|

市場調査レポート

商品コード

1699427

不動産用ディーゼル発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Diesel Powered Real Estate Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 不動産用ディーゼル発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

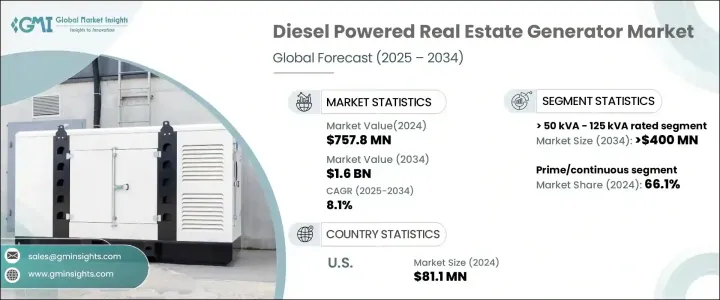

不動産用ディーゼル発電機の世界市場は、2024年に7億5,780万米ドルに達し、2025年から2034年にかけてCAGR 8.1%で成長すると予測されています。

世界的に都市化が加速し、信頼性が高く安定した電力ソリューションへの需要が高まる中、市場は大きな勢いを見せています。特に新興経済諸国では急速なインフラ開発が進み、バックアップ電源や継続的な電源の必要性が高まっています。住宅と商業の両分野で不動産プロジェクトが拡大する中、開発業者は中断のない電力供給を確保するため、効率的で費用対効果の高いディーゼル発電機に投資しています。異常気象による停電の頻度の増加、送電網の老朽化、エネルギー消費の増大は、市場の拡大をさらに促進します。

技術的進歩は、引き続き市場成長の推進に重要な役割を果たしています。自動負荷管理システム、電子燃料噴射、ターボ過給機構などの技術革新は、燃費を改善し、排出ガスを削減しています。カーボンフットプリントの最小化を目指す規制圧力が、メーカーをよりクリーンで静かでエネルギー効率の高いディーゼル発電機の開発に駆り立てています。政府や民間の利害関係者は、送電網の故障に伴うリスクを軽減し、不動産部門全体の事業継続性を確保するため、バックアップ電源ソリューションに多額の投資を行っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億5,780万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 8.1% |

定格50kVA未満のディーゼル発電機は、2024年に1億2,000万米ドルと評価されました。これらの小型発電機に対する需要の高まりは、停電しやすい地域や信頼できる送電網インフラがない地域で安定した電力を供給する能力に起因しています。燃料効率と騒音低減の進歩により、これらの発電機は安定したエネルギー・ソリューションを求める住宅所有者や企業にとって好ましい選択肢となっています。コンパクトで高性能なこれらのユニットは、一時的または補助的な電力が不可欠な都市部や半都市部の開発で支持を集めています。

市場は、スタンバイ発電と原動機/連続発電の2つの主要アプリケーション・セグメントに分けられます。2024年には、原動機/連続発電機が市場シェア全体の66.1%を占め、運転効率の向上と燃料節約能力の強化がその原動力となっています。高度な噴射技術とインテリジェントな電力管理システムを特徴とする次世代ディーゼルエンジンへの公共投資と民間投資が、採用率を高めています。産業界や不動産開発業者が持続可能かつ強力なエネルギー・ソリューションを優先する中、技術的に優れたディーゼル発電機への需要は高まり続けています。

米国の不動産用ディーゼル発電機市場は、2024年に8,110万米ドルと評価されました。異常気象による電力障害の増加、電力網の老朽化、電力需要の急増により、信頼性の高いバックアップ電源ソリューションの必要性が高まっています。不動産開発業者、商業施設所有者、インフラ計画者は、中断のない業務を維持し、停電に伴うリスクを軽減するためにディーゼル発電機に注目しています。米国市場は、発電機の効率向上、排出量削減、系統独立型電源ソリューションの拡大に向けた投資で、エネルギー・プロバイダーの焦点であり続けています。電力信頼性への懸念が高まる中、不動産用途におけるディーゼル発電機の役割は、これまで以上に重要になっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:定格出力別

- 主要動向

- 50 kVA以下

- 50 kVA-125 kVA

- 125 kVA-200 kVA

- 200 kVA-350 kVA

- 350 kVA-500 kVA

- 500 kVA超

第6章 市場規模・予測:用途別

- 主要動向

- スタンバイ

- プライム/コンティニュアス

第7章 市場規模・予測:地域別

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- フィリピン

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- アンゴラ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

第8章 企業プロファイル

- Aggreko

- Atlas Copco

- Caterpillar

- Cooper

- Cummins

- DEUTZ Power Center

- Generac Power Systems

- Greaves Cotton

- HIMOINSA

- J C Bamford Excavators

- Kirloskar

- Mahindra Powerol

- Rehlko

- Rolls-Royce

- YANMAR HOLDINGS

The Global Diesel Powered Real Estate Generator Market reached USD 757.8 million in 2024 and is projected to grow at a CAGR of 8.1% between 2025 and 2034. The market is witnessing significant momentum as urbanization accelerates worldwide, increasing the demand for reliable and stable power solutions. Rapid infrastructure development, especially in emerging economies, is amplifying the need for backup and continuous power sources. With real estate projects expanding in both residential and commercial sectors, developers are investing in efficient and cost-effective diesel generators to ensure uninterrupted power supply. The increasing frequency of power outages due to extreme weather conditions, aging grid networks, and growing energy consumption further fuels market expansion.

Technological advancements continue to play a critical role in driving market growth. Innovations such as automatic load management systems, electronic fuel injection, and turbocharging mechanisms are improving fuel efficiency and reducing emissions. Regulatory pressures aimed at minimizing carbon footprints have pushed manufacturers to develop cleaner, quieter, and more energy-efficient diesel generators. Governments and private stakeholders are heavily investing in backup power solutions to mitigate risks associated with grid failures, ensuring business continuity across real estate sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $757.8 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 8.1% |

Diesel-powered real estate generators with a rating of <= 50 kVA were valued at USD 120 million in 2024. The rising demand for these smaller generators stems from their ability to deliver consistent power in regions prone to outages or lacking reliable grid infrastructure. Advancements in fuel efficiency and noise reduction have made these generators a preferred choice for homeowners and businesses seeking stable energy solutions. Compact and high-performing, these units are gaining traction in urban and semi-urban developments where temporary or supplemental power is essential.

The market is divided into two primary application segments: standby and prime/continuous power generation. In 2024, prime/continuous generators accounted for 66.1% of the total market share, driven by improvements in operational efficiency and enhanced fuel-saving capabilities. Public and private investments in next-generation diesel engines featuring advanced injection technologies and intelligent power management systems are bolstering adoption rates. As industries and real estate developers prioritize sustainable yet powerful energy solutions, the demand for technologically superior diesel generators continues to rise.

The U.S. diesel-powered real estate generator market was valued at USD 81.1 million in 2024. Increasing power disruptions caused by extreme weather conditions, an aging power grid, and surging electricity demand have intensified the need for reliable backup power solutions. Real estate developers, commercial property owners, and infrastructure planners are turning to diesel generators to maintain uninterrupted operations and mitigate risks associated with power failures. The U.S. market remains a focal point for energy providers, with investments directed toward upgrading generator efficiency, lowering emissions, and expanding grid-independent power solutions. As electricity reliability concerns grow, the role of diesel-powered generators in real estate applications is becoming more critical than ever.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 350 kVA

- 5.6 > 350 kVA - 500 kVA

- 5.7 > 500 kVA

Chapter 6 Market Size and Forecast, By Application (USD Million & Units)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Prime/continuous

Chapter 7 Market Size and Forecast, By Region (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Atlas Copco

- 8.3 Caterpillar

- 8.4 Cooper

- 8.5 Cummins

- 8.6 DEUTZ Power Center

- 8.7 Generac Power Systems

- 8.8 Greaves Cotton

- 8.9 HIMOINSA

- 8.10 J C Bamford Excavators

- 8.11 Kirloskar

- 8.12 Mahindra Powerol

- 8.13 Rehlko

- 8.14 Rolls-Royce

- 8.15 YANMAR HOLDINGS