|

市場調査レポート

商品コード

1684712

自動車用パラレル・ハイブリッド・パワーシステム市場の機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Parallel Hybrid Power System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用パラレル・ハイブリッド・パワーシステム市場の機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

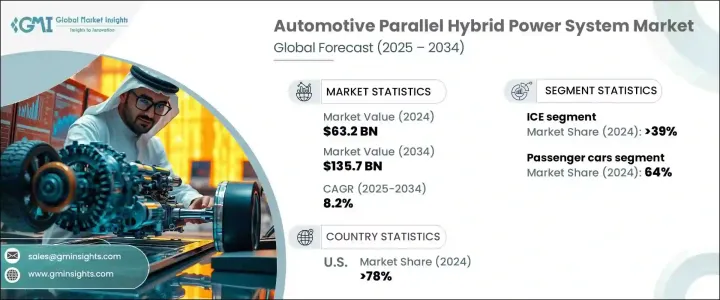

自動車用パラレル・ハイブリッド・パワーシステムの世界市場規模は、2024年に632億米ドルとなり、2025年から2034年にかけてCAGR 8.2%で成長すると予測されています。

温室効果ガスの排出削減と燃料効率の向上が重視されるようになり、市場は大きな勢いを見せています。世界各国の政府は、ハイブリッド電気自動車(HEV)の普及を促進するため、厳しい規制を実施し、インセンティブを提供しています。減税、補助金、EVインフラへの投資など、こうした政策により、ハイブリッド技術は消費者にとってより身近で魅力的なものとなっています。さらに、燃料価格の上昇と持続可能性への意識の高まりが、エネルギー効率の高いモビリティ・ソリューションへの消費者の嗜好を後押ししています。

自動車メーカーは、進化する規制基準と消費者の期待に応えるため、ハイブリッド車のポートフォリオを急速に拡大しています。回生ブレーキシステムや最適化されたバッテリー性能など、高度なパワートレイン技術の統合が進み、ハイブリッド車の効率と魅力がさらに高まっています。ハイブリッドパワーシステムが従来の内燃機関(ICE)車と完全な電気自動車とのギャップを埋め続けているため、その採用は世界市場で急増すると予想されます。競争力のある価格でハイブリッド・モデルを入手できるようになりつつあることも、特にEV充電インフラが未発達な地域での市場成長に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 632億米ドル |

| 予測金額 | 1,357億米ドル |

| CAGR | 8.2% |

市場は、電気モーター、内燃エンジン、バッテリー、パワーエレクトロニクス、トランスミッションシステムなどの主要コンポーネントに区分されます。内燃機関セグメントは、2024年の市場シェアの39%を占め、依然として優位を保っています。電動化へのシフトにもかかわらず、ICEベースのハイブリッド・システムは、よりクリーンな交通機関への移行において引き続き重要な役割を果たしています。ガソリンやディーゼルの燃料補給インフラが手頃な価格で広く利用できるため、特に新興経済諸国ではハイブリッド車が現実的な選択肢となっています。2034年には、燃費効率と排出ガス削減の技術進歩により、ICEセグメントは500億米ドルを超えると予想されます。

車種別では、自動車用パラレル・ハイブリッド・パワーシステム市場は、二輪車、乗用車、商用車に分類されます。乗用車は、消費者が低燃費で費用対効果の高い輸送ソリューションを優先するため、2024年には64%の市場シェアを獲得しました。ハイブリッド乗用車の需要は、交通渋滞と燃料費がエネルギー効率を最優先させる都市部で特に強いです。自動車メーカーは、パワートレイン性能の向上、バッテリー寿命の延長、スマート・テクノロジーのシームレスな統合を実現した革新的なハイブリッド・モデルを投入しており、性能と持続可能性のバランスを求める消費者にとって、ハイブリッド・モデルの魅力はますます高まっています。

米国は、自動車用パラレル・ハイブリッド・パワーシステムの最大市場であり続け、2024年の市場シェア全体の78%を占めています。同国の広範な道路網、堅牢なインフラ、燃費効率に対する消費者の意識の高まりが、採用を促進する主な要因となっています。国内メーカーがハイブリッド車の技術革新を主導していることから、米国は持続可能な輸送における技術進歩の主要拠点であり続けています。ハイブリッド車の需要が高まる中、自動車メーカーはハイブリッドパワートレインを改良し、エネルギー効率を向上させ、従来のガソリン車に代わるコスト効率の高い選択肢を提供するため、研究開発に多額の投資を行っています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- メーカー

- 流通チャネル

- サービスプロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- テクノロジーとイノベーションの展望

- ケーススタディ

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 政府の規制とインセンティブ

- 燃料価格の上昇とコスト効率

- 環境意識の高まり

- 技術の進歩

- 業界の潜在的リスク&課題

- バッテリー寿命の限界とリサイクルの問題

- 完全電気自動車との高い競合

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 電気モーター

- ICE

- バッテリー&エネルギー貯蔵システム

- パワーエレクトロニクス&コントローラー

- トランスミッション

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- 小型車

- 中型車

- SUVと高級車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 二輪車

第7章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- フルハイブリッドシステム

- マイルドハイブリッドシステム

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 都市交通

- 都市間移動

- オフハイウェイ用途

第9章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 回生ブレーキシステム

- 発進停止システム

- 電動アシストシステム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisin

- BorgWarner

- Continental

- Denso

- Hitachi Astemo

- Infineon

- LG Chem

- Magna

- Panasonic

- Bosch

- Samsung SDI

- Schaeffler

- Siemens

- Valeo

- ZF

- BYD

- Mitsubishi Electric

- Toyota Industries

- YASA

- Mahle

The Global Automotive Parallel Hybrid Power System Market was valued at USD 63.2 billion in 2024 and is projected to grow at a CAGR of 8.2% between 2025 and 2034. With a growing emphasis on reducing greenhouse gas emissions and enhancing fuel efficiency, the market is witnessing significant momentum. Governments worldwide are implementing stringent regulations and offering incentives to accelerate the adoption of hybrid electric vehicles (HEVs). These policies, including tax breaks, subsidies, and investment in EV infrastructure, are making hybrid technology more accessible and appealing to consumers. Additionally, rising fuel prices and increasing awareness of sustainability are driving consumer preferences toward energy-efficient mobility solutions.

Automakers are rapidly expanding their hybrid vehicle portfolios to meet evolving regulatory standards and consumer expectations. The growing integration of advanced powertrain technologies, including regenerative braking systems and optimized battery performance, is further enhancing the efficiency and appeal of hybrid vehicles. As hybrid power systems continue to bridge the gap between traditional internal combustion engine (ICE) vehicles and fully electric alternatives, their adoption is expected to surge across global markets. The increasing availability of hybrid models at competitive prices is also contributing to market growth, particularly in regions where EV charging infrastructure is still underdeveloped.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $63.2 Billion |

| Forecast Value | $135.7 Billion |

| CAGR | 8.2% |

The market is segmented into key components, including electric motors, internal combustion engines, batteries, power electronics, and transmission systems. The internal combustion engine segment remains dominant, accounting for 39% of the market share in 2024. Despite the shift toward electrification, ICE-based hybrid systems continue to play a crucial role in the transition to cleaner transportation. The affordability and widespread availability of gasoline and diesel refueling infrastructure make hybrid vehicles a practical choice, particularly in developing economies. By 2034, the ICE segment is expected to exceed USD 50 billion, driven by technological advancements in fuel efficiency and emissions reduction.

By vehicle type, the automotive parallel hybrid power system market is categorized into two-wheelers, passenger cars, and commercial vehicles. Passenger cars captured a 64% market share in 2024 as consumers prioritize fuel-efficient and cost-effective transportation solutions. The demand for hybrid passenger vehicles is particularly strong in urban areas, where traffic congestion and fuel costs make energy efficiency a top priority. Automakers are introducing innovative hybrid models with improved powertrain performance, extended battery life, and seamless integration of smart technologies, making them increasingly attractive to consumers seeking a balance between performance and sustainability.

The U.S. remains the largest market for automotive parallel hybrid power systems, accounting for 78% of the total market share in 2024. The country's extensive road networks, robust infrastructure, and increasing consumer awareness of fuel efficiency are key factors driving adoption. With domestic manufacturers leading the charge in hybrid vehicle innovation, the U.S. continues to be a major hub for technological advancements in sustainable transportation. As demand for hybrid vehicles rises, automakers are investing heavily in research and development to refine hybrid powertrains, improve energy efficiency, and offer cost-effective alternatives to traditional gasoline-powered vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distribution channels

- 3.1.4 Service providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Case studies

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Government regulations & incentives

- 3.8.1.2 Rising fuel prices & cost efficiency

- 3.8.1.3 Increasing environmental awareness

- 3.8.1.4 Technological advancements

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited battery life and recycling issues

- 3.8.2.2 High competition from fully electric vehicles

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric motor

- 5.3 ICE

- 5.4 Battery & energy storage systems

- 5.5 Power electronics & controllers

- 5.6 Transmission system

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Compact cars

- 6.2.2 Mid-size cars

- 6.2.3 SUVs & luxury cars

- 6.3 Commercial Vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Heavy commercial vehicles (HCVs)

- 6.4 Two-Wheelers

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Full hybrid system

- 7.3 Mild hybrid system

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Urban transportation

- 8.3 Intercity travel

- 8.4 Off-highway applications

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Regenerative braking systems

- 9.3 Start-stop systems

- 9.4 Electric-assist systems

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin

- 11.2 BorgWarner

- 11.3 Continental

- 11.4 Denso

- 11.5 Hitachi Astemo

- 11.6 Infineon

- 11.7 LG Chem

- 11.8 Magna

- 11.9 Panasonic

- 11.10 Bosch

- 11.11 Samsung SDI

- 11.12 Schaeffler

- 11.13 Siemens

- 11.14 Valeo

- 11.15 ZF

- 11.16 BYD

- 11.17 Mitsubishi Electric

- 11.18 Toyota Industries

- 11.19 YASA

- 11.20 Mahle