|

市場調査レポート

商品コード

1685090

医療機器検査サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Medical Devices Testing Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 医療機器検査サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月10日

発行: Global Market Insights Inc.

ページ情報: 英文 148 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

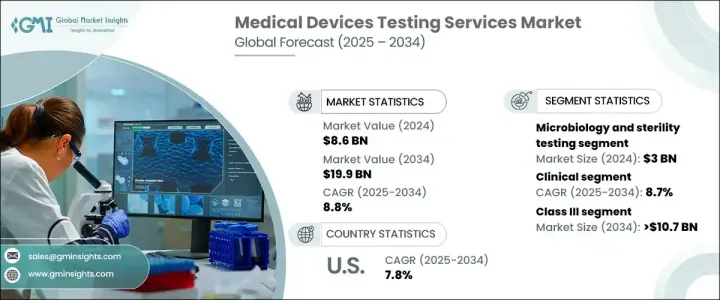

医療機器検査サービスの世界市場は、2024年に86億米ドルと評価され、2025年から2034年にかけて8.8%のCAGRで堅調に成長すると予測されています。

この成長は、医療機器の安全性、性能、有効性を保証する厳格な規制要件を満たす必要性が高まっていることが主な要因です。ヘルスケア技術の絶え間ない革新に伴い、包括的で厳格な試験サービスに対する需要はこれまで以上に不可欠となっています。医療機器メーカーは、国際的な規制基準に準拠し、費用のかかる製品リコールや安全性の問題を回避するために、試験を優先しています。ウェアラブル、埋め込み型技術、診断ツールなどの医療機器の複雑さが増すにつれ、高度な試験方法の必要性も高まっています。臨床試験や前臨床試験、微生物検査を通じて安全性と有効性を確保する必要性は、今後も市場の将来を形成していくと思われます。

さまざまな検査サービスの中でも、微生物検査と無菌検査が2024年の市場を独占し、30億米ドルを生み出しました。このサービスは、微生物汚染の検出や滅菌技術の検証に不可欠であり、機器が安全基準を満たすことを保証するために極めて重要です。ヘルスケア施設における感染管理の重視の高まりが、こうしたサービスの需要をさらに押し上げています。ヘルスケア関連感染が依然として最大の関心事であることを考えると、無菌検査のニーズは今後も上昇基調を続けると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 86億米ドル |

| 予測金額 | 199億米ドル |

| CAGR | 8.8% |

医療機器検査サービス市場は、臨床試験と前臨床試験にも区分されます。CAGR8.7%の成長が見込まれる臨床試験分野は、2034年までに131億米ドルに達すると予測されています。臨床試験は、医療機器の安全性と有効性を実際の条件下で検証し、規制と市場の期待の両方を満たすようにするために不可欠です。医療技術の進歩に伴い、臨床試験は、ウェアラブルやインプラントのような機器の使いやすさ、生体適合性、全体的な安全性を評価する上でさらに重要になっています。これらの機器の複雑さが増すにつれて、特に人体にシームレスに統合される新しい技術革新では、臨床評価により詳細なアプローチが要求されます。

米国の医療機器検査サービス市場は2024年に22億米ドルを獲得し、2025年から2034年にかけてCAGR 7.8%で成長すると予想されています。北米は、先進的なヘルスケアインフラと強力な規制の枠組みを背景に、世界市場で優位を保っています。この地域は、FDAなどの規制機関のネットワークが確立されており、医療機器の最高の安全性と品質基準を確保するために包括的な試験プロトコルを実施しています。この厳格な規制状況と、研究開発および試験サービスへの多大な投資が相まって、北米は医療機器試験の中心地となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 厳格な承認基準への注目の高まり

- 医療技術の一貫した急速な進歩

- 医療機器の検証と妥当性確認に対するニーズの高まり

- 業界の潜在的リスク&課題

- 熟練した専門家と試験施設の不足

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:サービス別、2021年~2034年

- 主要動向

- 微生物検査と無菌検査

- 抗菌試験

- パイロジェンおよびエンドトキシン試験

- 無菌試験とバリデーション

- バイオバーデン測定

- その他の微生物学および無菌試験

- 生体適合性試験

- 化学試験

- パッケージバリデーション

第6章 市場推計・予測:フェーズ別、2021年~2034年

- 主要動向

- 臨床試験

- 前臨床

第7章 市場推計・予測:デバイスクラス別、2021年~2034年

- 主要動向

- クラスIII

- クラスII

- クラスI

第8章 市場推計・予測:モード別、2021年~2034年

- 主要動向

- アウトソーシング

- インハウス

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 医療機器メーカー

- 臨床研究機関(CRO)

- 学術・研究機関

- その他のエンドユーザー

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- charles river

- element

- eurofins

- intertek

- labcorp

- NAMSA

- Pace

- SGS

- Sterigenics

- TUV SUD

- WuXiAppTec

The Global Medical Devices Testing Services Market, valued at USD 8.6 billion in 2024, is projected to grow at a robust CAGR of 8.8% from 2025 to 2034. This growth is largely driven by an increasing need to meet stringent regulatory requirements that ensure medical devices' safety, performance, and efficacy. With continuous innovations in healthcare technology, the demand for comprehensive and rigorous testing services is more essential than ever. Medical device manufacturers are prioritizing testing to comply with international regulatory standards and avoid costly product recalls or safety issues. As the complexity of medical devices such as wearables, implantable technologies, and diagnostic tools rises, so does the need for advanced testing methods. The need to ensure safety and effectiveness through clinical and preclinical trials, as well as microbiological testing, will continue to shape the future of the market.

Among the various testing services, microbiology and sterility testing dominated the market in 2024, generating USD 3 billion. This service is critical in detecting microbial contamination and validating sterilization techniques, which is crucial for ensuring that devices meet safety standards. The growing emphasis on infection control in healthcare facilities further drives the demand for these services. Given that healthcare-associated infections remain a top concern, the need for sterility testing is expected to continue its upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.6 Billion |

| Forecast Value | $19.9 Billion |

| CAGR | 8.8% |

The medical devices testing services market is also segmented into clinical and preclinical testing. The clinical testing segment, which is expected to grow at a CAGR of 8.7%, is projected to reach USD 13.1 billion by 2034. Clinical trials are essential for validating the safety and efficacy of medical devices under real-world conditions, ensuring they meet both regulatory and market expectations. As medical technology advances, clinical testing is becoming even more critical in assessing the usability, biocompatibility, and overall safety of devices like wearables and implants. The increasing complexity of these devices requires a more detailed approach to clinical evaluations, especially with newer innovations that integrate seamlessly into the human body.

The U.S. medical devices testing services market garnered USD 2.2 billion in 2024 and is expected to grow at a CAGR of 7.8% from 2025 to 2034. North America, driven by its advanced healthcare infrastructure and strong regulatory framework, remains a dominant player in the global market. The region benefits from a well-established network of regulatory bodies, such as the FDA, that enforce comprehensive testing protocols to ensure the highest safety and quality standards for medical devices. This rigorous regulatory landscape, combined with considerable investments in R&D and testing services, makes North America a hub for medical devices testing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing focus on strict approval norms

- 3.2.1.2 Consistent and rapid advancements in medical technologies

- 3.2.1.3 Rising need for verification and validation of medical devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals and testing facilities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Services, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Microbiology and sterility testing

- 5.2.1 Antimicrobial testing

- 5.2.2 Pyrogen and endotoxin testing

- 5.2.3 Sterility test and validation

- 5.2.4 Bioburden determination

- 5.2.5 Other microbiology and sterility testings

- 5.3 Biocompatibility tests

- 5.4 Chemistry test

- 5.5 Package validation

Chapter 6 Market Estimates and Forecast, By Phase, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical

- 6.3 Preclinical

Chapter 7 Market Estimates and Forecast, By Device Class, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Class III

- 7.3 Class II

- 7.4 Class I

Chapter 8 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Outsourced

- 8.3 In-house

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Medical device manufacturers

- 9.3 Clinical research organizations (CROs)

- 9.4 Academic and research institutions

- 9.5 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 charles river

- 11.2 element

- 11.3 eurofins

- 11.4 intertek

- 11.5 labcorp

- 11.6 NAMSA

- 11.7 Pace

- 11.8 SGS

- 11.9 Sterigenics

- 11.10 TUV SUD

- 11.11 WuXiAppTec