|

市場調査レポート

商品コード

1643177

欧州のディーゼル発電機:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のディーゼル発電機:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

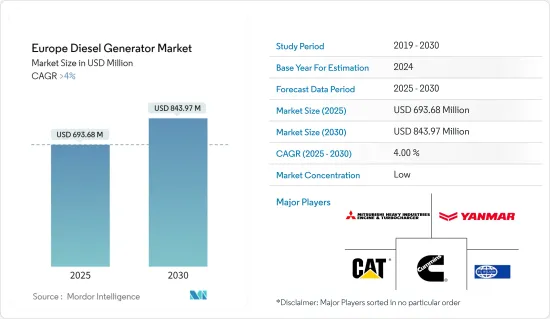

欧州のディーゼル発電機市場規模は、2025年に6億9,368万米ドルと推定され、2030年には8億4,397万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4%を超えると予測されます。

主要ハイライト

- 中期的には、スタンバイ用途のディーゼル発電機のニーズが市場を牽引すると予測されます。これらの発電機は、産業、建設、医療、オフグリッド用途など多くのセグメントで必要とされています。

- オングリッド、オフグリッドの両方で、代替電源として再生可能エネルギーの利用が拡大しているため、今後数年間は市場の成長が鈍化する可能性が高いです。

- 再生可能エネルギー源へのシフトが進む中、欧州の消費者は、太陽光のような再生可能エネルギー源を組み込んだハイブリッド・ディーゼル発電機のような、効率的で環境に安全な選択肢を求めています。このことは、近い将来、市場参入企業に大きなビジネス機会をもたらすと予想されます。

欧州のディーゼル発電機市場動向

産業セグメントが市場を独占する見込み

- 鉱業、製造業、農業、建設業を含む産業セグメントは、今後数年間に使用されるエネルギーの半分以上を使用しています。

- エネルギー使用量が最も多いのは、鉱業、製造業、農業、建設業を含む産業部門です。このため、これらの産業、特に医療、製薬、製造施設では、常時稼動で信頼性の高い電力がますます必要とされるため、ディーゼル発電機の需要が高まる可能性が高いです。

- したがって、製薬や製造施設などの産業では、継続的で信頼性の高い電力供給に対する需要が高まっており、ディーゼル発電機の需要が拡大すると予想されます。産業事業は主に、停電時(操業停止時間を避けるため)や送電網へのアクセスが制限されている地域で、ディーゼル発電機から発電された電力に依存しています。

- 2023年現在、欧州はアジア太平洋に次ぐ世界第2位の鉄鋼生産国です。世界鉄鋼協会によると、2023年の欧州連合の鉄鋼生産量は1億2,630万トンです。鉄鋼業は電力の主要な消費者であり、鉄鋼製造のために大量の信頼できるエネルギーを必要とします。ドイツのような多くの国では、いまだにディーゼル発電機を鉄鋼業に使用しており、これが国の開発作業を支えています。

- 今後数年間で、英国とロシアはともに産業部門の成長が見込まれます。これは、両国の製造業が急成長しているためで、産業部門におけるディーゼル発電機の需要が高まる可能性が高いです。

- さらに、特に英国とトルコでは、産業部門を拡大するための政府の取り組みが、予測期間中にディーゼル発電機の需要を促進すると予想されます。

英国が市場を独占する見込み

- 英国は、世界で最も発展した国の一つであり、欧州で最も工業化された国の一つです。増え続けるエネルギー需要に伴い、経済のさまざまなセグメントでも中断のない電力供給が必要とされています。

- 英国の送電網は、ピーク時のバックアップ電源を必要としています。National Grid Electricity Transmission(NGET)は、このピーク需要に対応するためにディーゼル発電機(DG)セットを使用し、冷却ファン、ポンプ、照明などの重要な活動のために変電所にバックアップ電力を供給してきました。

- バックアップ発電機は、イングランドとウェールズ全土にある250以上のNGETサイトで使用されており、その大半はディーゼル発電です。これらのシステムは、NGETに電力供給喪失事故からの回復力を提供しています。

- 生活水準の向上により、電力バックアップ装置の需要が高まっており、国はディーゼル発電機のコストと有効性から恩恵を受けています。英国では、農業、通信、建設などさまざまなセグメントで定期的に発電機が利用されています。

- 国内の建設活動はここ数ヶ月で増加しています。英国政府によると、2023年には新規住宅公募のために175.5件の発注があり、これは2018年から継続的に増加しています。建設活動の増加は、予測期間中にディーゼル発電機の需要を生み出すと予想されます。

- 英国の農業セクターは規模が大きく、国土面積の60%以上を占めています。同国の送電網は再生可能電源への依存度を高めているが、農業産業は電源バックアップシステムへの関心が高いです。ディーゼル発電システムへの依存度が高まっており、これが市場を牽引しています。

- 欧州のデータセンターの40%以上が英国にあり、大量の電力を消費しています。データセンターは、停電時の電力需要を満たすためにディーゼル発電機を使用しています。2023年現在、英国では513のデータセンターが稼動しています。

- 同国では今後数年間、より多くのデータセンターが確認され、ディーゼル発電機の需要が増加すると予想されています。

欧州のディーゼル発電機産業概要

欧州のディーゼル発電機市場は、適度にセグメント化されています。同市場の主要参入企業には、Caterpillar Inc.、Mitsubishi Heavy Industries Engine &Turbocharger Ltd.、FG Wilson Engineering(Dublin)Ltd.、Cummins Inc.、Yanmar Holdingsなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- スタンバイ用途におけるディーゼル発電機のニーズ

- 複数のエンドユーザー産業における使用の増加

- 抑制要因

- 代替電源としての再生可能エネルギー利用の増加

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 容量

- 75kVA以下

- 75~350kVA以下

- 350kVA以上

- エンドユーザー

- 住宅用

- 商業用

- 産業用

- 地域

- ドイツ

- ロシア

- 英国

- ノルウェー

- ノルディック

- フランス

- イタリア

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Caterpillar Inc.

- Mitsubishi Heavy Industries Engine & Turbocharger Ltd

- F G Wilson

- Cummins Inc.

- Yanmar Holdings Co. Ltd

- Generac Power Systems

- Kohler Co.

- Doosan Corporation

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- ハイブリッドディーゼル発電機の需要増加

The Europe Diesel Generator Market size is estimated at USD 693.68 million in 2025, and is expected to reach USD 843.97 million by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

Key Highlights

- In the medium period, the market is expected to be driven by the need for diesel generators in standby applications. These generators are needed in many fields, including industrial, construction, medical, and off-grid applications.

- The growing use of renewables as an alternative power source, both on-grid and off-grid, is likely to slow the market's growth over the next few years.

- Nevertheless, with the increasing shift toward renewable energy sources, European consumers are looking for efficient and environmentally safe options, such as hybrid diesel generators that incorporate renewable sources like solar. This, in turn, is expected to create significant opportunities for the market players in the near future.

Europe Diesel Generator Market Trends

The Industrial Segment is Expected to Dominate the Market

- The industrial segment, which includes mining, manufacturing, agriculture, and construction, uses more than half of the energy that will be used over the next few years.

- The largest amount of energy is used by the industrial sector, which includes mining, manufacturing, agriculture, and construction. Because of this, the demand for diesel generators is likely to go up as these industries, especially healthcare, pharmaceutical, and manufacturing facilities, need more and more power that is always on and reliable.

- Therefore, the increasing demand for continuous and reliable power supply in industries like pharmaceuticals and manufacturing facilities is expected to escalate the demand for diesel generators. Industrial operations mainly depend on electricity generated from diesel generators during power outages (to avoid operation downtime) and in regions with limited grid access.

- As of 2023, Europe was the second-largest producer of steel in the world after Asia-Pacific. According to the World Steel Association, in 2023, the European Union produced 126.3 million tonnes of steel. The steel industry is a major consumer of power and requires a large amount of reliable energy for steel manufacturing. Many countries like Germany still use diesel generators for the steel industry, which are the backbone of the country's development work.

- In the next few years, both the United Kingdom and Russia are likely to see growth in their industrial sectors. This is because the manufacturing sectors in both countries are growing quickly, which is likely to increase the demand for diesel generators in the industrial sector.

- Furthermore, government initiatives to expand the industrial sector, especially in the United Kingdom and Turkey, are expected to propel the demand for diesel generators during the forecast period.

The United Kingdom is Expected to Dominate the Market

- The United Kingdom is one of the most developed countries in the world and one of the most industrialized countries in Europe. With an ever-increasing demand for energy, various sectors of the economy also need an uninterrupted power supply.

- The United Kingdom's national grid requires a backup power source when there is a peak demand. The National Grid Electricity Transmission (NGET) has been using diesel generators (DG) sets to accommodate this peak demand and provide backup power to substations for key activities such as cooling fans, pumps, and lighting, enabling it to continue to perform its crucial role in the electricity transmission system.

- Backup generators are used at over 250 NGET sites across England and Wales, the majority of which are diesel-powered. These systems provide NGET with the resilience to recover from a loss of power supply event.

- The country benefits from the cost and effectiveness of diesel generators, with improved living standards increasing the demand for power backup devices. Various sectors, such as agriculture, telecommunication, and construction, within the United Kingdom regularly utilize generators.

- Construction activity around the country has been increasing in the past few months. According to the government of the United Kingdom, in 2023, 175.5 orders were placed for new housing public, which has been continuously increasing since 2018. The rise in construction activities is expected to create demand for diesel generators during the forecast period.

- The UK agriculture sector is large and covers more than 60% of the country's total land area. Although the country's power grid is increasingly dependent on renewable sources, the agriculture industry is more interested in the power backup system. It is becoming more dependent on diesel generator systems, which is driving the market.

- More than 40% of the data centers in Europe are present in the United Kingdom and consume a significant amount of power. The data center uses a diesel generator to meet the demand for electricity during a power cut. As of 2023, there were 513 data centers active in the United Kingdom.

- The country is expected to witness more data centers in the coming years, increasing the demand for diesel generators.

Europe Diesel Generator Industry Overview

The European diesel generator market is moderately fragmented. Some of the major players in the market are Caterpillar Inc., Mitsubishi Heavy Industries Engine & Turbocharger Ltd, FG Wilson Engineering (Dublin) Ltd, Cummins Inc., and Yanmar Holdings Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Need for Diesel Generators in Standby Applications

- 4.5.1.2 Increasing Use in Several End-user Industries

- 4.5.2 Restraints

- 4.5.2.1 Growing Use of Renewables as an Alternative Power Source

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Capacity

- 5.1.1 Below 75 kVA

- 5.1.2 75-350 kVA

- 5.1.3 Above 350 kVA

- 5.2 End User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 Russia

- 5.3.3 United Kingdom

- 5.3.4 Norway

- 5.3.5 NORDIC

- 5.3.6 France

- 5.3.7 Italy

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Mitsubishi Heavy Industries Engine & Turbocharger Ltd

- 6.3.3 F G Wilson

- 6.3.4 Cummins Inc.

- 6.3.5 Yanmar Holdings Co. Ltd

- 6.3.6 Generac Power Systems

- 6.3.7 Kohler Co.

- 6.3.8 Doosan Corporation

- 6.4 List of Other Prominent Players

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Hybrid Diesel Generators