|

市場調査レポート

商品コード

1698267

自動車用トラクションモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用トラクションモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月17日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

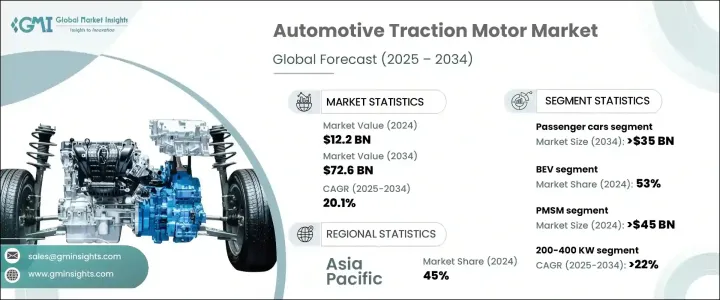

自動車用トラクションモーターの世界市場は、2024年には122億米ドルとなり、2025年から2034年にかけてCAGR 20.1%で成長すると予測されています。

電気自動車(EV)の生産台数が世界的に大幅に増加していることが、この成長の主な要因となっています。各国政府は、ディーゼル車への依存を減らし、自動車の電動化を推進することで、二酸化炭素排出量の削減を推進しています。消費者の持続可能性と燃料節約への意識も高まっており、EVへの移行がさらに加速しています。

パワーエレクトロニクスとモーター制御の技術的進歩により、トラクションモーターの効率と性能が向上しています。炭化ケイ素(SiC)や窒化ガリウム(GaN)半導体の採用は、電力効率を高め、エネルギー損失を最小限に抑え、モーター出力を最適化します。この進歩により、メーカーはより小型で軽量なモーターを開発できるようになり、車両性能の向上につながります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 122億米ドル |

| 予測金額 | 726億米ドル |

| CAGR | 20.1% |

自動車用トラクションモーター市場は、モータータイプ別に永久磁石同期モーター(PMSM)とAC誘導モーターに分類されます。2024年にはPMSMが市場を独占し、450億米ドル以上の収益を生み出します。これらのモーターは、軽量構造、優れたトルク、高効率のため好まれ、EV牽引システムによく使用されています。PMSMは誘導モーターに比べて消費電力が大きいため、メーカーは最新のEV設計に組み込むことを優先しています。

レアアース(希土類)材料をめぐるコストと供給の懸念の高まりにより、メーカーは、ネオジムやジスプロシウムなしで効率的に機能するレアアース・フリーのPMSMを開発するようになりました。こうした技術革新によりサプライチェーンが安定し、EVへのPMSMの採用が広がっています。これらの設計が改善され続ければ、より多くのメーカーが導入し、市場拡大をさらに促進すると予想されます。

また、市場は出力別に200kW未満、200~400kW、400kW以上の3つに区分されます。200~400 kWのセグメントは、2034年までにCAGR 22%以上の成長が見込まれています。このレンジの高出力トラクションモーターは、電動SUV、スポーツカー、商用車で人気が高まっています。自動車メーカーは、これらのモーターを統合して加速と性能を高め、強力かつ効率的な電動ドライブトレインに対する需要の高まりに対応しています。

トラックやバスを含む電気商用車も、高出力トラクションモーターの需要に拍車をかけています。物流と貨物輸送は電動化に移行しつつあり、高トルクと高出力のモーターへのニーズが高まっています。現在、多くのEVがデュアルモーターによる全輪駆動(AWD)システムを搭載しており、安定性とトラクションを向上させる一方で、200~400kWの範囲の定格出力が必要とされています。自動車メーカーは、車両ダイナミクスを最適化するためにこの設計を採用しており、高出力トラクションモーターの需要をさらに押し上げています。

中国、日本、韓国、インドなどの国々がEVインフラと製造に多額の投資を行っており、アジア太平洋地域は依然としてEV生産において支配的な力を持っています。大手EVメーカーの存在と、この地域のサプライチェーン、特にレアアース磁石生産の進歩が、市場の成長を支えています。世界最大のEV市場である中国は、国内需要と世界需要の両方に対応するため、生産能力の拡大を続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料・部品サプライヤー

- 自動車メーカー

- 自動車メーカー

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 価格動向

- ケーススタディ

- 影響要因

- 促進要因

- 電気自動車を促進する政府のインセンティブと排出削減政策の増加

- 環境に優しくエネルギー効率の高い電気自動車に対する消費者の需要の高まり

- モーター効率の向上によるエネルギー消費の削減と航続距離の延長

- AIと自律走行技術の採用が増加し、トラクションモーター・システムの技術革新を促進

- 業界の潜在的リスク&課題

- モーターに必要な希土類元素などの重要材料のサプライチェーンにおける制約

- 高度なトラクションモーター技術に関連する高い開発コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 二輪車

- オフロード車

第6章 市場推計・予測:電動ドライブトレイン別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- ハイブリッド電気自動車(HEV)

- プラグインハイブリッド車(PHEV)

第7章 市場推計・予測:モーター別、2021年~2034年

- 主要動向

- PMSM

- ACインダクション

第8章 市場推計・予測:出力別、2021年~2034年

- 主要動向

- 200KW未満

- 200-400 KW

- 400KW以上

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Audi

- Bosch

- Continental

- Ford

- General

- Honda

- Hyundai

- Kia

- Magna

- Magneti Marelli

- Mercedes Benz

- Mitsubishi

- Nidec

- Parker Hannifin

- PSA Group

- SAIC Motor

- Schaeffler

- Valeo

- Volkswagen

- ZF Friedrichshafen

The Global Automotive Traction Motor Market was valued at USD 12.2 billion in 2024 and is projected to grow at a CAGR of 20.1% from 2025 to 2034. A significant rise in electric vehicle (EV) production worldwide is a key driver of this growth. Governments are pushing for lower carbon emissions by reducing reliance on diesel fleets and promoting vehicle electrification. Consumers are also becoming more conscious of sustainability and fuel conservation, further accelerating the transition to EVs.

Technological advancements in power electronics and motor control are improving the efficiency and performance of traction motors. The adoption of silicon carbide (SiC) and gallium nitride (GaN) semiconductors enhances power efficiency, minimizes energy loss, and optimizes motor output. This progress allows manufacturers to develop more compact and lightweight motors, leading to better vehicle performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.2 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 20.1% |

The automotive traction motor market is categorized by motor type into Permanent Magnet Synchronous Motors (PMSM) and AC induction motors. PMSM dominated the market in 2024, generating over USD 45 billion in revenue. These motors are preferred due to their lightweight structure, superior torque, and higher efficiency, making them a popular choice for EV traction systems. As PMSMs consume more electric energy compared to induction motors, manufacturers are prioritizing their integration into modern EV designs.

Rising costs and supply concerns surrounding rare earth materials have prompted manufacturers to develop rare-earth-free PMSMs that function efficiently without neodymium or dysprosium. These innovations are stabilizing the supply chain and facilitating broader adoption of PMSMs in EVs. As these designs continue to improve, more manufacturers are expected to implement them, further driving market expansion.

The market is also segmented by power output into three categories: less than 200 kW, 200-400 kW, and above 400 kW. The 200-400 kW segment is anticipated to grow at a CAGR of over 22% by 2034. High-output traction motors in this range are becoming increasingly popular in electric SUVs, sports cars, and commercial vehicles. Automakers are integrating these motors to enhance acceleration and performance, meeting the growing demand for powerful yet efficient electric drivetrains.

Electric commercial vehicles, including trucks and buses, are also fueling the demand for high-power traction motors. Logistics and freight transport are transitioning toward electrification, increasing the need for motors with high torque and power capacity. Many EVs are now equipped with dual-motor all-wheel-drive (AWD) systems, improving stability and traction while requiring power ratings within the 200-400 kW range. Automakers are adopting this design to optimize vehicle dynamics, further driving the demand for high-power traction motors.

Asia Pacific remains a dominant force in EV production, with countries such as China, Japan, South Korea, and India investing heavily in EV infrastructure and manufacturing. The presence of leading EV manufacturers and advancements in the regional supply chain, particularly in rare earth magnet production, are supporting market growth. China, as the world's largest EV market, continues to expand production capacity to cater to both domestic and global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material & component suppliers

- 3.1.2 Manufacturers

- 3.1.3 Automotive manufacturers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trend

- 3.9 Case studies

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing government incentives and emission reduction policies promoting electric vehicles

- 3.10.1.2 Rising consumer demand for eco-friendly and energy-efficient electric vehicles

- 3.10.1.3 Advancements in motor efficiency, reducing energy consumption and extending vehicle range

- 3.10.1.4 Growing adoption of AI and autonomous technologies, driving innovation in traction motor systems

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Supply chain constraints for critical materials such as rare earth elements needed for motors

- 3.10.2.2 High development costs associated with advanced traction motor technologies

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Heavy Commercial Vehicles (HCV)

- 5.4 Two-wheelers

- 5.5 Off-road vehicles

Chapter 6 Market Estimates & Forecast, By Electric Drivetrain, 2021 - 2034($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicle (BEV)

- 6.3 Hybrid Electric Vehicle (HEV)

- 6.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 7 Market Estimates & Forecast, By Motor, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 PMSM

- 7.3 AC Induction

Chapter 8 Market Estimates & Forecast, By Power Output, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 200 KW

- 8.3 200-400 KW

- 8.4 Above 400 KW

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Audi

- 10.2 Bosch

- 10.3 Continental

- 10.4 Ford

- 10.5 General

- 10.6 Honda

- 10.7 Hyundai

- 10.8 Kia

- 10.9 Magna

- 10.10 Magneti Marelli

- 10.11 Mercedes Benz

- 10.12 Mitsubishi

- 10.13 Nidec

- 10.14 Parker Hannifin

- 10.15 PSA Group

- 10.16 SAIC Motor

- 10.17 Schaeffler

- 10.18 Valeo

- 10.19 Volkswagen

- 10.20 ZF Friedrichshafen