|

市場調査レポート

商品コード

1708190

フードサービス用使い捨て用品の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Food Service Disposable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フードサービス用使い捨て用品の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

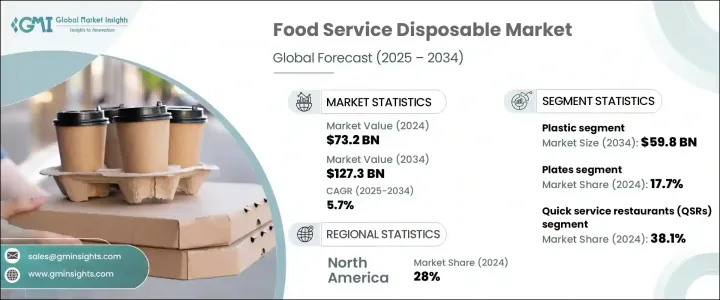

世界のフードサービス用使い捨て用品市場は、2024年に732億米ドルと評価され、2025年から2034年にかけてCAGR5.7%で成長すると予測されています。

この成長の主因は、クイックサービスレストラン(QSR)の急拡大とオンラインフードデリバリープラットフォームの急増です。都市化と消費者のライフスタイルの変化により、利便性への選好が高まり、QSRは衛生、業務効率、費用対効果を確保するため、幅広いフードサービス用使い捨て用品を採用するようになりました。この分野のメーカーは、QSRの高まる需要に応えるため、高品質でコスト効率が高く、環境的に持続可能な使い捨て製品の生産に注力する必要があります。市場が拡大し続ける中、衛生性と機能性を高める環境に優しい材料や革新的なデザインへの投資は、外食産業の進化する要件を満たす上で極めて重要です。

同時に、オンラインフードデリバリーサービスの世界の増加は、耐久性があり安全な使い捨て包装の需要を煽っています。デジタル注文、アプリベースのフードサービス、クラウドキッチンの人気が高まっているため、パッケージングプロバイダーは、食品の安全性と配達効率を維持する、長持ちし、漏れにくく、不正開封防止機能を備えたパッケージングソリューションを開発する必要に迫られています。消費者の間で健康志向が高まるにつれ、食品に安全で持続可能な生分解性材料への注目も顕著になっています。フードサービス用使い捨て用品メーカーは、オンライン食品注文システムの急速な成長をサポートするだけでなく、環境に優しい選択肢を求める消費者の選好に沿ったパッケージの開発を重視しなければなりません。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 732億米ドル |

| 予測金額 | 1,273億米ドル |

| CAGR | 5.7% |

市場は材料別に紙・板紙、プラスチック、アルミニウム、その他に区分されます。プラスチック分野は、2034年までに598億米ドルを生み出すと予測されています。持続可能性への懸念と規制圧力の高まりにより、プラスチック分野ではリサイクル可能で生分解性のソリューション開発へのシフトが見られます。堆肥化可能なプラスチックや先進リサイクル技術における新たなイノベーションは、環境に優しいパッケージングを求める顧客の要望と、外食産業における利便性や耐久性のニーズとのバランスを取るために企業が努力していることから、支持を集めています。

製品タイプ別に見ると、市場はプレート、トレイ、ボウル、カップ、クラムシェル、ラップ・フィルム、ホイル、その他に分けられます。プレートは2024年の市場シェアの17.7%を占めました。皿の需要は、QSR、屋台、オンラインフードサービスの成長によって、便利で外出先でも食べられるソリューションへのニーズが高まっていることが背景にあります。シングルユースで衛生的な食用ソリューションに対する消費者の選好が、このセグメントの成長にさらに寄与しています。さらに、持続可能な代替品を求める動きから、紙、竹、バガスなどの材料を使った堆肥化・生分解可能なプレートの開発も進んでいます。

市場はまた、最終用途別にQSR、フルサービスレストラン(FSR)、ケータリングサービス、オンラインデリバリー、その他に区分されます。2024年のシェアはQSRセグメントが38.1%で市場を独占しました。世界的および地域的なQSRチェーンの拡大と急速な近代化が相まって、テイクアウトやデリバリー時に食品の品質を維持しながら携帯性を高める軽量で耐久性があり柔軟な材料の採用に拍車をかけています。

北米は2024年の世界市場シェアの28%を占めました。同地域の消費者の選好はますます持続可能な包装ソリューションに傾いており、生分解性および堆肥化可能な包装材料の採用を促進しています。利便性、衛生、持続可能性に対する消費者の期待に応える、堅牢で漏れにくく、不正開封防止機能を備えた包装に対する需要の高まりを反映しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 産業エコシステム分析

- 業界への影響要因

- 成長促進要因

- コンビニエンスフードへの需要の高まり

- オンライン食品デリバリープラットフォームの成長

- 新興国における可処分所得の増加

- クイックサービスレストラン(QSR)の拡大

- 企業・施設部門におけるケータリングサービスの台頭

- 業界の潜在的リスク・課題

- 使い捨てプラスチックに関する環境問題や規制

- 原材料価格の変動

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- GAP分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- プラスチック

- ポリプロピレン(PP)

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリスチレン(PS)

- 生分解性プラスチック

- その他

- 紙・板紙

- アルミニウム

- その他

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- プレート

- トレー

- ボウル

- カップ

- クラムシェル

- ラップ・フィルム

- ホイル

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- クイックサービスレストラン(QSR)

- フルサービスレストラン(FSR)

- ケータリングサービス

- オンラインデリバリー

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Anchor Packaging

- Berry Global

- Billerud

- Contital

- D&W Fine Pack

- Dart Container

- Georgia-Pacific

- Graphic Packaging International

- Huhtamaki

- Oji Fibre Solutions

- Pactiv Evergreen

- Plus Pack

- ProAmpac

- Stora Enso

- Vegware

- WestRock

- WinCup

The Global Food Service Disposable Market was valued at USD 73.2 billion in 2024 and is projected to grow at a CAGR of 5.7% from 2025 to 2034. This growth is primarily driven by the rapid expansion of quick-service restaurants (QSRs) and the surge in online food delivery platforms. Urbanization and changing consumer lifestyles have increased the preference for convenience, prompting QSRs to adopt a wide range of food service disposables to ensure hygiene, operational efficiency, and cost-effectiveness. Manufacturers in this space must focus on producing high-quality, cost-effective, and environmentally sustainable disposable products to cater to the growing demand from QSRs. As the market continues to expand, investments in eco-friendly materials and innovative designs that enhance hygiene and functionality will be pivotal in meeting the evolving requirements of the food service industry.

Simultaneously, the global rise in online food delivery services is fueling the demand for durable and secure disposable packaging. The increasing popularity of digital ordering, app-based food services, and cloud kitchens has pushed packaging providers to develop long-lasting, leak-proof, and tamper-evident packaging solutions that maintain food safety and delivery efficiency. As health consciousness grows among consumers, the focus on food-safe, sustainable, and biodegradable materials is becoming more pronounced. Food service disposable producers must emphasize the development of packaging that not only supports the rapid growth of online food ordering systems but also aligns with consumers' preferences for environmentally friendly options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $73.2 Billion |

| Forecast Value | $127.3 Billion |

| CAGR | 5.7% |

The market is segmented by material into paper and paperboard, plastic, aluminum, and others. The plastic segment is anticipated to generate USD 59.8 billion by 2034. Due to sustainability concerns and increasing regulatory pressures, the plastic segment is witnessing a shift towards the development of recyclable and biodegradable solutions. New innovations in compostable plastics and advanced recycling technologies are gaining traction as businesses strive to balance customer demand for eco-friendly packaging with the need for convenience and durability in the food service sector.

By product type, the market is divided into plates, trays, bowls, cups, clamshells, wraps and films, foils, and others. Plates accounted for 17.7% of the market share in 2024. Demand for plates is rising due to the increasing need for convenient, on-the-go eating solutions, driven by the growth of QSRs, street food vendors, and online food services. Consumers' preference for single-use, hygienic eating solutions is further contributing to segment growth. Moreover, the push for sustainable alternatives has led to the development of compostable and biodegradable plates made from materials such as paper, bamboo, and bagasse.

The market is also segmented by end-use into QSRs, full-service restaurants (FSRs), catering services, online delivery, and others. The QSR segment dominated the market with a 38.1% share in 2024. Global and regional QSR chain expansion, combined with rapid modernization, has spurred the adoption of lightweight, durable, and flexible materials that enhance portability while maintaining food quality during takeout and delivery.

North America accounted for 28% of the global market share in 2024. Consumer preferences in the region are increasingly leaning towards sustainable packaging solutions, driving the adoption of biodegradable and compostable packaging materials. The US food service disposable market alone generated USD 16.6 billion in 2024, reflecting the growing demand for robust, leak-proof, and tamper-evident packaging that meets consumer expectations for convenience, hygiene, and sustainability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for convenience food

- 3.2.1.2 Growth of online food delivery platforms

- 3.2.1.3 Rising disposable income in emerging economies

- 3.2.1.4 Expansion of quick-service restaurants (QSRs)

- 3.2.1.5 Rise of catering services in corporate and institutional sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns and regulations on single-use plastics

- 3.2.2.2 Fluctuating raw material prices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 GAP analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Bn & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.2.1 Polypropylene (PP)

- 5.2.2 Polyethylene (PE)

- 5.2.3 Polyethylene terephthalate (PET)

- 5.2.4 Polystyrene (PS)

- 5.2.5 Biodegradable plastic

- 5.2.6 Others

- 5.3 Paper & paperboard

- 5.4 Aluminum

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Bn & Kilo Tons)

- 6.1 Key trends

- 6.2 Plates

- 6.3 Trays

- 6.4 Bowls

- 6.5 Cups

- 6.6 Clamshells

- 6.7 Wraps & films

- 6.8 Foils

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Bn & Kilo Tons)

- 7.1 Key trends

- 7.2 Quick service restaurants (QSRs)

- 7.3 Full-service restaurants (FSRs)

- 7.4 Catering services

- 7.5 Online delivery

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anchor Packaging

- 9.2 Berry Global

- 9.3 Billerud

- 9.4 Contital

- 9.5 D&W Fine Pack

- 9.6 Dart Container

- 9.7 Georgia-Pacific

- 9.8 Graphic Packaging International

- 9.9 Huhtamaki

- 9.10 Oji Fibre Solutions

- 9.11 Pactiv Evergreen

- 9.12 Plus Pack

- 9.13 ProAmpac

- 9.14 Stora Enso

- 9.15 Vegware

- 9.16 WestRock

- 9.17 WinCup