|

市場調査レポート

商品コード

1844360

金属製造廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Metal Manufacturing Waste Heat Recovery System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 金属製造廃熱回収システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年09月19日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

概要

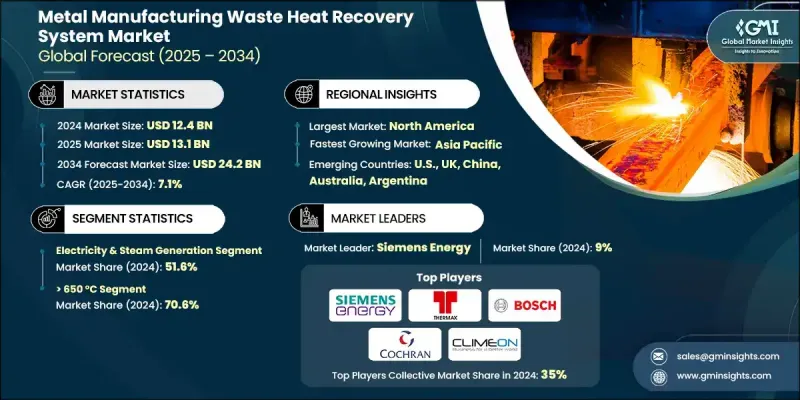

金属製造廃熱回収システムの世界市場規模は、2024年に124億米ドルとなり、CAGR 7.1%で成長し、2034年には242億米ドルに達すると予測されています。

製造業者が業務効率、持続可能性、全体的なエネルギー費用の削減に重点を置いているため、市場は着実な成長を続けています。圧延、鍛造、製錬、鋳造などの高温プロセスでは、大量の余剰熱エネルギーが発生します。廃熱回収システムは、このエネルギーを回収し、電気、蒸気、プロセス熱などの利用可能な形態に変換し、操業に再統合するように設計されています。これにより、エネルギー消費を大幅に削減し、排出量を削減し、企業が厳しい環境基準を遵守するのに役立ちます。世界的な規制機関が二酸化炭素削減とクリーン生産を推進する中、金属製造のようなエネルギー集約型産業への圧力は高まっています。これらのシステムは、企業が持続可能性の目標を推進しながら、一次エネルギー投入への依存を減らすのにも役立ちます。熱交換器技術、有機ランキンサイクル、熱電材料における最近の改良は、廃熱回収システムの性能と信頼性を高め、業界の成長と長期的な普及をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 124億米ドル |

| 予測金額 | 242億米ドル |

| CAGR | 7.1% |

2024年の電気・蒸気発電のシェアは51.6%で、2034年までのCAGRは8.1%と予測されます。廃熱回収システム(WHRS)の導入が、再生可能な取り組みや、新興地域における政府の支援による電化の取り組みの中で拡大していることが、需要を加速しています。また、産業廃棄物エネルギーを電力や蒸気の用途に再利用することへの注目が高まっていることも、特にインフラ整備の遅れている地域における市場の勢いにプラスの影響を与えています。

650 °C以上の温度セグメントは2024年に70.6%のシェアを占め、2034年までにCAGR 7%で成長すると予測されています。高温用途向けに設計されたシステムは、特に製錬・鋳造ライン内の直接回収セットアップにおいて、ますます重要になってきています。これらのシステムは、極端な排気流から直接熱を回収するため、加熱ステージを追加する必要がなく、熱効率が向上します。堅牢な構造により、転炉や高炉で一般的に見られる高ダスト・高熱環境に耐えることができ、集約的な産業環境での連続使用に最適です。

欧州金属製造廃熱回収システム市場は、厳しい環境指令、進化する鉄鋼業界の慣行、廃棄物発電インフラへの投資拡大に後押しされ、2034年までCAGR 6.6%で成長すると予想されます。これらのシステムは、光熱費の高騰や埋立地の利用制限に直面している都市部のエネルギー課題に対処する上で重要な役割を果たしており、高度な回収ソリューションに対する強い需要を生み出しています。

世界の金属製造廃熱回収システム市場をリードする企業には、シーメンス・エナジー、IHIコーポレーション、エコーゲン・パワー・システムズ、クライミオン、サーマックス、ボッシュ、プロメック・エンジニアリング、カニン・エナジー、三菱重工業、オーラ、フォーブス・マーシャル、ターボデン、CMRグリーン・テクノロジーズ、ファーストESCOインド、川崎重工業、ジョン・ウッド・グループ、コクラン、プライメタルズ・テクノロジーズ、ソフインター、CTP TEAMなどがあります。存在感を高めるため、各社は戦略的な製品開発、分野横断的な協力関係、技術革新に注力しています。各社は、過酷な環境条件や高粉塵用途など、幅広い産業要件を満たす、よりコンパクトで高効率の回収システムに投資しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への浸透

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:用途別、2021-2034

- 主要動向

- 予熱

- 電気と蒸気の発電

- 蒸気ランキンサイクル

- 有機ランキンサイクル

- カリーナサイクル

- その他

第6章 市場規模・予測:温度別、2021-2034

- 主要動向

- 230℃未満

- 230℃~650℃

- 650℃以上

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- AURA

- Bosch

- Climeon

- CMR Green Technologies Ltd.

- Cochran

- CTP TEAM

- Echogen Power Systems

- FirstESCO India Pvt. Ltd.

- Forbes Marshall

- IHI Corporation

- John Wood Group

- Kanin Energy

- Kawasaki Heavy Industries

- Mitsubishi Heavy Industries

- Primetals Technologies

- Promec Engineering

- Siemens Energy

- Sofinter

- Thermax

- Turboden