|

市場調査レポート

商品コード

1684843

廃熱回収システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Waste Heat Recovery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 廃熱回収システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月28日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

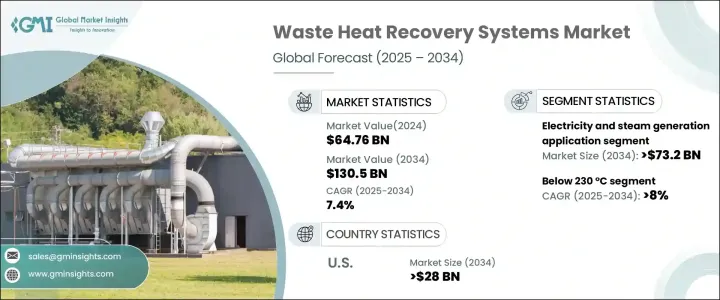

世界の廃熱回収システム市場は、2024年に647億6,000万米ドルに達し、持続可能性への取り組みの高まり、厳しい環境規制、エネルギー効率の進歩に牽引され、2025年から2034年にかけてCAGR 7.5%で拡大すると予測されています。

さまざまな業界の企業が、資源利用の最適化、エネルギー効率の向上、進化する規制要件への対応を目的に、廃熱回収ソリューションの採用を増やしています。これらのシステムは、産業プロセスから余分な熱を回収し、使用可能なエネルギーに変換することで、二酸化炭素排出量を削減し、運用コストを削減します。セメント、ガラス、化学、石油精製などの業界が費用対効果の高いソリューションを求める中、廃熱回収技術は現代の産業運営に欠かせないものとなりつつあります。よりクリーンなエネルギーソリューションと持続可能性の向上を目指す動きは、こうした先端技術の採用を強化し続けており、世界のエネルギー転換の重要な要素となっています。

世界中の産業界がカーボンフットプリントの削減と長期的なエネルギー効率の達成に注力する中、廃熱回収システムは勢いを増しています。企業は、これらの技術が環境保全に貢献するだけでなく、エネルギー消費を削減することで大幅なコスト削減を実現することを認識しつつあります。循環型経済への取り組みが重視されるようになり、エネルギー効率の高い製造プロセスが推進されていることが、市場の拡大を加速しています。さらに、熱交換器、熱電発電機、有機ランキンサイクルの技術進歩がシステム効率を高め、幅広い産業にとって魅力的なものとなっています。政府のインセンティブやクリーンエネルギーを促進する有利な政策は、廃熱回収ソリューションの採用をさらに後押ししています。企業が持続可能性を優先し続ける中、これらのシステムに対する需要は急増し、産業用エネルギー管理の将来を再構築すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 647億6,000万米ドル |

| 予測金額 | 1,305億米ドル |

| CAGR | 7.5% |

2034年までに、電気・蒸気発電部門は732億米ドルを生み出すと予測されています。地球環境問題や温室効果ガス排出量の増加に対する懸念が高まり、産業界はエネルギー効率の高いソリューションを事業運営に組み込む必要に迫られています。廃熱回収技術は、余熱を回収して発電に再利用することで、こうした懸念に効果的に対処し、事業の持続可能性を大幅に改善します。世界の産業界が脱炭素化への取り組みを強化する中、廃熱回収システムはエネルギー効率を高め、排出量を削減するための不可欠なツールとなっています。企業は、廃熱回収の導入によるコスト削減から法規制遵守の改善まで、長期的なメリットをますます認識するようになっており、市場の持続的な成長を後押ししています。

230 °C以下で作動する廃熱回収システム市場は、2034年までCAGR 8%で成長すると予想されます。パルプ・製紙、食品加工、化学など、温度範囲が緩やかな産業での採用が増加していることが、拡大に拍車をかけています。工業プロセスからの廃熱は、エネルギー回収の大きな機会となるため、これらの分野は回収技術を採用する主要な企業となっています。これらのシステムに投資する企業は、長期的なコスト削減、エネルギー消費量の削減、炭素排出量の最小化から恩恵を受け、持続可能性への取り組みを強化しています。資源の最適化とエネルギー効率に優れた製造業への注目の高まりは、こうした先進的システムへの需要をさらに高めています。

米国の廃熱回収システム市場は、高いエネルギーコスト、厳しい環境規制、持続可能な産業慣行へのシフトの高まりを背景に、2034年までに280億米ドルを創出する見通しです。さまざまな分野の企業が、エネルギー効率を高め、脱炭素化への取り組みを支援するため、最先端の廃熱回収ソリューションに多額の投資を行っています。回収熱を発電に利用し、従来のエネルギー源への依存を減らすことに焦点を当てた取り組みにより、産業界と技術プロバイダーとの協力体制は市場をさらに強化しています。産業界が持続可能性とコスト効率を優先し続ける中、廃熱回収技術への需要は加速し、エネルギー管理と産業運営の未来を形作ることになると思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- プレヒーティング

- 電気・蒸気発電

- 蒸気ランキンサイクル

- 有機ランキンサイクル

- カリーナサイクル

- その他

第6章 市場規模・予測:温度別、2021年~2034年

- 主要動向

- 230°C未満

- 230 °C-650 °C

- 650 °C超

第7章 市場規模・予測:最終用途別、2021~2034年

- 主要動向

- 石油精製

- セメント

- 重金属製造

- 化学

- パルプ・製紙

- 飲食品

- ガラス

- その他製造業

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- Aura

- BIHL

- Bosch Industriekessel

- Climeon

- Cochran

- Durr Group

- Echogen

- Exergy International

- Forbes Marshall

- General Electric

- IHI Power Systems

- John Wood Group

- Mitsubishi Heavy Industries

- Ormat

- Promec Engineering

- Rentech Boilers

- Siemens Energy

- Sofinter

- Thermax

- Viessmann

The Global Waste Heat Recovery Systems Market reached USD 64.76 billion in 2024 and is projected to expand at a 7.5% CAGR from 2025 to 2034, driven by rising sustainability initiatives, stringent environmental regulations, and advancements in energy efficiency. Companies across multiple industries are increasingly adopting waste heat recovery solutions to optimize resource utilization, enhance energy efficiency, and meet evolving regulatory requirements. These systems capture excess heat from industrial processes and convert it into usable energy, reducing carbon emissions and lowering operational costs. With industries such as cement, glass, chemicals, and petroleum refining seeking cost-effective solutions, waste heat recovery technologies are becoming indispensable in modern industrial operations. The push toward cleaner energy solutions and improved sustainability practices continues to reinforce the adoption of these advanced technologies, making them a critical component of the global energy transition.

As industries worldwide focus on reducing carbon footprints and achieving long-term energy efficiency, waste heat recovery systems are gaining momentum. Companies are realizing that these technologies not only contribute to environmental conservation but also provide significant cost savings by reducing energy consumption. The growing emphasis on circular economy practices and the push for energy-efficient manufacturing processes are accelerating market expansion. Furthermore, technological advancements in heat exchangers, thermoelectric generators, and organic Rankine cycles are enhancing system efficiency, making them more attractive to a wide range of industries. Government incentives and favorable policies promoting clean energy further support the adoption of waste heat recovery solutions. As businesses continue prioritizing sustainability, demand for these systems is expected to surge, reshaping the future of industrial energy management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $64.76 Billion |

| Forecast Value | $130.5 Billion |

| CAGR | 7.5% |

By 2034, the electricity and steam generation segment is projected to generate USD 73.2 billion. Rising concerns over global environmental issues and increasing greenhouse gas emissions are pushing industries to integrate energy-efficient solutions into their operations. Waste heat recovery technologies effectively address these concerns by capturing residual heat and repurposing it for power generation, significantly improving operational sustainability. With global industries intensifying their decarbonization efforts, these systems have become essential tools for enhancing energy efficiency and reducing emissions. Businesses are increasingly recognizing the long-term benefits of implementing waste heat recovery, from cost reductions to improved regulatory compliance, driving sustained market growth.

The market for waste heat recovery systems operating at temperatures below 230 °C is expected to grow at a CAGR of 8% through 2034. The expansion is fueled by rising adoption in industries with moderate temperature ranges, including pulp and paper, food processing, and chemicals. Waste heat from industrial processes presents a substantial opportunity for energy recovery, making these sectors key adopters of recovery technologies. Companies investing in these systems benefit from long-term cost savings, reduced energy consumption, and minimized carbon emissions, reinforcing their commitment to sustainability. The increasing focus on resource optimization and energy-efficient manufacturing further amplifies the demand for these advanced systems.

The U.S. waste heat recovery systems market is poised to generate USD 28 billion by 2034, driven by high energy costs, stringent environmental regulations, and the growing shift toward sustainable industrial practices. Companies across various sectors are heavily investing in cutting-edge waste heat recovery solutions to enhance energy efficiency and support decarbonization initiatives. The collaboration between industries and technology providers is further strengthening the market, with efforts focused on utilizing recovered heat for power generation and reducing dependence on traditional energy sources. As industrial sectors continue prioritizing sustainability and cost-efficiency, the demand for waste heat recovery technologies is set to accelerate, shaping the future of energy management and industrial operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Pre-Heating

- 5.3 Electricity & steam generation

- 5.3.1 Steam rankine cycle

- 5.3.2 Organic rankine cycle

- 5.3.3 Kalina cycle

- 5.4 Other

Chapter 6 Market Size and Forecast, By Temperature, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 <230°C

- 6.3 230°C - 650 °C

- 6.4 >650 °C

Chapter 7 Market Size and Forecast, By End Use, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Petroleum refining

- 7.3 Cement

- 7.4 Heavy metal manufacturing

- 7.5 Chemical

- 7.6 Pulp & paper

- 7.7 Food & beverage

- 7.8 Glass

- 7.9 Other manufacturing

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Aura

- 9.2 BIHL

- 9.3 Bosch Industriekessel

- 9.4 Climeon

- 9.5 Cochran

- 9.6 Durr Group

- 9.7 Echogen

- 9.8 Exergy International

- 9.9 Forbes Marshall

- 9.10 General Electric

- 9.11 IHI Power Systems

- 9.12 John Wood Group

- 9.13 Mitsubishi Heavy Industries

- 9.14 Ormat

- 9.15 Promec Engineering

- 9.16 Rentech Boilers

- 9.17 Siemens Energy

- 9.18 Sofinter

- 9.19 Thermax

- 9.20 Viessmann