|

市場調査レポート

商品コード

1998730

食品用漂白剤市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Food Bleaching Agent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 食品用漂白剤市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月09日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

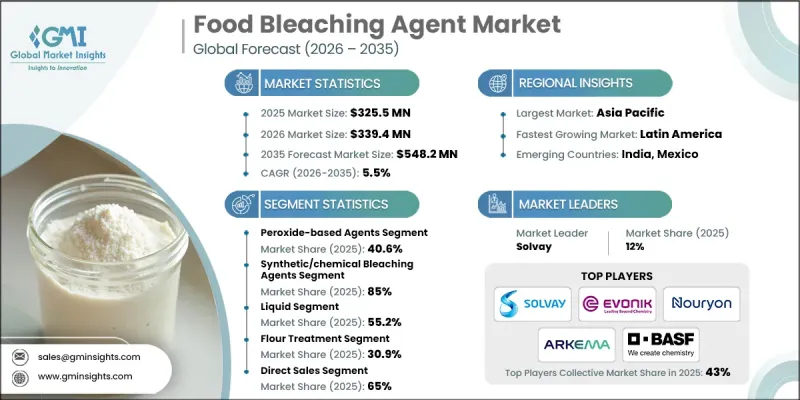

世界の食品用漂白剤市場は、2025年に3億2,550万米ドルと評価され、CAGR 5.5%で成長し、2035年までに5億4,820万米ドルに達すると推定されています。

食品用漂白剤は、製品の見た目を維持しつつ、食感を向上させ、加工効率全体を改善するのに役立つため、現代の食品製造において極めて重要な役割を果たしています。これらの薬剤は、生産者が原材料の特性を均一にするのを支援し、メーカーが大規模な生産ロット全体で一貫性を維持できるようにします。時が経つにつれ、漂白剤の価値提案は、単なる色の調整にとどまらず、複雑な製造プロセスにおける機能性の向上にまで拡大しています。また、市場の発展には、進化する規制枠組みや変化する消費者の期待に応えるために設計された、化学的および天然由来の配合における継続的なイノベーションも影響を与えています。消費パターンの変化により、食品メーカーは、視覚的な品質と信頼性の高い加工性能を維持するパッケージ食品に注力するようになっています。同時に、消費者は、品質の向上や最小限の加工といったイメージに合致する食品をますます求めるようになっています。その結果、業界関係者は、特に食品原料に対する規制当局の監視や消費者の目が厳しい地域において、天然由来または植物由来の代替配合を徐々に模索しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 3億2,550万米ドル |

| 予測額 | 5億4,820万米ドル |

| CAGR | 5.5% |

過酸化物系漂白剤セグメントは、2025年に40.6%のシェアを占め、2035年までCAGR 6.1%で成長すると予測されています。これらの薬剤は、その強力な酸化特性と信頼性の高い運用性能により、食品加工業界全体で広く採用され続けています。その化学的安定性により、大容量の生産環境でも効果的に機能するため、一貫性があり信頼性の高い原料処理を必要とする産業用加工システムに適しています。過酸化物系薬剤が安定した加工条件を維持できる能力は、世界の食品用漂白剤市場において、好まれるソリューションとしての地位をさらに強固なものにしています。

合成または化学系漂白剤セグメントは85%のシェアを占めており、2026年から2035年にかけてCAGR5.1%で成長すると予想されています。これらの薬剤は、大規模な食品製造の要件に合致する高い反応性と一貫した結果を提供するため、業界を支配し続けています。その予測可能な化学的性能により、生産者は複数の製品カテゴリーにわたって均一な製品外観と安定した加工条件を実現できます。さらに、迅速な色補正、強力な酸化作用、そして信頼性の高い加工性能が求められる産業環境においては、一貫した生産スケジュールと標準化された製品品質を維持するために、合成漂白剤が不可欠であり続けています。

北米の食品用漂白剤市場は、2025年に47.4%のシェアを占めました。同地域は、高度に発達した食品製造インフラと、一貫した製品品質を重視する厳格な食品安全基準により、戦略的に重要な市場へと発展しました。先進的な生産技術と確立された加工施設の存在により、同地域の企業は技術的に高度な漂白剤配合を迅速に導入することが可能となっています。また、強力な製造能力は大規模な食品生産活動を支え、効率的で信頼性の高い食品用漂白剤に対する地域の需要をさらに強めています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 視覚的な訴求力を高める加工・包装食品への需要の高まり

- 製パン・菓子類用途における漂白剤の採用拡大

- 天然および合成食品漂白剤における技術的進歩

- 業界の潜在的リスク&課題

- クリーンラベルや天然成分に対する消費者の嗜好の高まり

- 市場の成長に影響を与える合成漂白剤に関連する潜在的な健康上の懸念

- 市場機会

- 天然由来および植物由来の代替品の開発

- 酵素漂白技術の商業化

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 剤型別

- 将来の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:薬剤の種類別、2022-2035

- 過酸化物系薬剤

- 塩素系薬剤

- 物理吸着剤

- 亜硫酸塩系薬剤

- 酵素系漂白剤

- 天然・植物由来の代替品

- 過酸系薬剤

- その他の化学系薬剤

第6章 市場推計・予測:ソース別、2022-2035

- 合成/化学系漂白剤

- 天然/植物由来の漂白剤

- 鉱物由来の漂白剤

第7章 市場推計・予測:形態別、2022-2035

- 液体

- 粉末

- 顆粒

第8章 市場推計・予測:用途別、2022-2035

- 小麦粉処理

- 食用油脂

- ベーカリー・菓子類製品

- 乳製品

- 澱粉・糖類製品

- 飲料

- 無菌包装

- 食肉・家禽加工

- 卵製品

- 香辛料・ハーブ

- その他

第9章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 販売代理店・卸売業者

- オンラインチャネル

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- Solvay

- Evonik Industries AG

- BASF SE

- AkzoNobel N.V.

- Arkema S.A.

- Nouryon

- Aditya Birla Chemicals

- Kemira Oyj

- Clariant AG

- Imerys S.A.

- Kemin Industries

- DSM-Firmenich