|

市場調査レポート

商品コード

1750415

オフハイウェイEVコンポーネントの市場機会、成長促進要因、産業動向分析、2025~2034年予測Off-highway EV Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| オフハイウェイEVコンポーネントの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月07日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

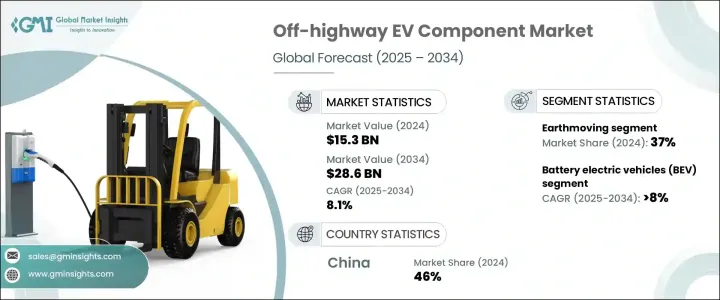

世界のオフハイウェイEVコンポーネント市場は、2024年には153億米ドルとなり、CAGR 8.1%で成長し、2034年には286億米ドルに達すると予測されています。

産業界が従来の内燃エンジンに代わるよりクリーンな選択肢を優先する中、排出ガスの削減、燃料消費の低減、メンテナンスコストの最小化を実現する電動式機器が支持を集めています。規制の義務化、排出ガス規制法、環境意識の高まりが、相手先商標製品メーカーに電動ソリューションへの投資を促しています。さらに、政府と民間部門は、スマートインフラとグリーン開発に多額の投資を行っており、オフハイウェイEVコンポーネントの需要をさらに高めています。

ローダー、ドーザー、クレーンなどの電動機器の採用は、大規模な都市開発やインフラ・プロジェクトの環境フットプリントの削減に不可欠です。電動化だけでなく、予測診断、フリート接続、スマートテレマティックスなどのデジタル技術の統合は、オフハイウェイ分野における作業効率を再定義しています。このような進歩は、過酷で高負荷の環境向けに調整された、高度に専門化された電子部品への需要に拍車をかけています。遠隔監視とリアルタイムのデータ機能を備えた機器は、より良い稼働時間とライフサイクルコスト管理をサポートし、フリートオペレータが現場作業におけるパフォーマンスを最適化するのに役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 153億米ドル |

| 予測金額 | 286億米ドル |

| CAGR | 8.1% |

多様なプロジェクト現場での電動掘削機、ローダー、および同様の機器の高い使用率に牽引され、アプリケーションカテゴリの中で、土木分野が2024年に37%のシェアを占め、最大シェアを獲得しました。土工機械は、その一貫した使用パターンと、排ガス規制区域で操業する必要性が高まっていることから、電動化に適しています。OEMとシステムサプライヤーは、公共プロジェクトと民間プロジェクトの両方で高まる需要を満たすため、次世代バッテリーパック、電気ドライブトレイン、冷却システムで対応しています。

2024年のオフハイウェイEVコンポーネント市場では、バッテリー式電気自動車(BEV)が66%のシェアを占め、最も大きな割合を占める。BEVはまた、燃料消費量の低減、機械的複雑さの低減、メンテナンス要件の最小化により、運転効率と長期的なコストメリットも提供します。トンネル、密集した都市部の作業現場、屋内農業施設など、閉鎖的または制限された環境への適合性は、その有用性をさらに高めます。また、BEVの静かな動作音は、騒音規制のある環境でもますます好まれるようになり、複数のオフハイウェイ分野での幅広い採用を支えています。

中国オフハイウェイEVコンポーネント市場シェアは46%で、2024年には32億5,000万米ドルを創出します。これは、産業排出物の削減と設備効率の改善を目的とした国家政策による一貫した支援に支えられています。特にバッテリー生産と電動パワートレイン技術において高度な製造能力を持つ中国は、高性能なEVコンポーネントを大規模に供給しています。この国の包括的なEVインフラは、農業、鉱業、建設部門への広範な配備と相まって、引き続きリーダーシップを強化し、この地域全体の市場拡大を加速させています。

市場ポジションを強化するため、Tata Elxsi, Volvo AB, Komatsu, Liebherr, and Deere & Companyなどの企業は、垂直統合と長期的提携に注力しています。次世代バッテリーシステム、パワーエレクトロニクス、デジタルプラットフォームへの戦略的投資により、これらの企業は電動化の動向をリードすることができます。技術プロバイダーとの提携や、カスタマイズされたソリューションの共同開発により、これらの企業はコスト競争力を維持しながら、セクター固有のニーズに応えることができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- ティア1自動車部品サプライヤー

- オフハイウェイシステムに特化したインテグレーター

- オフハイウェイ車両OEM

- テクノロジープロバイダー

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 価格動向

- 地域

- 成分

- コスト内訳分析

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界各国政府は温室効果ガスの排出を抑制するためにますます厳しい規制を実施しています

- 建設、鉱業、農業機械の電動化

- バッテリーとモーター技術の進歩

- スマートシティ、鉱業の自動化、機械化農業への投資の増加

- OEMとティア1サプライヤーのコラボレーション

- 業界の潜在的リスク&課題

- 初期購入コストが高め

- バッテリー技術の限界

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- バッテリーパック

- 電気モーター

- コントローラー

- インバーター

- パワーエレクトロニクス

- 熱管理システム

- 車載充電器

- 電動パワーステアリングシステム

- その他

第6章 市場推計・予測:推進力別、2021-2034

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

- 燃料電池電気自動車(FCEV)

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- マテリアルハンドリング

- 土木工事

- 収穫

- 輸送と運搬

- 掘削と発破

第8章 市場推計・予測:車両別、2021-2034

- 主要動向

- 電気建設車両

- 掘削機

- ブルドーザー

- ローダー

- 電気農業用車両

- トラクター

- 収穫機

- 噴霧器

- 電気鉱山車両

- 運搬トラック

- ドリル

- その他

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- オリジナル機器メーカー(OEM)

- アフターマーケット

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Bell Equipment

- Caterpillar

- CNH Industrial

- Dana

- Deere &Company

- Doosan

- Epiroc

- Hitachi Construction Machinery

- JCB

- Komatsu

- Kubota

- Liebherr

- Manitou Group

- Sandvik

- Sona Comstar

- Sumitomo Heavy Industries

- Tata AutoComp

- Tata Elxsi

- Terex

- Volvo AB

The Global Off-highway EV Component Market was valued at USD 15.3 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 28.6 billion by 2034, fueled by the accelerating transition toward electrified construction, mining, and agricultural machinery. As industries prioritize cleaner alternatives to traditional combustion engines, electric-powered equipment is gaining traction for reduced emissions, lower fuel consumption, and minimized maintenance costs. Regulatory mandates, emission control laws, and rising environmental awareness are pressuring original equipment manufacturers to invest in electric solutions. Additionally, governments and private sectors are investing heavily in smart infrastructure and green development, further increasing the demand for off-highway EV components.

The adoption of electric equipment such as loaders, dozers, and cranes is essential in reducing the environmental footprint of major urban development and infrastructure projects. Beyond electrification, the integration of digital technologies-such as predictive diagnostics, fleet connectivity, and smart telematics-is redefining operational efficiency in off-highway segments. These advancements fuel demand for highly specialized electronic components tailored for rugged, high-duty environments. Equipment with remote monitoring and real-time data capabilities supports better uptime and lifecycle cost control, helping fleet operators optimize performance in field operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.3 Billion |

| Forecast Value | $28.6 Billion |

| CAGR | 8.1% |

Among application categories, the earthmoving segment captured the largest share in 2024, accounting for 37% share, driven by the high usage of electric excavators, loaders, and similar equipment across diverse project sites. Earthmoving machinery is well-suited for electrification, given its consistent usage patterns and the increasing need to operate in emission-regulated zones. OEMs and system suppliers are responding with next-gen battery packs, electric drivetrains, and cooling systems to meet growing demand in both public and private projects.

In 2024, battery electric vehicles (BEVs) captured the largest portion in the off-highway EV component market, making up 66% share, driven by their ability to operate without tailpipe emissions, a major advantage in today's push for greener construction and mining operations. BEVs also offer operational efficiency and long-term cost benefits, thanks to lower fuel consumption, reduced mechanical complexity, and minimal maintenance requirements. Their compatibility with closed or restricted environments, such as tunnels, dense urban job sites, and indoor agriculture facilities, further enhances their utility. The quiet operation of BEVs also makes them increasingly favored in noise-regulated environments, supporting broader adoption across multiple off-highway sectors.

China Off-highway EV Component Market held 46% share and generated USD 3.25 billion in 2024, underpinned by consistent support from national policies aimed at reducing industrial emissions and improving equipment efficiency. With advanced manufacturing capabilities, especially in battery production and electric powertrain technologies, China supplies high-performance EV components at scale. The nation's comprehensive EV infrastructure, combined with widespread deployment across agriculture, mining, and construction sectors, continues to reinforce its leadership and accelerate the region's overall market expansion.

To reinforce their market positions, companies such as Tata Elxsi, Volvo AB, Komatsu, Liebherr, and Deere & Company are focusing on vertical integration and long-term collaborations. Strategic investments in next-gen battery systems, power electronics, and digital platforms enable these firms to lead electrification trends. Partnerships with tech providers and co-development of customized solutions allow these players to cater to sector-specific needs while maintaining cost competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Tier 1 automotive suppliers

- 3.2.3 Specialized off-highway system integrators

- 3.2.4 Off-highway vehicle OEM

- 3.2.5 Technology providers

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.6.1 Region

- 3.6.2 Component

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Governments worldwide are implementing increasingly strict regulations to curb greenhouse gas emissions

- 3.11.1.2 Electrification of construction, mining & agriculture equipment

- 3.11.1.3 Advancements in battery & motor technologies

- 3.11.1.4 Increased investments in smart cities, mining automation, and mechanized agriculture

- 3.11.1.5 OEM & tier-1 supplier collaborations

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial purchase cost

- 3.11.2.2 Battery technology limitations

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Battery packs

- 5.3 Electric motors

- 5.4 Controllers

- 5.5 Inverters

- 5.6 Power electronics

- 5.7 Thermal management systems

- 5.8 Onboard chargers

- 5.9 Electric power steering systems

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEV)

- 6.3 Plug-in hybrid electric vehicles (PHEV)

- 6.4 Hybrid electric vehicles (HEV)

- 6.5 Fuel cell electric vehicles (FCEV)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Material handling

- 7.3 Earthmoving

- 7.4 Harvesting

- 7.5 Transport & hauling

- 7.6 Drilling & blasting

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Electric construction vehicles

- 8.2.1 Excavators

- 8.2.2 Bulldozers

- 8.2.3 Loaders

- 8.3 Electric agricultural vehicles

- 8.3.1 Tractors

- 8.3.2 Harvesters

- 8.3.3 Sprayers

- 8.4 Electric mining vehicles

- 8.4.1 Haul trucks

- 8.4.2 Drills

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Original Equipment Manufacturers (OEM)

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Bell Equipment

- 11.2 Caterpillar

- 11.3 CNH Industrial

- 11.4 Dana

- 11.5 Deere & Company

- 11.6 Doosan

- 11.7 Epiroc

- 11.8 Hitachi Construction Machinery

- 11.9 JCB

- 11.10 Komatsu

- 11.11 Kubota

- 11.12 Liebherr

- 11.13 Manitou Group

- 11.14 Sandvik

- 11.15 Sona Comstar

- 11.16 Sumitomo Heavy Industries

- 11.17 Tata AutoComp

- 11.18 Tata Elxsi

- 11.19 Terex

- 11.20 Volvo AB