ノートパソコン市場の機会、成長促進要因、業界動向分析、予測、2026年~2035年

Laptop Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 2027524

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

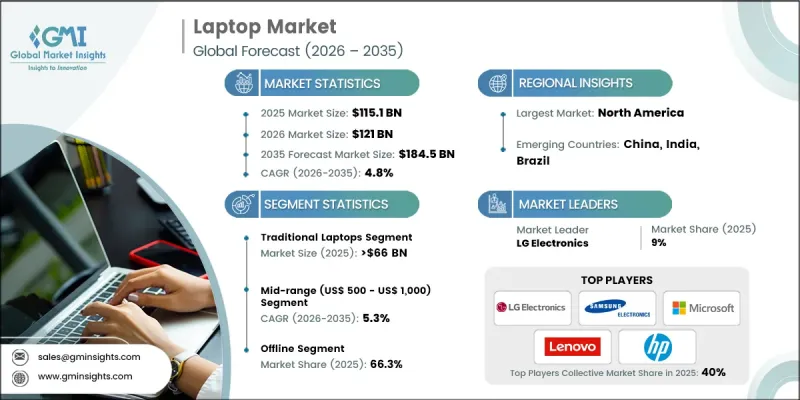

世界のノートパソコン市場は、2025年に1,151億米ドルと評価され、CAGR4.8%で成長し、2035年までに1,845億米ドルに達すると推定されています。

市場の拡大は、リモートワークモデルの普及、ハイブリッド学習環境の拡大、そして高性能かつ接続性に優れたポータブルコンピューティングデバイスへの依存度の高まりによって牽引されています。消費者も企業も同様に、シームレスなマルチタスク、高速処理、効率的な電力管理を実現する高度なノートパソコンを求めています。主要メーカー間の戦略的な合併や買収を通じて競合情勢は変化しており、これにより各社は製品ポートフォリオを拡大し、技術力を強化することが可能になっています。この業界再編は、標準的なノートパソコン、コンバーチブルデバイス、ゲーミングシステム、ウルトラポータブルモデルなど、複数のカテゴリーにわたるイノベーションを加速させています。プロセッサ技術、バッテリー効率、統合ソフトウェアエコシステムの継続的な進歩が、需要をさらに後押ししています。業界全体でデジタルトランスフォーメーションが加速する中、ノートパソコンは生産性、コミュニケーション、エンターテインメントに不可欠なツールとなりつつあり、多様なユーザー層におけるその重要性を高め、長期的な市場成長を牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始金額 | 1,151億米ドル |

| 予測金額 | 1,845億米ドル |

| CAGR | 4.8% |

インテリジェントかつ高性能なコンピューティングソリューションへの移行により、市場における製品への期待が再定義されています。機能に制限のある従来のノートパソコンは、AI対応プロセッサ、クラウド統合、およびバッテリー駆動時間の延長を特徴とする先進的なシステムに徐々に置き換えられています。これらの革新により、ユーザーはパーソナライズされたコンピューティング体験、複数のデバイス間での接続性の向上、そして様々なタスクに対する最適化されたパフォーマンスの恩恵を受けることができます。ノートパソコンは携帯性、効率性、そして複雑なワークロードを容易に処理できる能力を備えているため、専門家、学生、ゲーマーからの需要の高まりが、その普及を後押しし続けています。

従来のノートパソコン市場は2025年に660億米ドルの規模となり、2035年までに1,003億米ドルに達すると予測されています。このセグメントは、企業ユーザー、教育機関、そして信頼性の高いコンピューティングソリューションを求めるコスト意識の高い消費者からの安定した需要により、依然として支配的な地位を維持しています。馴染みのあるデザイン、耐久性、そして幅広い価格帯での入手可能性が、持続的な成長に寄与しています。従来のノートパソコンは、日々のコンピューティングニーズに対する実用的な選択肢であり続け、新しいフォームファクターの登場にもかかわらず、その重要性を維持しています。

オフライン流通セグメントは2025年に66.3%のシェアを占め、2035年までCAGR4.5%で成長すると予想されています。実店舗は、製品を実際に手に取って体験できる機会、個別対応のサポート、そして即時の商品入手可能性を提供することで、購入プロセスにおいて引き続き重要な役割を果たしています。これらの利点は、特に製造品質、キーボードの操作感、ディスプレイの性能といった機能を評価する際、消費者が十分な情報に基づいた判断を下すのに役立ちます。オフラインチャネルは、法人顧客や初めてノートパソコンを購入するユーザーにとって特に重要であり、店舗への来客数の維持と堅調な販売実績に貢献しています。

米国のノートパソコン市場は2025年に319億米ドルに達し、同地域で最も安定し、かつ高成長を遂げている市場の一つとしての地位を維持しています。堅調な個人消費、デジタル技術の広範な普及、そして頻繁な技術アップグレードが、市場の継続的な拡大を支えています。プレミアムデバイス、ゲーミングノートパソコン、プロフェッショナル向けシステム、コンバーチブルモデルに対する需要は依然として高い水準にあります。確立された小売ネットワークと堅調なeコマースエコシステムの存在が市場の成長をさらに後押しする一方、高度なコンピューティングソリューションへの関心の高まりが、イノベーションと普及を牽引し続けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 成長促進要因

- リモートワークおよびハイブリッド学習ソリューションへの需要の高まり

- 急速な技術の進歩

- クラウドコンピューティングとデジタルエコシステムの拡大

- 業界の潜在的リスク&課題

- 激しい競合圧力と価格への敏感さ

- 製品の急速な陳腐化

- 機会

- DaaS(device-as-a-service)への需要の高まり

- AIファーストおよびコネクテッド・エコシステムへの移行

- 成長促進要因

- 成長可能性分析

- 今後の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別の規制枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

- 貿易データ分析

- 輸出入の数量・金額動向

- 主要貿易ルートと関税の影響

- 地域別貿易政策の影響(米国と中国の貿易の動向)

- 市場に対するAIおよび生成AIの影響

- AIによる既存ビジネスモデルの変革

- 製品開発のための予測分析

- インフラおよび導入状況(1次調査に基づく)

- 地域別・購入者セグメント別の導入普及率(1次調査に基づく)

- スケーラビリティの制約とインフラ投資の動向(1次調査に基づく)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 ノートパソコン市場推計・予測:製品タイプ別、2022年~2035年

- 従来型ノートパソコン

- 2-in-1ノートパソコン

第6章 ノートパソコン市場推計・予測:画面サイズ別、2022年~2035年

- 10.9インチ以下

- 11~14.9インチ

- 15~16.9インチ

- 17インチ以上

第7章 ノートパソコン市場推計・予測:価格帯別、2022年~2035年

- エコノミー(500米ドル以下)

- ミドルレンジ(500~1,000米国ドル)

- ハイエンド(1,000米ドル以上)

第8章 ノートパソコン市場推計・予測:最終用途別、2022年~2035年

- 個人向け

- 商業用

- 企業向け

- ゲーミング

- 教育機関

- BFSI

- その他(小売店、クリエイティブスタジオなど)

- 産業用

第9章 ノートパソコン市場推計・予測:流通チャネル別、2022年~2035年

- オンライン

- eコマースサイト

- 企業ウェブサイト

- オフライン

- マルチブランド店

- 百貨店

- 専門店

- その他の小売店

第10章 市場推計・予測:地域別、2022年~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Acer

- Apple Inc.

- ASUSTeK Computer Inc.

- Dell Inc.

- Haier Inc.

- HP Inc.

- Huawei Device Co., Ltd.

- Lenovo

- LG Electronics

- Microsoft

- Micro-Star INT'L CO., LTD.

- Razer Inc.

- SAMSUNG

- SONY ELECTRONICS INC.

- Toshiba Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日