製造業におけるAIの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

AI in Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684785

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

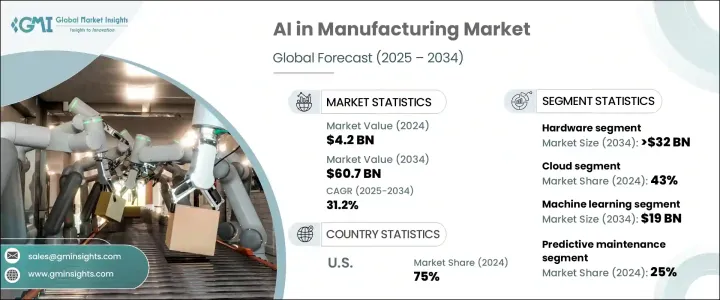

世界の製造業におけるAI市場は、2024年に42億米ドルと評価され、2025年から2034年にかけて31.2%のCAGRで成長すると予測されています。

製造業における合理化されたアウトソーシングソリューションへのニーズの高まりが、AIの採用を促進しています。企業は、生産管理、検査、在庫管理などのプロセスを自動化することで、生産効率を高め、コストを削減し、事業を拡大するためにAIを統合しています。AIを活用したソリューションの利用可能性の高まりは、大手メーカーから中小企業まで、あらゆる規模の企業に恩恵をもたらしています。世界各国の政府はAIの研究開発を優先しており、AIの導入を促進するための資金提供プログラム、税制優遇措置、規制支援などの財政的インセンティブを提供しています。これらのイニシアチブは、様々な業界においてイノベーションを促進し、生産性を向上させ、コストを削減することを目的としています。

市場はコンポーネントに基づいてハードウェア、ソフトウェア、サービスに区分されます。2024年には、ハードウェア分野の市場シェアが55%を超え、2034年には320億米ドルを超えると予想されています。ロボット工学、予知保全、品質管理などの製造業におけるAIアプリケーションは、リアルタイムのデータ処理に高性能なコンポーネントを必要とするため、高度なコンピューティングハードウェアに対する需要の高まりがこの成長を後押ししています。機械学習やディープラーニングのアルゴリズムも、AIの性能を向上させる強力なハードウェアの必要性を高めています。データ処理能力の急速な進歩により、自動化の拡大、生産性の向上、意思決定の改善が可能になりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 42億米ドル |

| 予測金額 | 607億米ドル |

| CAGR | 31.2% |

導入モデル別では、オンプレミスソリューションとクラウドソリューションに分類されます。2024年には、クラウドセグメントが市場の約43%を占めました。各業界の企業がデジタルトランスフォーメーションを取り入れる中、クラウドベースのAIソリューションの需要が高まり、製造業の競争力が強化されています。クラウドコンピューティングは柔軟性と拡張性を提供し、運用コストの削減とプロセスの合理化を実現します。さらに、遠隔地に導入することでデータの保存と処理を強化できるため、膨大なデータセットに依存するAIアプリケーションには不可欠です。また、クラウドベースのソリューションは、メーカー、サプライヤー、顧客間のリアルタイムのコラボレーションを可能にし、意思決定を改善し、市場投入までの時間を短縮します。

市場はまた、機械学習、コンピュータ・ビジョン、自然言語処理、コンテキスト対応コンピューティングなど、技術別に区分されます。機械学習は市場をリードし、2034年までに約190億米ドルを生み出すと予測されています。この成長は、インテリジェントな自動化とデータ主導の意思決定のための機械学習の使用の増加に起因しています。AI主導の品質管理ソリューションは、製品検査の精度を向上させ、生産ロスを最小限に抑えます。製造業における機械学習の採用は、最適化されたオペレーションのためにデータを収集、分析、処理するIoT技術の台頭によっても推進されています。

同市場はさらに、品質管理、予知保全、在庫管理、エネルギー管理、産業用ロボット、その他を含む用途別に分類されます。予知保全は2024年に約25%の最大シェアを占めました。AIを活用した予知保全ソリューションは、機械学習アルゴリズムを使用して機器の性能をリアルタイムで監視・評価し、故障の防止、保全コストの削減、生産中断の最小化を支援します。生産性の向上とダウンタイムの削減に対するニーズの高まりが、こうしたシステムの需要を促進しています。

米国は2024年の北米の製造業におけるAI市場をリードし、地域シェアの約75%を占めました。AI主導のスマート製造に対する同国の強力な政府支援が市場成長の主要因となっています。政策立案者は、国内の製造業の競争力を強化するため、自動化と先端技術を優先しています。さらに、サプライチェーンの強靭性の強化と生産効率の最適化に重点を置くことが、同産業におけるAIの採用をさらに促進しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- サービスプロバイダー

- テクノロジープロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース・イニシアチブ

- 規制状況

- 製造業におけるAIの進化

- 使用事例

- 影響要因

- 成長促進要因

- 自動化のニーズの高まり

- 機械学習技術の急速な開発

- AIを活用した予知保全ソリューションの採用

- 産業オートメーションへの投資の増加

- 業界の潜在的リスク・課題

- データプライバシーに関する懸念

- 熟練した専門家の不足

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- プロセッサー

- 中央処理装置(CPU)

- グラフィックス・プロセッシング・ユニット(GPU)

- フィールド・プログラマブル・ゲート・アレイ(FPGA)

- 特定用途向け集積回路(ASIC)

- テンソル・プロセッシング・ユニット(TPU)

- メモリー・ストレージ

- ネットワーキング・ハードウェア

- プロセッサー

- ソフトウェア

- サービス

- プロフェッショナル・サービス

- マネージドサービス

第6章 市場推計・予測:導入モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 機械学習

- コンピュータビジョン

- 自然言語処理

- コンテキスト対応コンピューティング

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 品質管理

- 予知保全

- 在庫管理

- エネルギー管理

- 産業用ロボット

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車

- エレクトロニクス

- 医薬品

- 重機

- 食品・飲料

- 航空宇宙・防衛

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ABB

- AWS

- Cognex

- Dassault

- Fanuc

- GE

- Honeywell

- IBM

- Intel

- Microsoft

- NVIDIA

- Oracle

- PTC

- Qualcomm

- Rockwell

- SAP

- Schneider

- Siemens

- Xilinx

目次

The Global AI In Manufacturing Market was valued at USD 4.2 billion in 2024 and is projected to grow at a CAGR of 31.2% between 2025 and 2034. The increasing need for streamlined outsourcing solutions within the manufacturing sector is driving AI adoption. Companies are integrating AI to enhance production efficiency, cut costs, and scale operations by automating processes such as production control, inspection, and inventory management. The rising availability of AI-powered solutions is benefiting businesses of all sizes, from large manufacturers to small and medium enterprises. Governments worldwide are prioritizing AI research and development, offering financial incentives such as funding programs, tax breaks, and regulatory support to boost AI implementation. These initiatives are designed to drive innovation, improve productivity, and reduce costs across various industries.

The market is segmented based on components into hardware, software, and services. In 2024, the hardware segment held a market share exceeding 55% and is expected to surpass USD 32 billion by 2034. The rising demand for advanced computing hardware is fueling this growth, as AI applications in manufacturing, such as robotics, predictive maintenance, and quality control, require high-performance components for real-time data processing. Machine learning and deep learning algorithms are also driving the need for powerful hardware to improve AI performance. Rapid advancements in data processing capabilities are enabling greater automation, enhanced productivity, and better decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $60.7 Billion |

| CAGR | 31.2% |

By deployment model, the market is categorized into on-premises and cloud solutions. In 2024, the cloud segment accounted for about 43% of the market. As companies across industries embrace digital transformation, the demand for cloud-based AI solutions is rising, enhancing competitiveness in manufacturing. Cloud computing offers flexibility and scalability, reducing operational costs and streamlining processes. Additionally, remote implementation allows for enhanced data storage and processing, which is critical for AI applications that rely on extensive datasets. Cloud-based solutions also enable real-time collaboration between manufacturers, suppliers, and customers, improving decision-making and accelerating time to market.

The market is also segmented by technology, including machine learning, computer vision, natural language processing, and context-aware computing. Machine learning led the market and is projected to generate around USD 19 billion by 2034. This growth is attributed to the increasing use of machine learning for intelligent automation and data-driven decision-making. AI-driven quality control solutions improve product inspection accuracy, minimizing production losses. Machine learning adoption in manufacturing is also being propelled by the rise of IoT technologies, which collect, analyze, and process data for optimized operations.

The market is further divided by application, including quality management, predictive maintenance, inventory management, energy management, industrial robotics, and others. Predictive maintenance held the largest share in 2024 at approximately 25%. AI-powered predictive maintenance solutions use machine learning algorithms to monitor and assess equipment performance in real-time, helping businesses prevent failures, reduce maintenance costs, and minimize production disruptions. The increasing need for higher productivity and reduced downtime is driving demand for these systems.

The United States led the North America AI in manufacturing market in 2024, holding about 75% of the regional share. The country's strong government support for AI-driven smart manufacturing is a key factor in market growth. Policymakers are prioritizing automation and advanced technologies to enhance the competitiveness of the nation's manufacturing sector. In addition, a focus on strengthening supply chain resilience and optimizing production efficiency is further driving AI adoption in the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Service providers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Evolution of AI in manufacturing

- 3.9 Use cases

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 The growing need for automation

- 3.10.1.2 Rapid developments in machine learning technologies

- 3.10.1.3 Adoption of AI-powered predictive maintenance solutions

- 3.10.1.4 Increasing investment in industrial automation

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Data privacy concerns

- 3.10.2.2 Lack of skilled professionals

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Processors

- 5.2.1.1 Central Processing Units (CPU)

- 5.2.1.2 Graphics Processing Units (GPU)

- 5.2.1.3 Field Programmable Gate Arrays (FPGA)

- 5.2.1.4 Application Specific Integrated Circuits (ASIC)

- 5.2.1.5 Tensor Processing Units (TPU)

- 5.2.2 Memory & storage

- 5.2.3 Networking hardware

- 5.2.1 Processors

- 5.3 Software

- 5.4 Services

- 5.4.1 Professional service

- 5.4.2 Managed service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Machine learning

- 7.3 Computer vision

- 7.4 Natural language processing

- 7.5 Context-aware computing

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Quality management

- 8.3 Predictive maintenance

- 8.4 Inventory management

- 8.5 Energy management

- 8.6 Industrial robotics

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Electronics

- 9.4 Pharmaceuticals

- 9.5 Heavy machinery

- 9.6 Food & beverage

- 9.7 Aerospace & defense

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 South Korea

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 UAE

- 10.5.2 South Africa

- 10.5.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 AWS

- 11.3 Cognex

- 11.4 Dassault

- 11.5 Fanuc

- 11.6 GE

- 11.7 Google

- 11.8 Honeywell

- 11.9 IBM

- 11.10 Intel

- 11.11 Microsoft

- 11.12 NVIDIA

- 11.13 Oracle

- 11.14 PTC

- 11.15 Qualcomm

- 11.16 Rockwell

- 11.17 SAP

- 11.18 Schneider

- 11.19 Siemens

- 11.20 Xilinx

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日