 Key trends

- 7.2 Bags

- 7.3 Pouches

- 7.4 Stick pack & sachets

- 7.5 Jars & containers

- 7.6 Boxes & cartons

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Berry Global Inc.

- 9.3 Constantia Flexibles

- 9.4 Coveris

- 9.5 Duropack Limited

- 9.6 Huhtamaki

- 9.7 Mondi

- 9.8 Printpack

- 9.9 ProAmpac

- 9.10 Sappi

- 9.11 Sonoco Products Company

- 9.12 SPG-Pack

- 9.13 Sprinpak

- 9.14 Swisspac Packaging

- 9.15 Transcontinental Inc.

- 9.16 WestRock Company

- 9.17 Winpak LTD.