中東・アフリカのディーゼル発電機市場:シェア分析、産業動向、統計、成長動向予測(2025年~2030年)

Middle East And Africa Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644283

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

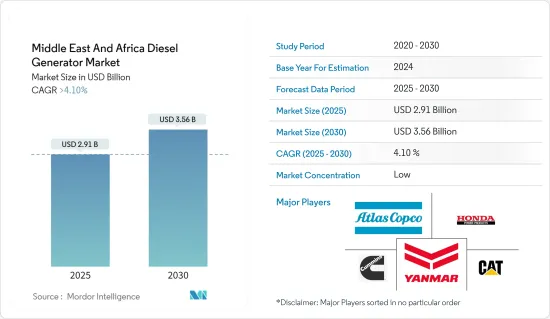

中東・アフリカのディーゼル発電機市場規模は、2025年に29億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.1%を超え、2030年には35億6,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、配電センターからの不安定な電力供給と建設インフラプロジェクトの増加が予測期間中の市場を牽引するとみられます。

- 一方、二酸化炭素排出量に対する懸念の高まりは、予測期間中の市場成長の妨げになると予想されます。

- 再生可能エネルギー源とディーゼル発電機を統合したハイブリッドシステムは、中東・アフリカのディーゼル発電機市場に大きな機会をもたらすと期待されています。

- ナイジェリアは、同地域におけるエネルギー需要の増加により、市場の支配的な地域になると予想されます。

中東・アフリカのディーゼル発電機市場動向

バックアップ発電機セグメントが市場を独占

- 中東・アフリカは、頻繁な停電、送電網の不安定性、エネルギーの供給を妨げる厳しい気候条件としばしば戦っています。重要な業務を維持し、重要な機器を保護し、必要不可欠なサービスを維持するためには、無停電電力が不可欠であることから、バックアップ発電機の魅力的な価値提案が強調されています。

- さらに、この地域で見られる産業の成長は、バックアップ発電機の重要性を高めています。この地域の産業情勢が盛んになるにつれて、安定した回復力のある電源に対する需要が最も重要になります。バックアップ発電機は、電力途絶に起因する潜在的な生産損失、収益への影響、操業停止時間に対して信頼できる安全装置を提供し、全体的な事業継続性を高めています。

- Energy Institute Statistical Review Of World Energy 2023によると、中東・アフリカの2022年の発電量は2021年に比べ0.6%増加しました。同時に、2012~2022年の年間成長率は2.2%を記録しました。同地域では電力需要が増加しているため、特にアフリカ地域では発電源が同じ場所で増加していないです。したがって、ディーゼル発電機の需要は今後数年間で増加すると予想されます。

- さらに、技術とデータインフラへの依存がバックアップ発電機の重要性を高めています。データセンター、通信施設、デジタルサービスの普及は、これらの重要なシステムの完全性と機能性を確保するために、継続的で安定した電力供給を必要とします。停電時に迅速に電力供給を引き受ける機能を備えたバックアップ発電機は、技術的な運用を保護する重要な要として浮上しています。

- 例えば、2023年2月、Microsoftはサウジアラビアに新しいデータセンターとAzureクラウド地域を建設する予定でした。これは、リヤドで開催されたLEAP 2023会議で発表されました。

- バックアップディーゼル発電機は、今後も市場を独占し続けると予想されます。これは、他の市場セグメントと比較して、その柔軟な使用方法と発電用の大きなサイズによるものです。

市場を独占するナイジェリア

- 急増する人口、急速な都市化、多様な産業部門により、信頼性の高い電源に対する需要が高まっています。既存の送電網に課題がある中、ナイジェリアでは電力の安定供給が求められており、エネルギーギャップを埋め、重要な業務をサポートするソリューションとしてディーゼル発電機の魅力が高まっている

- さらに、ナイジェリアのインフラ開発と建設ブームは、ディーゼル発電機の重要性を高めています。交通網、不動産プロジェクト、製造施設の拡大が続いており、安定した電力供給が必要とされています。ディーゼル発電機は、一時的な電力需要やバックアップ電力需要に対応し、ナイジェリアの野心的な開発イニシアチブを強化する、重要なイネーブラーとして浮上しています。

- 例えば、国際貿易局によると、ナイジェリアの建設市場規模は近年増加傾向にあります。2021年には1,277億米ドルだった市場規模は、2022年には1,315億3,000万米ドルとなり、3%強の成長率を記録しました。

- さらに、ナイジェリアの経済活動の地理的分布は、その優位性をさらに際立たせています。国土の変化に富み、都市の中心部では適応性の高い電力ソリューションが求められており、ディーゼル発電機は都市部でも遠隔地でも電力を供給できる柔軟性を備えています。この多用途性により、ナイジェリアは多様なディーゼル発電機用途の可能性を生かすことができます。

- 例えば、2023年3月、Hyundai Heavy EngineeringはMikano International Ltdとディーゼル発電機6台を供給する契約を締結したと発表しました。Mikano International Ltdはラゴスにプロジェクトを建設中で、同社はバックアップ電源としてこのディーゼル発電機を使用する予定です。Hyundaiは、ディーゼル発電機は2024年5月末までにナイジェリアに出荷されると発表しました。

- 結論として、中東・アフリカのディーゼル発電機市場でナイジェリアが注目されるのは、経済成長、インフラ拡大、地域力学にしっかりと根ざしたものです。ナイジェリアがエネルギー需給の複雑さを乗り越えていく中で、ディーゼル発電機の統合は、エネルギーの回復力を再定義し、インフラ開発を支援し、ナイジェリアのエネルギー安全保障とサステイナブル発展に大きく貢献する、変革的な力として浮上しています。

中東・アフリカのディーゼル発電機産業概要

中東・アフリカのディーゼル発電機市場は、部分的にセグメント化されています。この市場の主要企業(順不同)には、Caterpillar Inc.、Cummins Ltd.、Yanmar Holdings、Atlas Copco AB、Honda Siel Power Products Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 202年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 不安定な電力供給

- 建設インフラプロジェクト

- 抑制要因

- 環境への懸念

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 定格電力

- 0~75kVA

- 75~375kVA

- 375kVA以上

- 用途

- 主電源

- バックアップ電源

- ピークカット

- 市場分析:2028年までの市場規模と需要予測(地域別)

- ナイジェリア

- イラク

- サウジアラビア

- アラブ首長国連邦

- カタール

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Cummins Inc.

- Kirloskar Oil Engines Limited

- Honda Siel Power Products Limited

- Yanmar Holdings Co. Ltd

- Caterpillar Inc.

- Mitsubishi Heavy Industries Ltd

- Perkins Engines Company Limited

- Atlas Copco AB

- 市場シェア

第7章 市場機会と今後の動向

- ハイブリッドソリューション

目次

Product Code: 70581

The Middle East And Africa Diesel Generator Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 3.56 billion by 2030, at a CAGR of greater than 4.1% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the unreliable power supply from the distribution center and increasing construction and infrastructure projects are expected to drive the market during the forecasted period.

- On the other hand, increasing concerns over carbon emissions are expected to hinder the growth of the market during the forecasted period.

- Nevertheless, hybrid systems with integrated diesel generators with renewable energy sources are expected to create huge opportunities for the Middle-East and African diesel generator market.

- Nigeria is expected to be a dominant region for the market due to the increasing demand for energy in the region.

MEA Diesel Generator Market Trends

Backup Generator Segment to Dominate the Market

- The Middle-East and Africa often contend with frequent power outages, grid instability, and challenging climatic conditions that disrupt energy availability. The critical need for uninterrupted power to sustain vital operations, protect sensitive equipment, and maintain essential services underscores the compelling value proposition of backup generators.

- Moreover, the industrial growth witnessed in the region amplifies the significance of backup generators. The demand for consistent and resilient power sources becomes paramount as the region's industrial landscape flourishes. Backup generators offer a reliable safeguard against potential production losses, revenue impacts, and operational downtime resulting from power disruptions, thus enhancing overall business continuity.

- According to the Energy Institute Statistical Review Of World Energy 2023, the electricity generated in 2022 grew by 0.6% compared to 2021 in the Middle-East and African region. At the same time, an annual growth rate of 2.2% was recorded between 2012 and 2022. As the demand for electricity is increasing in the region, the power generating sources are not increasing at the same place, specifically in the African region; therefore, the demand for diesel generators is expected to rise in the coming years.

- Furthermore, the dependence on technology and data infrastructure elevates the importance of backup generators. The proliferation of data centers, telecommunications facilities, and digital services requires a continuous and stable power supply to ensure the integrity and functionality of these critical systems. Backup generators, equipped to assume power delivery during outages swiftly, emerge as a critical linchpin in safeguarding technological operations.

- For instance, in February 2023, Microsoft intended to build a new data center and Azure cloud region in Saudi Arabia. It was announced during the LEAP 2023 conference in Riyadh.

- Backup diesel generators are, thus, expected to continue dominating the market. This is due to their flexibility in usage and large size for electricity generation compared to other market segments.

Nigeria to Dominate the Market

- The nation's burgeoning population, rapid urbanization, and diverse industrial sectors create a heightened demand for reliable power sources. Nigeria's quest for uninterrupted electricity supply amid existing grid challenges enhances the appeal of diesel generators as a solution to bridge energy gaps and support critical operations.

- Moreover, Nigeria's infrastructure development and construction boom amplify the significance of diesel generators. The ongoing expansion of transportation networks, real estate projects, and manufacturing facilities necessitates a stable power supply. Diesel generators emerge as a vital enabler, catering to temporary and backup power needs and bolstering Nigeria's ambitious development initiatives.

- For instance, according to the International Trade Administration, Nigeria's construction market size has been on the rise in recent years. In 2022, the total market size was USD 131.53 billion, compared to USD 127.7 billion in 2021, while registering a growth rate of just over 3%.

- Furthermore, Nigeria's geographical distribution of economic activity further underscores its dominance. The nation's varied landscapes and urban centers call for adaptable power solutions, where diesel generators offer the flexibility to provide power in urban and remote settings. This versatility positions Nigeria to capitalize on the potential for a diverse range of diesel generator applications.

- For instance, in March 2023, Hyundai Heavy Engineering announced that the company had signed a contract with Mikano International Ltd to provide six diesel generators. Mikano International Ltd is building a project in Lagos where the company is expected to use these diesel generators as a backup power solution. Hyundai announced that the diesel generators will be shipped to Nigeria by the end of May 2024.

- In conclusion, the envisaged prominence of Nigeria within the Middle-East and African diesel generator market is firmly grounded in economic growth, infrastructure expansion, and regional dynamics. As Nigeria navigates the complexities of energy demand and supply, the integration of diesel generators emerges as a transformative force, poised to redefine energy resilience, support infrastructure development, and contribute significantly to Nigeria's journey towards energy security and sustainable progress.

MEA Diesel Generator Industry Overview

The Middle-East and African diesel generator market is partially fragmented. Some of the key players in this market (in no particular order) include Caterpillar Inc., Cummins Ltd, Yanmar Holdings Co. Ltd, Atlas Copco AB, and Honda Siel Power Products Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 202

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Unreliable Power Supply

- 4.5.1.2 Construction and Infrastructure Projects

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ratings

- 5.1.1 0-75 kVA

- 5.1.2 75-375 kVA

- 5.1.3 Above 375 kVA

- 5.2 Application

- 5.2.1 Prime Power

- 5.2.2 Backup Power

- 5.2.3 Peak Shaving

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 Nigeria

- 5.3.2 Iraq

- 5.3.3 Saudi Arabia

- 5.3.4 United Arab Emirates

- 5.3.5 Qatar

- 5.3.6 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cummins Inc.

- 6.3.2 Kirloskar Oil Engines Limited

- 6.3.3 Honda Siel Power Products Limited

- 6.3.4 Yanmar Holdings Co. Ltd

- 6.3.5 Caterpillar Inc.

- 6.3.6 Mitsubishi Heavy Industries Ltd

- 6.3.7 Perkins Engines Company Limited

- 6.3.8 Atlas Copco AB

- 6.4 Market Share

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Hybrid Solutions

中東・アフリカのディーゼル発電機市場:シェア分析、産業動向、統計、成長動向予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日