|

市場調査レポート

商品コード

1699312

データセンターチップ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Data Center Chip Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| データセンターチップ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月20日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

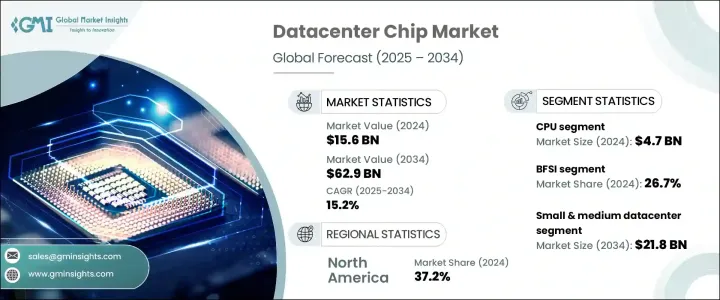

世界のデータセンターチップ市場は、2024年に156億米ドルと評価され、2025年から2034年の間に15.2%の堅調なCAGRを反映すると予測されています。

成長の原動力は、人工知能(AI)、機械学習(ML)、高性能コンピューティングに対する需要の高まりです。企業がデジタルトランスフォーメーションを受け入れ続ける中、高度なデータ処理能力へのニーズはかつてないほど高まっています。組織はクラウドベースのプラットフォームに移行し、AI主導のアナリティクスに依存し、膨大な量のデータを効率的に管理するために高度なコンピューティング・ソリューションを導入しています。こうした進歩がデータセンター・チップ技術の拡大に拍車をかけ、最新のコンピューティング・インフラに不可欠なコンポーネントとなっています。

5Gネットワークの急速な展開、データトラフィックの増大、クラウドサービスへの依存度の高まりは、市場の需要を加速させています。企業は、コンピューティングパワーを最適化し、エネルギー効率を高め、データ処理の待ち時間を短縮するために、次世代チップに多額の投資を行っています。リアルタイム処理が重要なエッジコンピューティングへのシフトは、最先端チップ技術の必要性をさらに強調しています。データ集約型アプリケーションが業界全体の主流になりつつある中、半導体メーカーは優れた処理能力、電力効率の向上、セキュリティ機能の強化を備えたチップの設計に注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 156億米ドル |

| 予測金額 | 629億米ドル |

| CAGR | 15.2% |

同市場は、中央演算処理装置(CPU)、グラフィックス・プロセッシング・ユニット(GPU)、フィールド・プログラマブル・ゲート・アレイ(FPGA)、特定用途向け集積回路(ASIC)、その他など、チップの種類によって区分されます。CPUは、クラウドコンピューティングの採用拡大、ITインフラストラクチャの仮想環境への移行、AIアプリケーションによる計算需要の増大が原動力となり、2024年に47億米ドルを生み出しました。現代のコンピューティングのバックボーンとして、CPUはシームレスなシステム運用を可能にし、企業ソフトウェアからデータ分析まであらゆるものをサポートします。特にAIベースのワークロードが業界全体で拡大するにつれて、高速処理能力に対する需要は急増し続けています。

業界別では、データセンター・チップ市場は、BFSI、政府、IT・通信、運輸、エネルギー・公益事業、その他の分野で高い採用率を示しています。BFSI部門は、安全で高速なデータ処理へのニーズとブロックチェーン技術の採用増加により、2024年の市場シェアの26.7%を占めました。フィンテック企業やデジタル・バンキング・プラットフォームが急速に拡大する中、金融サービスにおける高度なチップ技術の需要はかつてないほど高まっています。データセンター用チップは、トランザクションの安全性を確保し、ダウンタイムを最小限に抑え、金融機関全体の業務効率を高める上で極めて重要な役割を果たしています。

北米は、AI、機械学習、クラウドコンピューティングへの多額の投資に牽引され、2024年の世界市場で37.2%のシェアを占めました。米国は44億米ドルの市場収益を占め、2034年までのCAGRは15.4%と予測されます。同国は、半導体製造、AI駆動コンピューティング、リアルタイムデータ処理に力を入れており、世界のデータセンターチップランドスケープにおける主要プレーヤーとして位置付けられています。クラウドの採用や半導体研究開発における政府の取り組みが増え続ける中、北米は進化する市場でのリーダーシップを維持することになります。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- AIと機械学習の需要急増

- エネルギー効率と持続可能性の重視

- ハイパースケールデータセンターとクラウドコンピューティング

- 5Gインフラの急速な拡大

- ストレージ需要の増大とデータ分析

- 促進要因

- 業界の潜在的リスク&課題

- 急速な技術革新

- サプライチェーンの混乱

- 規制状況

- 技術動向

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:チップタイプ別、2021年~2034年

- 主要動向

- 中央演算処理装置(CPU)

- グラフィックス・プロセッシング・ユニット(GPU)

- FPGA(フィールド・プログラマブル・ゲート・アレイ)

- 特定用途向け集積回路(ASIC)

- その他

第6章 市場推計・予測:産業別、2021年~2034年

- 主要動向

- BFSI

- 政府機関

- IT・通信

- 運輸

- エネルギー・公益事業

- その他

第7章 市場推計・予測:データセンター規模別、2021年~2034年

- 主要動向

- 中小規模

- 大規模

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Advanced Micro Devices

- Broadcom

- GlobalFoundries

- Huawei Technologies

- Intel

- MediaTek

- Micron Technology

- Microsoft

- NVIDIA

- Qualcomm Technologies

- Samsung Electronics

- SK Hynix

- Taiwan Semiconductor Manufacturing Company

The Global Data Center Chip Market was valued at USD 15.6 billion in 2024 and is projected to reflect a robust CAGR of 15.2% between 2025 and 2034. The growth is fueled by the rising demand for artificial intelligence (AI), machine learning (ML), and high-performance computing. As businesses continue to embrace digital transformation, the need for advanced data processing capabilities has never been greater. Organizations are shifting to cloud-based platforms, relying on AI-driven analytics, and deploying sophisticated computing solutions to manage vast volumes of data efficiently. These advancements are fueling the expansion of data center chip technologies, making them essential components in modern computing infrastructures.

The rapid deployment of 5G networks, growing data traffic, and increasing reliance on cloud services are accelerating market demand. Enterprises are heavily investing in next-generation chips to optimize computing power, enhance energy efficiency, and reduce latency in data processing. The shift toward edge computing, where real-time processing is critical, further underscores the necessity of cutting-edge chip technologies. With data-intensive applications becoming mainstream across industries, semiconductor manufacturers are focusing on designing chips with superior processing capabilities, improved power efficiency, and enhanced security features.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.6 Billion |

| Forecast Value | $62.9 Billion |

| CAGR | 15.2% |

The market is segmented by chip type, including central processing units (CPU), graphics processing units (GPU), field-programmable gate arrays (FPGA), application-specific integrated circuits (ASIC), and others. CPUs generated USD 4.7 billion in 2024, driven by the increasing adoption of cloud computing, the migration of IT infrastructure to virtual environments, and growing computational demands from AI applications. As the backbone of modern computing, CPUs enable seamless system operations, supporting everything from enterprise software to data analytics. The demand for high-speed processing power continues to surge, particularly as AI-based workloads expand across industries.

Based on industry verticals, the data center chip market is witnessing high adoption across BFSI, government, IT and telecom, transportation, energy and utility, and other sectors. The BFSI sector accounted for 26.7% of the market share in 2024, fueled by the need for secure, high-speed data processing and the increasing adoption of blockchain technology. With fintech companies and digital banking platforms expanding rapidly, the demand for advanced chip technologies in financial services is at an all-time high. Data center chips play a pivotal role in ensuring transaction security, minimizing downtime, and enhancing overall operational efficiency for financial institutions.

North America dominated the global market with a 37.2% share in 2024, led by substantial investments in AI, machine learning, and cloud computing. The United States accounted for USD 4.4 billion in market revenue and is projected to grow at a CAGR of 15.4% through 2034. The country's strong focus on semiconductor manufacturing, AI-driven computing, and real-time data processing positions it as a key player in the global data center chip landscape. As cloud adoption and government initiatives in semiconductor R&D continue to rise, North America is set to maintain its leadership in the evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in Demand for AI & Machine Learning

- 3.2.1.2 Focus on Energy-Efficiency & Sustainability

- 3.2.1.3 Hyperscale Data Centres & Cloud Computing

- 3.2.1.4 Rapid Expansion of 5G Infrastructure

- 3.2.1.5 Growing Storage Demands and Data Analytics

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1.1 Rapid Technological Changes

- 3.3.1.2 Supply Chain Disruptions

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Chip Type, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Central Processing Unit (CPU)

- 5.3 Graphics Processing Unit (GPU)

- 5.4 Field-Programmable Gate Array (FPGA)

- 5.5 Application Specific Integrated Circuit (ASIC)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Vertical Industry, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 BFSI

- 6.3 Government

- 6.4 IT and telecom

- 6.5 Transportation

- 6.6 Energy & utilities

- 6.7 Other

Chapter 7 Market Estimates and Forecast, By Data Center Size, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Small and medium size

- 7.3 Large size

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Advanced Micro Devices

- 9.2 Broadcom

- 9.3 Google

- 9.4 GlobalFoundries

- 9.5 Huawei Technologies

- 9.6 Intel

- 9.7 MediaTek

- 9.8 Micron Technology

- 9.9 Microsoft

- 9.10 NVIDIA

- 9.11 Qualcomm Technologies

- 9.12 Samsung Electronics

- 9.13 SK Hynix

- 9.14 Taiwan Semiconductor Manufacturing Company