|

市場調査レポート

商品コード

1644664

自動車用ヒューズ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Automotive Fuse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用ヒューズ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

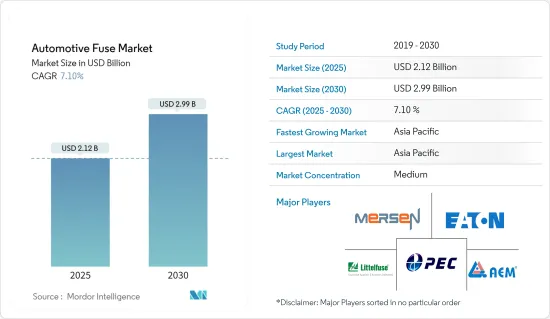

自動車用ヒューズ市場規模は2025年に21億2,000万米ドルと推計され、2030年には29億9,000万米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは7.1%です。

自動車用ヒューズは、自動車の配線や電気部品を保護します。通常、これらのヒューズはDC32ボルトに設定されているが、42ボルトで動作することもあります。1つまたは複数のヒューズボックスに収納され、通常はエンジンルームの片側またはダッシュボードの下、ステアリングホイールの近くに配置されています。これらのヒューズは短絡や過電流から保護し、潜在的に危険な電流レベルを検出すると回路を切断します。

主なハイライト

- 自動車用ヒューズは、過電流や短絡状態から電気回路を保護します。商用トラックから乗用車まで、あらゆる車種に不可欠な自動車用ヒューズ市場は、今後急速に拡大する見通しです。この成長の背景には、電気自動車の人気急上昇、高度な安全機能に対する需要の増加、自動車電気システムの複雑化といった要因があります。

- 自動車産業は、電動化と自律走行技術のイントロダクションよって大きな変貌を遂げました。この進化は、最新の自動車の安全性と信頼性を確保するための重要な部品である自動車用ヒューズの需要を促進しています。

- 自動車産業における技術の進歩、ドライバーレス車の台頭、モノのインターネット(IoT)技術の統合は、自動車用ヒューズの需要をさらに押し上げています。これらの進歩は、車両電子機器の信頼性と完全性を維持するための堅牢な回路保護方法を必要とします。特に電気自動車やハイブリッド車のニーズに対応するヒューズ技術の革新は、市場の成長を促進すると予想されます。

- 現代の自動車は複雑化し、電気的要求が高まっているにもかかわらず、低電圧ヒューズ技術の進歩は遅れています。現代の自動車には、ADAS(先進運転支援システム)、インフォテインメントシステム、電動パワートレインなど数多くの電子システムが組み込まれており、これらのシステムには堅牢で信頼性の高いヒューズが必要です。しかし、この技術的ギャップにより、今日の自動車電気システムの進化する要件に対応するヒューズの能力が制限されています。

- 自動車生産台数の伸びは、特に先進国での需要減退により、2024年には減速すると予測されています。高金利の継続は、家計所得が引き続き逼迫し、資金調達オプションがますます高価になっているため、自動車生産と販売の両方に圧力をかけています。さらに、既存の受注残が満たされるにつれて、2024年と2025年には自動車生産に対する需要の減少が予想されます。同部門は、インフレの持続や、自動車のサプライチェーンを混乱させる可能性のある部品不足など、大きな下振れリスクに直面しています。

自動車用ヒューズ市場の動向

電気自動車/ハイブリッド車が大きな成長を遂げる

- 一般に全電気自動車として知られるバッテリー電気自動車(BEV)は、従来の内燃エンジンの代わりに電気モーターを利用します。対照的に、ハイブリッド電気自動車は、内燃エンジンと1つ以上の電気モーターを組み合わせ、蓄電池からエネルギーを取り出します。BEVとは異なり、ハイブリッド電気自動車は充電のためにプラグを差し込むことができないです。バッテリーは回生ブレーキと内燃機関によって充電されます。この電気モーターの追加パワーは、より小さなエンジンを可能にし、バッテリーは補助負荷をサポートすることもでき、車両が据置型であるときのエンジンのアイドリングを最小限に抑えることができます。

- 電気自動車(EV)やハイブリッド電気自動車(HEV)のヒューズは、電気回路、機器、バッテリーを過負荷や短絡などの故障から保護します。EVは直流(DC)電圧を使用して電気回路を動作させます。

- 充電時間が短くなるにつれて、より高い電圧と電流をサポートするシステムの需要が高まっています。400Vから800Vへの移行は、バッテリー回路保護に大きな課題をもたらします。充電時間の短縮を推し進めるにはシステム電圧の上昇が必要ですが、走行距離の延長は故障電流を増加させます。多様なEVが計画されているため、より高い動作電流の需要が高まっています。このような力学は、回路保護のニーズを再構築しています。

- 中国では新車登録台数の3台に1台以上が電気自動車で、欧州では5台に1台を超え、米国では10台に1台に達しています。逆に、日本やインドのような先進的な自動車市場でも、電気自動車の販売は低迷しています。このような販売の集中が世界の電気自動車ストックを形成しており、自動車販売とストック全体の約3分の2を占める中国の動向の重要性を強調しています。

大きな成長を遂げるアジア太平洋地域

- 中国は、その強力な国内市場と計り知れない潜在力を背景に、自動車・モビリティ産業の世界的リーダーです。中国工業情報化部の予測によると、国内の自動車生産台数は2025年までに3,500万台に達する見込みで、世界有数の自動車メーカーとしての中国の地位が強化されます。この成長は、中国の自動車産業のさまざまな分野での急速な進歩を推進しています。

- 国際貿易局の報告によると、日本は世界第4位の自動車市場にランクされ、中国、米国、インドに次いでいます。日本はトヨタ、ホンダ、日産、マツダ、スズキといった大手自動車メーカーを抱える自動車製造の世界的大国です。自動車部門は日本のGDPの2.9%を占め、その経済的重要性を際立たせています。その結果、日本は自動車の安全性と公害防止に焦点を当てた厳格な法律を施行しています。

- 日本は、燃費、CO2、その他の排出ガスを測定する試験サイクルの国際基準を支持しています。特筆すべきは、国連の自動車規制調和世界フォーラムに基づく世界調和小型車テストサイクル(WLTC)の開発において、日本が極めて重要な役割を果たしたことです。このコミットメントを反映し、日本は、乗用車と非重量車のテストサイクルをJC08からWLTCに移行しています。

- 自動車産業は経済成長と雇用創出にとって極めて重要であり、インドのGDPに7.1%貢献しています。消費者需要の拡大、所得の増加、都市化、消費者行動の変化が自動車産業成長の主な原動力となっています。

- 2024年4月だけでも、乗用車、三輪車、二輪車、四輪車の生産台数は235万8,041台に達しました。さらに、23年度のインドからの自動車輸出総額は476万1,487台に達しました。この数年間で、自動車部門のGDPへの貢献は7.1%に大幅に増加しました。さらに、自動車部門は約1,900万人に直接・間接雇用を提供しています。

自動車用ヒューズ産業の概要

自動車用ヒューズ市場は、多数の現地メーカーが存在するため、半固体化しています。市場の主要企業には、Pacific Engineering Corporation、Littelfuse Inc.、Eaton Corporation、Mersen Electrical Power、AEM Components(USA)Inc.などが含まれます。

市場は、統合の進展、技術の進歩、地政学的シナリオによって変動しています。また、新興中小企業の増加に伴い、その収益に起因する投資能力を考慮すると、市場競争は今後も激化すると予想されます。

さらに、イノベーションによる持続可能な競争優位性がかなり高い市場では、さまざまなエンドユーザー産業にわたる新規顧客からの需要増加が予測されることから、競争は激化すると予想されます。このような状況では、エンドユーザーがヒューズ製造業者に期待する品質の重要性を考慮すると、ブランド・アイデンティティが大きな役割を果たします。また、Eaton Corporation、Little Fuse Inc.、Pacific Engineering Corporation、Mersen Electric Power、AEM Components USA Inc.など、市場の既存大手企業による市場浸透度も高いです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 自動車新時代の進化- 電動化と自動化

- 自動車への電気・電子ユニット搭載の増加

- 市場の課題/抑制要因

- 低電圧ヒューズ分野の限られた開発とヒューズ市場における未組織アフターマーケット

第6章 市場セグメンテーション

- タイプ別

- ブレード

- ガラス

- スローブロー

- 高電圧ヒューズ

- チップヒューズ

- その他のタイプ

- 車両タイプ別

- 乗用車(従来型-ICE)

- 商用車(従来型-ICE)

- 電気自動車/ハイブリッド車

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- フランス

- ドイツ

- スペイン

- アジア

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Pacific Engineering Corporation

- Littelfuse Inc.

- Eaton Corporation

- Mersen Electrical Power

- AEM Components(USA)Inc.

- On Semiconductor Corporation

- OptiFuse

- Bel Fuse Inc.

第8章 投資分析

第9章 市場の将来

The Automotive Fuse Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 2.99 billion by 2030, at a CAGR of 7.1% during the forecast period (2025-2030).

Automotive fuses safeguard a vehicle's wiring and electrical components. Typically set at 32 volts DC, these fuses can operate at 42 volts. Housed in one or more fuse boxes, they are usually located on one side of the engine compartment or under the dashboard near the steering wheel. These fuses protect against short circuits and over-currents, disconnecting the circuit upon detecting potentially dangerous current levels.

Key Highlights

- Automotive fuses protect electrical circuits from overcurrent and short-circuit situations. Essential for all vehicle types, from commercial trucks to passenger cars, the automotive fuse market is poised for rapid expansion in the coming years. This growth is driven by several factors: the surging popularity of electric vehicles, an increasing demand for advanced safety features, and the escalating complexity of automotive electrical systems.

- The automotive industry underwent a significant transformation with the introduction of electrification and autonomous driving technologies. This evolution is driving the demand for automotive fuses, which are critical components for ensuring the safety and reliability of modern vehicles.

- Technological advancements in the automotive industry, the rise of driverless cars, and the integration of Internet of Things (IoT) technologies further drive the demand for automotive fuses. These advancements require robust circuit protection methods to maintain the dependability and integrity of vehicle electronics. Innovations in fuse technology, particularly those catering to the needs of electric and hybrid vehicles, are expected to propel the growth of the market.

- Despite modern vehicles' growing complexity and electrical demands, advancements in low-voltage fuse technology have lagged. Modern vehicles incorporate numerous electronic systems, such as advanced driver-assistance systems (ADAS), infotainment systems, and electric powertrains, which require robust and reliable fuses. However, this technological gap limits the fuses' ability to cater to the evolving requirements of today's automotive electrical systems.

- The anticipated growth in automotive production is projected to decelerate in 2024 due to a decline in demand, especially within advanced economies. The ongoing high interest rates are exerting pressure on both automotive production and sales as household incomes continue to be strained and financing options have become increasingly expensive. Furthermore, as existing order backlogs are fulfilled, a reduction in demand for automotive production is expected in 2024 and 2025. The sector faces significant downside risks, including persistent inflation and potential component shortages that may disrupt automotive supply chains.

Automotive Fuse Market Trends

Electric/Hybrid Vehicles to Witness Major Growth

- Battery electric vehicles (BEVs), commonly known as all-electric vehicles, utilize an electric motor instead of a traditional internal combustion engine. In contrast, hybrid electric vehicles combine an internal combustion engine with one or more electric motors, drawing energy from stored batteries. Unlike BEVs, hybrid electric vehicles cannot be plugged in for charging; their batteries recharge through regenerative braking and the internal combustion engine. This electric motor's added power can enable a smaller engine, and the battery can also support auxiliary loads, minimizing engine idling when the vehicle is stationary.

- Fuses in Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) safeguard electrical circuits, equipment, and batteries from faults like overloads and short circuits. EVs operate their electrical circuits using direct current (DC) voltage.

- As charging times decrease, a growing demand for systems supporting higher voltage and current is growing. Transitioning from 400V to 800V introduces significant challenges for battery circuit protection. While the push for quicker charging times necessitates elevated system voltages, an extended driving range increases fault currents. The diverse range of planned EVs amplifies the demand for higher operating currents. These dynamics are reshaping circuit protection needs.

- Electric cars are making significant inroads in global markets: in China, over one in three new car registrations were electric; in Europe, the figure surpassed one in five; and in the United States, it reached one in ten. Conversely, electric car sales remain subdued even in advanced automotive markets like Japan and India. This concentration in sales shapes the global electric car stock and underscores the significance of trends in China, which accounts for about two-thirds of total car sales and stocks.

Asia Pacific to Register Major Growth

- China is a global leader in the automotive and mobility industry, driven by its strong domestic market and immense potential. The Chinese Ministry of Industry and Information Technology predicts domestic vehicle production is expected to reach 35 million by 2025, reinforcing China's position as the world's leading car manufacturer. This growth propels rapid advancements across various sectors of China's automobile industry.

- As reported by the International Trade Administration, Japan ranks as the world's fourth-largest automotive market, trailing only China, the United States, and India. Japan is a global powerhouse in automotive manufacturing, hosting major automakers like Toyota, Honda, Nissan, Mazda, and Suzuki. The automotive sector constitutes 2.9% of Japan's GDP, underscoring its economic significance. Consequently, Japan enforces stringent laws focused on vehicle safety and pollution control.

- Japan is championing international standards for testing cycles that gauge fuel consumption, CO2, and other emissions. Notably, Japan played a pivotal role in developing the World Harmonized Light Vehicle Test Cycle (WLTC) under the UN's World Forum for Harmonization of Vehicle Regulations. Reflecting this commitment, Japan is transitioning from its JC08 test cycle to the WLTC for passenger and non-heavy-duty vehicles.

- The automotive industry is crucial to economic growth and job creation, contributing 7.1% to India's GDP. The growing consumer demand, rising income, urbanization, and changing consumer behavior are the major driving forces for the automotive industry's growth.

- In April 2024 alone, production figures for passenger vehicles, three-wheelers, two-wheelers, and quadricycles reached 2,358,041 units. Additionally, in FY23, total automobile exports from India amounted to 4,761,487 vehicles. Over the years, the sector's contribution to the national GDP has significantly increased to 7.1%. Moreover, the automotive sector provides direct and indirect employment to approximately 19 million individuals.

Automotive Fuse Industry Overview

The automotive fuse market is semiconsolidated due to the large number of local manufacturers available in the automotive fuse market landscape. The significant players in the market include Pacific Engineering Corporation, Littelfuse Inc., Eaton Corporation, Mersen Electrical Power, and AEM Components (USA) Inc.

The market studied is fluctuating due to growing consolidation, technological advancement, and geopolitical scenarios. In addition, with the increasing number of new SMEs, the intense competition in the market studied is expected to continue to rise, considering their ability to invest, which results from their revenues.

Further, in a market where the sustainable competitive advantage through innovation is considerably high, competition is anticipated to grow, considering the projected increase in demand from new customers across various end-user industries. In such a situation, the brand identity plays a major role, considering the importance of quality that the end-users expect from a fuse manufacturing player. The market penetration levels are also high with large market incumbents, such as Eaton Corporation, Little Fuse Inc., Pacific Engineering Corporation, Mersen Electric Power, and AEM Components USA Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Evolution of New Automotive Era -Electrification and Autonomy

- 5.1.2 Increasing Incorporation of Electrical and Electronic Units in Automobiles

- 5.2 Market Challenges/Restraints

- 5.2.1 Limited Development in the Field of Low-Voltage Fuses and Unorganized Aftermarket in the Fuse Market

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Blade

- 6.1.2 Glass

- 6.1.3 Slow Blow

- 6.1.4 High-Voltage Fuses

- 6.1.5 Chip Fuse

- 6.1.6 Other Types

- 6.2 By Type of Vehicle

- 6.2.1 Passenger Cars (Traditional -ICE)

- 6.2.2 Commercial Vehicles (Traditional -ICE)

- 6.2.3 Electric/Hybrid Vehicles

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 France

- 6.3.2.2 Germany

- 6.3.2.3 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Pacific Engineering Corporation

- 7.1.2 Littelfuse Inc.

- 7.1.3 Eaton Corporation

- 7.1.4 Mersen Electrical Power

- 7.1.5 AEM Components (USA) Inc.

- 7.1.6 On Semiconductor Corporation

- 7.1.7 OptiFuse

- 7.1.8 Bel Fuse Inc.