|

市場調査レポート

商品コード

1698295

自動車用ヒューズ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Fuse Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ヒューズ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月17日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

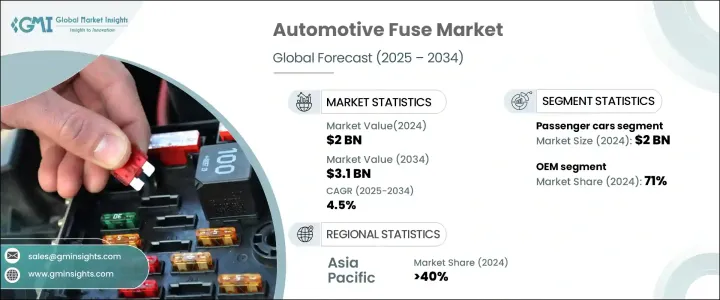

自動車用ヒューズの世界市場は、2024年に20億米ドルと評価され、2025年から2034年にかけてCAGR 4.5%で成長すると予測されています。

自動車業界が電気自動車生産へのシフトを加速させる中、高性能ヒューズの需要が高まっています。自動車生産台数が前年比10.3%増加する中、自動車メーカーは電気部品の統合が進むのをサポートする高度な回路保護ソリューションを求めています。規制機関は堅牢な電気安全システムを義務付けており、ヒューズは短絡、過熱、電気故障の防止に不可欠です。

ヒューズ技術の急速な進歩により、特に高電圧の電気自動車ではシステム保護が強化されています。各メーカーは、急速充電環境や過酷な条件に耐える耐久性のあるヒューズの開発に注力しています。研究開発の目的は、ヒューズの効率を高め、進化する安全規制への準拠を確実にすることです。自動車メーカーは、車両の電子機器を保護し、電力管理をサポートし、全体的な信頼性を向上させる革新的なヒューズを採用しており、市場は大きく成長しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 20億米ドル |

| 予測金額 | 31億米ドル |

| CAGR | 4.5% |

ADAS(先進運転支援システム)、デジタルダッシュボード、電動パワーステアリングの導入が進むにつれ、より高速応答のヒューズに対するニーズが高まっています。高性能ヒューズ・ソリューションへの投資により、自動車の電気部品を保護しつつ、新たな安全基準への準拠が保証されます。従来のヒューズからスマートヒューズへの移行により、遠隔診断機能が導入され、電気負荷を監視して故障を防止することで安全性が向上します。このようなインテリジェントヒューズは、最適な性能のために効率的な電力管理に依存する電気自動車やコネクテッドカーに有益です。

自動車メーカーはヒューズメーカーと協力し、スマートヒューズ技術を最新の車両アーキテクチャに統合しています。デジタル化は新たな機会を育み、自動車回路保護を最適化します。電動パワートレインへの移行には、熱管理を強化し電気的リスクを防止しながら、高電圧および電流負荷に対応できるヒューズが必要です。こうした進歩は電気自動車やハイブリッド車の急速な普及を促し、高性能ヒューズはその開発に不可欠なものとなっています。

メーカーは車両の信頼性を高めるためにスマートヒューズ技術に投資し、リアルタイムの故障検出と予知保全を行っています。インテリジェントヒューズは電気システムの問題を即座に報告し、安全性を向上させ、ダウンタイムを最小限に抑えます。自動車メーカーはこれらのヒューズを最新の車両電子機器に統合することで、メンテナンス作業を合理化し、継続的な監視を保証することで、安全性と性能を強化しています。

自動車メーカーはサプライヤーと協力し、特定の車両構造や運用要件に合わせてカスタマイズされたヒューズシステムを開発しています。最適化された電気保護により、車両性能の向上、寿命の延長、メンテナンスコストの削減が実現します。カスタマイズされたヒューズ設計は、厳格な安全規制の遵守を確保しつつ、高度な電力システムをサポートします。

市場は燃料タイプ別にガソリン車、ディーゼル車、全電気自動車、ハイブリッド車、燃料電池車に区分されます。ガソリン・セグメントは予測期間を通じて大幅な成長が見込まれます。電気自動車の台頭にもかかわらず、ガソリン車が依然として主流であるため、従来型の高性能ヒューズの需要が維持されています。これらのヒューズは、イグニッション、燃料噴射、照明システムなどの主要な電気部品を保護します。

ヒューズタイプによって、市場はブレードヒューズ、ガラスヒューズ、スローブローヒューズ、EVヒューズ、その他に分類されます。ブレードヒューズは、その互換性、費用対効果、交換の容易さにより、2024年に最大の市場シェアを占めました。従来の自動車と電気自動車の両方で広く採用されていることから、回路保護における信頼性が裏付けられています。EVの普及が進むにつれ、バッテリー管理および配電システムをサポートするために、電圧および電流容量が強化されたブレードヒューズが開発されています。

アジア太平洋地域は、自動車生産台数の増加と消費者需要の高まりにより、力強い市場成長を遂げています。電動モビリティに対する政府の優遇措置が高電圧ヒューズの採用を促し、自動車回路保護の技術進歩を促進しています。この地域の自動車メーカーは車両エレクトロニクスの強化に注力しており、効率的な配電とシステムの安全性を確保するインテリジェントな高速応答ヒューズの需要を促進しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- サービス・プロバイダー

- 販売業者

- 最終用途

- 利益率分析

- コスト内訳分析

- テクノロジーとイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 電気自動車とハイブリッド車の普及

- 高度な車両安全機能に対する需要の高まり

- カーエレクトロニクスとコネクティビティ・ソリューションの成長

- 自動車の安全性と排出ガスに関する厳しい規制

- 業界の潜在的リスク&課題

- 最新の車両アーキテクチャとの統合課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ヒューズ別、2021年~2034年

- 主要動向

- ブレード

- ガラス

- スローブロー

- EVヒューズ

- その他

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- 商用車

第7章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- オール電化

- ハイブリッド

- FCEV

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AEM Components

- Blue Sea Systems

- Conquer

- Dongguan Better Electronics Technology

- Eaton

- ETA Elektrotechnische Apparate

- Fuzetec Technology

- GLOSO TECH

- Halfords

- Littelfuse

- Mersen

- MTA

- ON Semiconductor

- OptiFuse

- Pacific Engineering Corporation(PEC)

- Protectron Electromech

- Rainbow Power

- SCHURTER

- Siba

- Ultra Wiring Connectivity System

The Global Automotive Fuse Market, valued at USD 2 billion in 2024, is projected to grow at a CAGR of 4.5% from 2025 to 2034. As the automotive industry accelerates its shift toward electric vehicle production, demand for high-performance fuses rises. With vehicle production increasing by 10.3% year-over-year, automakers seek advanced circuit protection solutions to support the growing integration of electrical components. Regulatory bodies mandate robust electrical safety systems, making fuses essential for preventing short circuits, overheating, and electrical failures.

Rapid advancements in fuse technology enhance system protection, particularly in high-voltage electric vehicles. Manufacturers focus on developing durable fuses that withstand fast-charging environments and extreme conditions. Research and development efforts aim to enhance fuse efficiency, ensuring compliance with evolving safety regulations. The market experiences significant growth as automakers adopt innovative fuses that safeguard vehicle electronics, support power management, and improve overall reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 4.5% |

The increasing incorporation of advanced driver assistance systems, digital dashboards, and electric power steering drives the need for faster-response fuses. Investment in high-performance fuse solutions ensures compliance with emerging safety standards while protecting vehicle electrical components. The shift from conventional to smart fuses introduces remote diagnostic capabilities, improving safety by monitoring electrical loads and preventing failures. These intelligent fuses benefit electric and connected vehicles, which rely on efficient power management for optimal performance.

Automakers collaborate with fuse manufacturers to integrate smart fuse technologies into modern vehicle architectures. Digitalization fosters new opportunities, optimizing automotive circuit protection. The transition to electric powertrains requires fuses capable of handling high voltage and current loads while enhancing thermal management and preventing electrical risks. These advancements drive rapid adoption of electric and hybrid vehicles, making high-performance fuses indispensable to their development.

Manufacturers invest in smart fuse technology to enhance vehicle reliability, providing real-time fault detection and predictive maintenance. Intelligent fuses instantly report electrical system issues, improving safety and minimizing downtime. Automakers integrate these fuses into modern vehicle electronics to streamline maintenance operations and ensure continuous monitoring, reinforcing safety and performance.

Automakers collaborate with suppliers to develop customized fuse systems that align with specific vehicle structures and operational requirements. Optimized electrical protection enhances vehicle performance, extends lifespan, and reduces maintenance costs. Tailored fuse designs support sophisticated power systems while ensuring adherence to strict safety regulations.

The market is segmented by fuel type into gasoline, diesel, all-electric, hybrid, and fuel-cell vehicles. The gasoline segment is expected to witness substantial growth throughout the forecast period. Despite the rise of electric vehicles, gasoline cars remain dominant, sustaining demand for conventional and high-performance fuses. These fuses protect key electrical components, including ignition, fuel injection, and lighting systems.

By fuse type, the market is categorized into blade, glass, slow-blow, EV fuses, and others. Blade fuses held the largest market share in 2024 due to their compatibility, cost-effectiveness, and ease of replacement. Their widespread adoption in both traditional and electric vehicles underscores their reliability in circuit protection. As EV adoption rises, blade fuses with enhanced voltage and current capacities are being developed to support battery management and power distribution systems.

The Asia Pacific region experiences strong market growth, driven by increasing vehicle production and rising consumer demand. Government incentives for electric mobility encourage high-voltage fuse adoption, promoting technological advancements in automotive circuit protection. Automakers in the region focus on enhancing vehicle electronics, fueling demand for intelligent, high-speed response fuses that ensure efficient power distribution and system safety.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Manufacturer

- 3.2.4 Service provider

- 3.2.5 Distributor

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing adoption of electric and hybrid vehicles

- 3.8.1.2 Rising demand for advanced vehicle safety features

- 3.8.1.3 Growth in automotive electronics and connectivity solutions

- 3.8.1.4 Stringent regulations for vehicle safety and emissions

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Integration challenges with modern vehicle architectures

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fuse, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Blade

- 5.3 Glass

- 5.4 Slow blow

- 5.5 EV fuse

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicle

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 All-electric

- 7.5 Hybrid

- 7.6 FCEV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AEM Components

- 10.2 Blue Sea Systems

- 10.3 Conquer

- 10.4 Dongguan Better Electronics Technology

- 10.5 Eaton

- 10.6 ETA Elektrotechnische Apparate

- 10.7 Fuzetec Technology

- 10.8 GLOSO TECH

- 10.9 Halfords

- 10.10 Littelfuse

- 10.11 Mersen

- 10.12 MTA

- 10.13 ON Semiconductor

- 10.14 OptiFuse

- 10.15 Pacific Engineering Corporation (PEC)

- 10.16 Protectron Electromech

- 10.17 Rainbow Power

- 10.18 SCHURTER

- 10.19 Siba

- 10.20 Ultra Wiring Connectivity System