|

市場調査レポート

商品コード

1699282

炭素回収・貯留市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Carbon Capture and Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 炭素回収・貯留市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月19日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

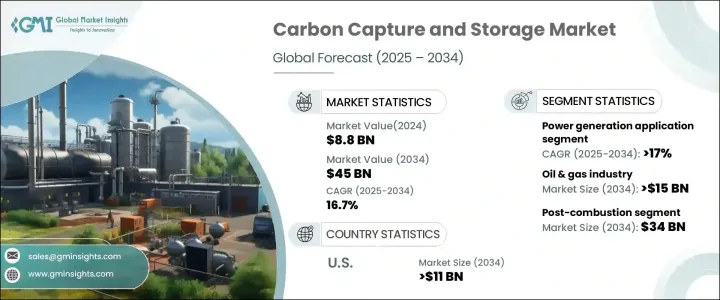

世界の炭素回収・貯留市場の2024年の市場規模は88億米ドルで、2025年から2034年にかけて16.7%のCAGRで成長すると予測されています。

温室効果ガスの排出を抑制し、脱炭素化目標を達成する緊急性が高まっていることが、CCS技術への大きな投資を促しています。世界各国政府は厳しい環境規制を実施しており、産業界はコンプライアンス基準を満たし、二酸化炭素排出量を削減するために、先進的な炭素回収ソリューションを導入する必要に迫られています。気候変動に対する懸念の高まりは、急速な産業拡大やエネルギー需要と相まって、費用対効果の高い排出抑制技術の必要性をさらに高めています。

エネルギー、化学、製造の各分野の企業は、世界の持続可能性イニシアティブに沿うため、CCSソリューションを積極的に事業に組み込んでいます。クリーンエネルギーへの移行への注目の高まりは、炭素回収効率の進歩と相まって、市場拡大の新たな機会を引き出しています。さらに、研究開発活動の活発化が、拡張性と運用可能性を高める次世代CCS技術の革新を促進しています。産業界が環境への責任と経済成長の両立を目指す中、CCSは長期的なカーボンニュートラル達成のための極めて重要なソリューションとして台頭しつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 88億米ドル |

| 予測金額 | 450億米ドル |

| CAGR | 16.7% |

市場は技術によって、燃焼前、酸素燃焼、燃焼後に区分されます。燃焼後回収技術は大幅な成長が見込まれ、2034年までに340億米ドルに達すると予測されています。この技術は、既存の産業設備とのシームレスな統合により、発電所、製油所、製造施設での大規模な採用を可能にし、支持を集めています。排ガス規制が優先課題となる中、燃焼後システムは効率と費用対効果を高めて進化しており、実行可能な炭素削減戦略を求める産業にとって魅力的な選択肢となっています。革新的な吸収剤と高度なろ過技術の開発は、燃焼後技術の性能と採用をさらに後押しし、一貫した市場拡大を確実なものにしています。

用途別では、市場は発電、化学処理、石油・ガスなどの産業にまたがっています。発電分野は2024年に36%のシェアを獲得し、2034年まで17%のCAGRで成長すると予想されています。水素の生産、貯蔵、流通を促進するCCSインフラの導入が増加していることは、この分野での需要を促進する重要な要因です。世界のエネルギー消費量の増加が続く中、政府や公益事業者は、エネルギー生産量を損なうことなく排出量目標を達成するため、CCSの導入を優先しています。発電所はCCSソリューションを活用して従来のエネルギーシステムを改修し、運転効率を維持しながら厳格な環境政策へのコンプライアンスを確保しています。再生可能エネルギー・プロジェクトやカーボン・マイナス・イニシアチブにおけるCCSの統合は、進化するエネルギー情勢におけるCCSの役割をさらに確固たるものにしています。

米国市場は2024年に33億米ドルを生み出し、2034年には110億米ドルに達すると予測されています。二酸化炭素排出量の削減とエネルギー・インフラの近代化を重視する国の姿勢が、CCS投資を加速させています。排出制御システムの技術的進歩は、大規模CCSプロジェクトに対する多額の資金調達と相まって、国全体の市場成長を牽引しています。北米は依然としてCCS拡大の主要地域であり、戦略的パートナーシップと政府のインセンティブが技術革新と展開の促進に重要な役割を果たしています。産業界がよりクリーンな生産方法を追求する中、米国市場は力強い成長を遂げ、世界のCCS情勢におけるリーダーシップを強化することになると思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 燃焼前

- 燃焼後

- 酸素燃焼

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 石油・ガス

- 化学処理

- 発電

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- デンマーク

- スウェーデン

- アジア太平洋

- 中国

- オーストラリア

- 韓国

- 世界のその他の地域

第8章 企業プロファイル

- Air Products

- Aker Solutions

- Carbon Clean

- Chevron

- Dakota Gasification Company

- Equinor

- Exxon Mobil

- Fluor

- General Electric

- Halliburton

- Linde

- Mitsubishi Heavy Industries

- NRG Energy

- Shell Cansolv

- Siemens

- SLB

- Sulzer

- TotalEnergies

The Global Carbon Capture And Storage Market was valued at USD 8.8 billion in 2024 and is projected to grow at a CAGR of 16.7% between 2025 and 2034. The increasing urgency to curb greenhouse gas emissions and achieve decarbonization goals is driving significant investments in CCS technologies. Governments worldwide are implementing stringent environmental regulations, compelling industries to adopt advanced carbon capture solutions to meet compliance standards and mitigate their carbon footprint. Rising concerns over climate change, combined with the rapid industrial expansion and energy demands, are further propelling the need for cost-effective emission control technologies.

Companies across the energy, chemical, and manufacturing sectors are actively integrating CCS solutions into their operations to align with global sustainability initiatives. The growing focus on clean energy transition, coupled with advancements in carbon capture efficiency, is unlocking new opportunities for market expansion. Additionally, increasing research and development activities are fostering the innovation of next-generation CCS technologies that enhance scalability and operational feasibility. As industries strive to balance environmental responsibility with economic growth, CCS is emerging as a pivotal solution for achieving long-term carbon neutrality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $45 Billion |

| CAGR | 16.7% |

The market is segmented based on technology into pre-combustion, oxy-fuel combustion, and post-combustion. Post-combustion capture technology is expected to witness substantial growth, with forecasts indicating it will reach USD 34 billion by 2034. This technology is gaining traction due to its seamless integration with existing industrial setups, enabling large-scale adoption across power plants, refineries, and manufacturing facilities. As emission control becomes a priority, post-combustion systems are evolving with enhanced efficiency and cost-effectiveness, making them an attractive option for industries seeking viable carbon reduction strategies. The development of innovative absorbents and advanced filtration techniques is further boosting the performance and adoption of post-combustion technology, ensuring consistent market expansion.

In terms of application, the market spans power generation, chemical processing, and oil & gas, among other industries. The power generation segment captured a 36% share in 2024 and is expected to grow at a CAGR of 17% through 2034. The increasing deployment of CCS infrastructure to facilitate hydrogen production, storage, and distribution is a crucial factor fueling demand within this sector. As global energy consumption continues to rise, governments and utility providers are prioritizing CCS adoption to meet emission targets without compromising energy output. Power plants are leveraging CCS solutions to retrofit conventional energy systems, ensuring compliance with strict environmental policies while maintaining operational efficiency. The integration of CCS in renewable energy projects and carbon-negative initiatives is further solidifying its role in the evolving energy landscape.

The U.S. market generated USD 3.3 billion in 2024 and is projected to reach USD 11 billion by 2034. The nation's emphasis on reducing carbon emissions and modernizing energy infrastructure is accelerating CCS investments. Technological advancements in emission control systems, coupled with substantial funding for large-scale CCS projects, are driving market growth across the country. North America remains a key region for CCS expansion, with strategic partnerships and government incentives playing a vital role in fostering innovation and deployment. As industries strive for cleaner production methods, the U.S. market is set to experience robust growth, reinforcing its leadership in the global CCS landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (MTPA, USD Billion)

- 5.1 Key trends

- 5.2 Pre combustion

- 5.3 Post combustion

- 5.4 Oxy-Fuel combustion

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (MTPA, USD Billion)

- 6.1 Key trends

- 6.2 Oil and gas

- 6.3 Chemical processing

- 6.4 Power generation

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (MTPA, USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 Denmark

- 7.3.4 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 South Korea

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Air Products

- 8.2 Aker Solutions

- 8.3 Carbon Clean

- 8.4 Chevron

- 8.5 Dakota Gasification Company

- 8.6 Equinor

- 8.7 Exxon Mobil

- 8.8 Fluor

- 8.9 General Electric

- 8.10 Halliburton

- 8.11 Linde

- 8.12 Mitsubishi Heavy Industries

- 8.13 NRG Energy

- 8.14 Shell Cansolv

- 8.15 Siemens

- 8.16 SLB

- 8.17 Sulzer

- 8.18 TotalEnergies