|

市場調査レポート

商品コード

1699410

バイオマーカー探索アウトソーシングサービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Biomarker Discovery Outsourcing Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| バイオマーカー探索アウトソーシングサービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

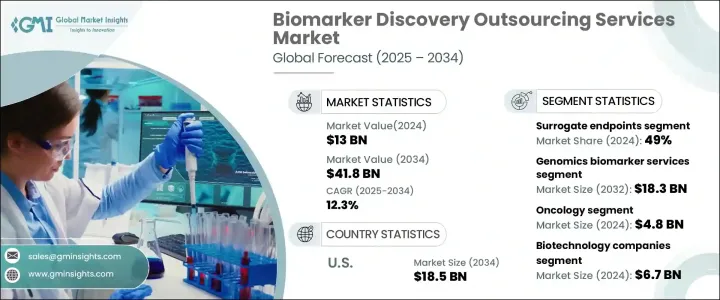

世界のバイオマーカー探索アウトソーシングサービス市場は、2024年に130億米ドルと評価され、2025年から2034年にかけてCAGR 12.3%で拡大すると予測されています。

同市場は、慢性疾患の増加、オミックス技術の急速な進歩、製薬・バイオテクノロジー部門における研究開発投資の増加などを背景に大きく成長しています。個別化医療が重視されるようになり、がん、心血管疾患、糖尿病などの慢性疾患の早期発見、診断、モニタリングを可能にする新規バイオマーカーの需要がさらに高まっています。慢性疾患の有病率が世界的に上昇する中、的を絞った治療戦略を促進するバイオマーカーに対する需要は増加の一途をたどっています。

政府のイニシアチブの高まり、製薬会社と研究機関の協力、バイオマーカー検証に対する規制当局の支援が、市場の拡大を加速しています。バイオマーカー探索における人工知能(AI)と機械学習(ML)の採用の増加も、潜在的なバイオマーカーの迅速な同定と検証を可能にし、業界を変革しています。新興国は、ヘルスケア支出の増加と高度な臨床研究センターの設立により、バイオマーカー研究の主要なプレーヤーになりつつあります。さらに、デジタルヘルスソリューションとバイオインフォマティクスツールの採用により、データ主導型のバイオマーカー探索が強化され、患者の転帰の改善と医薬品開発プロセスの効率化につながっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 130億米ドル |

| 予測金額 | 418億米ドル |

| CAGR | 12.3% |

同市場は、予測、予後、安全性バイオマーカー、代替エンドポイント、その他など、バイオマーカーのタイプ別に分類されます。2024年にはサロゲートエンドポイントが市場を独占し、総収益シェアの49%を占め、2025年から2034年にかけてCAGR 12.1%で成長すると予測されています。サロゲートバイオマーカーは、研究者が早期に治療効果を評価できるようにすることで、臨床試験プロセスを大幅に迅速化し、臨床試験において重要な役割を果たしています。特に新興市場で広く採用され、米国FDAなどの当局ががんや希少疾患の医薬品承認に強力な規制支援を提供していることが、引き続き市場シェアを押し上げています。

バイオマーカー探索アウトソーシングサービス市場はさらに、ゲノミクス、プロテオミクス、バイオインフォマティクス、その他を含むサービスタイプ別に区分されます。ゲノミクス・バイオマーカー・サービス分野だけでも、2024年には57億米ドルが創出されました。遺伝性疾患患者の増加や、がんや神経変性疾患のような慢性疾患に関連する死亡率の上昇が、ゲノムバイオマーカーサービスの需要に拍車をかけています。ゲノミクス研究に対する官民部門の投資の増加は、ゲノムバイオマーカーの発見と検証を促進し、市場をさらに強化しています。次世代シークエンシング(NGS)やその他の高スループットゲノム技術の統合により、バイオマーカー同定が強化され、より正確な診断や個別化された治療計画が確実になっています。

米国のバイオマーカー探索アウトソーシングサービス市場は、2034年までに185億米ドルに達すると予想されています。バイオテクノロジー分野でのリーダーシップ、高度なヘルスケアインフラ、確立された規制の枠組みが、この分野での優位性に寄与しています。米国FDAはバイオマーカー検証のために厳しいながらも支援的な規制メカニズムを導入しており、診断や医薬品開発プロセスへのバイオマーカーの統合を確実に成功に導いています。バイオ製薬企業、学術研究機関、政府機関の間の継続的なパートナーシップは、技術革新と市場拡大をさらに後押ししています。その結果、米国はバイオマーカー探索アウトソーシングサービスの最前線であり続け、予測期間を通じて世界市場をリードしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 研究開発投資の増加

- 個別化医療と標的療法への注目の高まり

- ハイスループット技術の進歩

- 生物製剤産業の活況

- 業界の潜在的リスク&課題

- 知的財産に関する懸念

- データ・セキュリティ

- 促進要因

- 成長の可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 予測バイオマーカー

- 予後バイオマーカー

- 安全性バイオマーカー

- 代替エンドポイント

- その他のタイプ

第6章 市場推計・予測:サービス別、2021年~2034年

- 主要動向

- ゲノミクスバイオマーカーサービス

- プロテオミクスバイオマーカーサービス

- バイオインフォマティクスバイオマーカーサービス

- その他のバイオマーカーサービス

第7章 市場推計・予測:治療領域別、2021年~2034年

- 主要動向

- がん領域

- 循環器

- 神経

- 自己免疫疾患

- その他の治療領域

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬企業

- バイオテクノロジー企業

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Almac Group Limited

- Biomcare ApS

- Bio-Rad Laboratories

- Crown Bioscience

- Evotec

- Excelra

- Frontage Labs

- ICON

- Integrated DNA Technologies

- Parexel International(MA)Corporation

- RayBiotech

- REPROCELL

- Sino Biological

- Svar Life Science

The Global Biomarker Discovery Outsourcing Services Market was valued at USD 13 billion in 2024 and is projected to expand at a CAGR of 12.3% between 2025 and 2034. The market is witnessing significant growth, driven by the increasing incidence of chronic diseases, rapid advancements in omics technologies, and rising investments in research and development within the pharmaceutical and biotechnology sectors. The growing emphasis on personalized medicine is further fueling demand for novel biomarkers that enable early detection, diagnosis, and monitoring of chronic conditions such as cancer, cardiovascular diseases, and diabetes. With chronic disease prevalence on the rise worldwide, the demand for biomarkers to facilitate targeted treatment strategies continues to increase.

Rising government initiatives, collaborations between pharmaceutical companies and research organizations, and regulatory support for biomarker validation are accelerating market expansion. The increasing adoption of artificial intelligence (AI) and machine learning (ML) in biomarker discovery is also transforming the industry, allowing for faster identification and validation of potential biomarkers. Emerging economies are becoming key players in biomarker research due to rising healthcare expenditures and the establishment of advanced clinical research centers. Additionally, the adoption of digital health solutions and bioinformatics tools is enhancing data-driven biomarker discovery, leading to improved patient outcomes and more efficient drug development processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13 Billion |

| Forecast Value | $41.8 Billion |

| CAGR | 12.3% |

The market is categorized into different biomarker types, including predictive, prognostic, safety biomarkers, surrogate endpoints, and others. Surrogate endpoints dominated the market in 2024, accounting for 49% of the total revenue share, and are expected to grow at a CAGR of 12.1% from 2025 to 2034. Surrogate biomarkers play a crucial role in clinical trials by enabling researchers to assess treatment efficacy early, significantly expediting the clinical study process. Their widespread adoption, particularly in emerging markets, and strong regulatory support from authorities such as the U.S. FDA for drug approvals in oncology and rare diseases continue to drive their market share.

The biomarker discovery outsourcing services market is further segmented by service type, which includes genomics, proteomics, bioinformatics, and others. The genomics biomarker services segment alone generated USD 5.7 billion in 2024. Increasing cases of genetic disorders and the rising mortality rates associated with chronic diseases like cancer and neurodegenerative conditions are fueling the demand for genomic biomarker services. Growing public and private sector investments in genomics research are expediting the discovery and validation of genomic biomarkers, further strengthening the market. The integration of next-generation sequencing (NGS) and other high-throughput genomic technologies is enhancing biomarker identification, ensuring more precise diagnostics and personalized treatment plans.

The U.S. Biomarker Discovery Outsourcing Services Market is expected to reach USD 18.5 billion by 2034. The country's leadership in the biotechnology sector, advanced healthcare infrastructure, and well-established regulatory framework are contributing to its dominance in this space. The U.S. FDA has implemented stringent yet supportive regulatory mechanisms for biomarker validation, ensuring the successful integration of biomarkers into diagnostics and drug development processes. Ongoing partnerships between biopharmaceutical companies, academic research institutions, and government agencies are further propelling innovation and market expansion. As a result, the U.S. remains at the forefront of biomarker discovery outsourcing services, leading the global market throughout the forecast period.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising investments in research and development

- 3.2.1.2 Increasing focus on personalized medicine and targeted therapies

- 3.2.1.3 Advancements in high-throughput technologies

- 3.2.1.4 Booming biologics industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Intellectual property concerns

- 3.2.2.2 Data security

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Predictive biomarkers

- 5.3 Prognostic biomarkers

- 5.4 Safety biomarkers

- 5.5 Surrogate endpoints

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Service, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Genomics biomarker services

- 6.3 Proteomics biomarker services

- 6.4 Bioinformatics biomarker services

- 6.5 Other biomarker services

Chapter 7 Market Estimates and Forecast, By Therapeutic Area, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oncology

- 7.3 Cardiology

- 7.4 Neurology

- 7.5 Autoimmune diseases

- 7.6 Other therapeutic areas

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical companies

- 8.3 Biotechnology companies

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Almac Group Limited

- 10.2 Biomcare ApS

- 10.3 Bio-Rad Laboratories

- 10.4 Crown Bioscience

- 10.5 Evotec

- 10.6 Excelra

- 10.7 Frontage Labs

- 10.8 ICON

- 10.9 Integrated DNA Technologies

- 10.10 Parexel International (MA) Corporation

- 10.11 RayBiotech

- 10.12 REPROCELL

- 10.13 Sino Biological

- 10.14 Svar Life Science