|

市場調査レポート

商品コード

1699358

住宅用自動モータスタータ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Residential Automatic Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 住宅用自動モータスタータ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

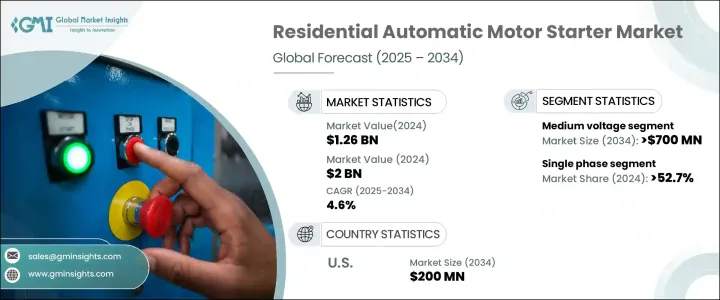

住宅用自動モータスタータの世界市場は、2024年には12億6,000万米ドルとなり、2025年から2034年にかけてCAGR 4.6%で成長すると予測されています。

この着実な拡大は、エネルギー効率への注目の高まりと、信頼性が高くコンパクトで使いやすい電気ソリューションへの需要の高まりを反映しています。より多くの住宅所有者がスマートライフに移行するにつれて、最新の住宅セットアップにシームレスに統合する高度なモータースタータのニーズは高まり続けています。消費者は、利便性を向上させ、エネルギー消費を削減し、持続可能性の動向に沿った機器をますます優先するようになっています。

都市化と急速な市場開拓は市場をさらに活性化させ、不動産所有者と建設業者は効率的な電源管理ソリューションを積極的に求めています。ホームオートメーションシステムの採用は、安全性を確保しながら電気性能を最適化できるインテリジェント・モータスタータの需要を押し上げています。さらに、エネルギー効率を支援する規制政策が、これらのシステムの展開を加速しています。スマートモニタリング機能や耐久性の向上などの技術的進歩により、これらのスタータは住宅用アプリケーションとしてより魅力的になっています。住宅部門が高性能、省スペース、環境に優しい電気インフラに焦点を当てて進化するにつれて、自動モータースタータの需要は世界中で急増し続けると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 12億6,000万米ドル |

| 予測金額 | 20億米ドル |

| CAGR | 4.6% |

市場は電圧によって低電圧、中電圧、高電圧のセグメントに分類されます。なかでも、中電圧セグメントは大きな成長が見込まれており、2034年までに7億米ドルを生み出すと予測されています。これらのシステムは、その効率性、コンパクトな設計、簡単な設置がますます認知され、近代的な住宅設備に理想的なものとなっています。省スペースで簡素化された電気ソリューションを求める住宅所有者は、中電圧モータースタータを好んでおり、さまざまな地域での普及をさらに促進しています。

位相別では、住宅用自動モータスタータ市場は単相システムと三相システムに分けられます。単相モータスタータは2024年に52.7%の圧倒的シェアを占め、需要は着実に増加すると予想されます。スマートホームの人気の高まり、持続可能性の重視の高まり、エネルギー効率の高い電気ソリューションの必要性などが、この動向の主な要因となっています。家庭が信頼性を損なうことなくエネルギー消費を最適化することを目指しているため、単相スタータは最新の電気システムにとって費用対効果の高い選択肢として浮上しています。

米国の住宅用自動モータスタータ市場は、エネルギー効率の高いスマートソリューションの採用増加により、2034年までに2億米ドルに達する勢いです。都市化の急速な進展、住宅の新築ブーム、効率的な電力管理への注目の高まりにより、先進的なモータースタータへの需要が高まっています。住宅所有者も建設業者も同様に、これらのシステムを最新の住宅に組み込むことの利点を認識しており、安全性と利便性を高めながら最適な電力使用を保証しています。市場が進化するにつれて、持続可能な住宅インフラの形成における自動モータースタータの役割は、ますます顕著になっていくと思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 低電圧

- 中電圧

- 高電圧

第6章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- オランダ

- オーストリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- ペルー

- アルゼンチン

第8章 企業プロファイル

- ABB

- C&S Electric

- CHINT Group

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric

- Havells India

- L&T Electrical and Automation

- Lovato Electric

- Mitsubishi Electric

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-Bentex Group

- WEG

The Global Residential Automatic Motor Starter Market was valued at USD 1.26 billion in 2024 and is projected to grow at a CAGR of 4.6% between 2025 and 2034. This steady expansion reflects the rising focus on energy efficiency and the increasing demand for reliable, compact, and user-friendly electrical solutions. As more homeowners shift toward smart living, the need for advanced motor starters that seamlessly integrate with modern residential setups continues to rise. Consumers are increasingly prioritizing devices that enhance convenience, reduce energy consumption, and align with sustainability trends.

Urbanization and rapid residential development further fuel the market, with property owners and builders actively seeking efficient power management solutions. The adoption of home automation systems is pushing demand for intelligent motor starters capable of optimizing electrical performance while ensuring safety. Additionally, regulatory policies supporting energy efficiency are accelerating the deployment of these systems. Technological advancements, including smart monitoring features and enhanced durability, are making these starters more attractive for residential applications. As the residential sector evolves with a focus on high-performance, space-saving, and eco-friendly electrical infrastructure, the demand for automatic motor starters will continue to surge worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.26 Billion |

| Forecast Value | $2 Billion |

| CAGR | 4.6% |

The market is categorized based on voltage into low, medium, and high-voltage segments. Among these, the medium-voltage segment is poised for significant growth, projected to generate USD 700 million by 2034. These systems are increasingly recognized for their efficiency, compact design, and easy installation, making them ideal for modern residential setups. Homeowners looking for space-saving and simplified electrical solutions are favoring medium-voltage motor starters, further driving their adoption across various regions.

In terms of phase, the residential automatic motor starter market is divided into single-phase and three-phase systems. Single-phase motor starters held a dominant 52.7% share in 2024, with demand expected to rise steadily. The growing popularity of smart homes, the heightened emphasis on sustainability, and the need for energy-efficient electrical solutions are all key contributors to this trend. As households aim to optimize energy consumption without compromising reliability, single-phase starters are emerging as a cost-effective choice for modern electrical systems.

The United States residential automatic motor starter market is on track to reach USD 200 million by 2034, driven by the increasing adoption of energy-efficient smart solutions. With a surge in urbanization, a boom in new residential construction, and a heightened focus on efficient power management, the demand for advanced motor starters is rising. Homeowners and builders alike are recognizing the benefits of integrating these systems into modern homes, ensuring optimal electricity usage while enhancing safety and convenience. As the market evolves, the role of automatic motor starters in shaping sustainable residential infrastructure will only become more prominent.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 C&S Electric

- 8.3 CHINT Group

- 8.4 Danfoss

- 8.5 Eaton

- 8.6 Emerson Electric

- 8.7 Fuji Electric

- 8.8 Havells India

- 8.9 L&T Electrical and Automation

- 8.10 Lovato Electric

- 8.11 Mitsubishi Electric

- 8.12 Rockwell Automation

- 8.13 Schneider Electric

- 8.14 Siemens

- 8.15 SKN-Bentex Group

- 8.16 WEG