車両追跡デバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vehicle Tracking Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666569

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

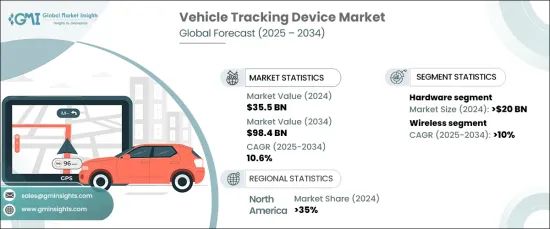

車両追跡デバイスの世界市場は、2024年に355億米ドルとなり、2025年から2034年にかけてCAGR10.6%で成長すると予測されています。

この急速な拡大は、車両管理におけるリアルタイムの追跡ソリューションに対する需要の増加、車両盗難に対する懸念の高まり、さまざまな業界における高度なテレマティクス技術の採用の高まりが主な要因となっています。企業が業務効率、セキュリティ、コスト管理を優先し続ける中、車両追跡デバイスは資産の監視、ルートの最適化、車両と商品の安全確保に不可欠なツールとなっています。実際、こうした機器の能力を高めるための戦略的パートナーシップも生まれつつあります。例えば、2024年3月、HERE Technologiesは、オーストラリアの商用車向け資産管理とナビゲーションサービスを改善するため、ネットスターと提携しました。

こうしたソリューションへの関心が高まっている背景には、コネクテッドデバイスとモノのインターネット(IoT)の急増があります。この動向は、物流業界や公共交通システムなど、商品のタイムリーな配送に追跡システムが不可欠な役割を果たす業界において特に顕著です。消費者も企業も同様に、業務効率の向上、セキュリティ、タイムリーな配送など、車両追跡の数多くの利点を認識しているため、市場は大幅な成長を遂げる態勢を整えています。特に、GPS追跡デバイスは、2032年までに約90億米ドルの収益が予測され、年間成長率は12%を超えて、市場を活性化させることが期待されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 355億米ドル |

| 予測金額 | 984億米ドル |

| CAGR | 10.6% |

車両追跡デバイス市場は、ハードウェアとソフトウェアコンポーネントに区分されます。2024年には、ハードウェアセグメントは200億米ドル以上の金額を占め、急速な拡大を続けています。企業が資産を管理するための信頼性が高く効率的なソリューションを求めているため、高品質のテレマティクスシステムとGPSデバイスに対する需要が高まっていることが、この成長の原動力となっています。Monimotoが2024年6月にリリースしたMonimoto 9のようなGPS追跡技術の進歩は、業界のイノベーションへのコミットメントを示しています。この新バージョンは、オートバイ、ボート、トレーラーなど、さまざまな資産の保護を強化します。

さらに、市場は接続性によって分類され、無線追跡装置は2025年から2034年にかけてCAGRが10%を超えると予測されています。無線セグメントの成長は主に、設置の容易さ、拡張性、リアルタイムデータ機能によるものです。IoTアプリケーションの継続的な開発も推進力となっており、企業は高度な追跡機能を活用し、より優れたデータ分析と遠隔監視によって業務を最適化できます。

北米は、2024年の世界の車両追跡デバイス市場の35%以上を占めました。この優位性は主に厳しい規制と確立された物流部門に起因します。同地域では、車両管理のためのリアルタイムの追跡ソリューションへの依存度が高く、企業が規制要件を満たし安全基準を強化するためにテレマティクスシステムを統合するなど、市場の需要を刺激し続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場範囲・定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- コンポーネントプロバイダー

- サービスプロバイダー

- メーカー

- 流通業者

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- コスト分析

- ケーススタディ

- 影響要因

- 成長促進要因

- 自動車の安全性に対する懸念の高まり

- 車両盗難件数の急増

- AIを活用した事故検知の増加

- 車両管理ニーズの高まり

- 業界の潜在的リスク・課題

- データとプライバシーに関する懸念

- 初期コストの高さ

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- OBDデバイス/トラッカー・アドバンストラッカー

- 独立型トラッカー

- ソフトウェア

- フリート管理プラットフォーム

- データ分析ツール

- マッピング・ナビゲーションシステム

- リアルタイム追跡ソフトウェア

- その他

第6章 市場推計・予測:接続性別、2021年~2034年

- 主要動向

- 有線

- 無線

第7章 市場推計・予測:通信トラッカー別、2021年~2034年

- 主要動向

- セルラーネットワーク

- 衛星通信

- デュアルモード

第8章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 運輸・物流

- 建設

- 石油・ガス

- 鉱業

- 緊急サービス

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- AT&T Intelligence

- ATrack Technology

- CalAmp

- Concox Information Technology

- Continental

- Garmin

- Geotab

- Laipac Technology

- Laird

- Meitrack

- Queclink Wireless Solutions

- Sensata

- Starcom Systems

- Suntech International

- Teletrac Navman

- Teltonika

- TomTom International

- Trackimo

- Vamosys

- Verizon Communications

目次

The Global Vehicle Tracking Device Market was valued at USD 35.5 billion in 2024 and is projected to grow at a CAGR of 10.6% from 2025 to 2034. This rapid expansion is largely driven by the increasing demand for real-time tracking solutions in fleet management, heightened concerns about vehicle theft, and the rising adoption of advanced telematics technologies across a variety of industries. As businesses continue to prioritize operational efficiency, security, and cost management, vehicle tracking devices have become indispensable tools for monitoring assets, optimizing routes, and ensuring the safety of vehicles and goods. In fact, strategic partnerships are emerging to boost the capabilities of these devices. For example, in March 2024, HERE Technologies teamed up with Netstar to improve asset management and navigation services for commercial vehicles in Australia.

The growing interest in these solutions can be attributed to the surge in connected devices and the Internet of Things (IoT), which enable businesses to capture and analyze real-time data to make better-informed decisions. This trend is particularly significant in industries like logistics, where tracking systems play an essential role in ensuring the timely delivery of goods, as well as in public transport systems. With consumers and businesses alike recognizing the numerous advantages of vehicle tracking, such as enhanced operational efficiency, security, and timely deliveries, the market is poised for substantial growth. In particular, GPS tracking devices are expected to fuel the market, with a projected revenue of around USD 9 billion by 2032 and an annual growth rate surpassing 12%.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.5 Billion |

| Forecast Value | $98.4 Billion |

| CAGR | 10.6% |

The vehicle tracking device market is segmented into hardware and software components. In 2024, the hardware segment accounted for over USD 20 billion in value and continues to expand rapidly. The increasing demand for high-quality telematics systems and GPS devices is driving this growth as businesses seek reliable, efficient solutions for managing their assets. Notably, advancements in GPS tracking technology, such as Monimoto's release of the Monimoto 9 in June 2024, illustrate the industry's commitment to innovation. This new version provides enhanced protection for various assets, including motorcycles, boats, and trailers.

Additionally, the market is categorized by connectivity, with wireless tracking devices projected to experience a CAGR of over 10% from 2025 to 2034. The wireless segment's growth is mainly due to the ease of installation, scalability, and the real-time data capabilities it offers. The continuous development of IoT applications is also a driving force, enabling businesses to harness advanced tracking functionalities and optimize their operations through better data analytics and remote monitoring.

North America accounted for more than 35% of the global vehicle tracking device market in 2024. This dominance is primarily attributed to stringent regulations and a well-established logistics sector. The region's heavy reliance on real-time tracking solutions for fleet management continues to fuel market demand, with companies integrating telematics systems to meet regulatory requirements and enhance safety standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Service providers

- 3.2.3 Manufacturers

- 3.2.4 Distributors

- 3.2.5 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Cost analysis

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing concerns over vehicle safety

- 3.9.1.2 Surge in number of vehicle thefts

- 3.9.1.3 Rising integration of AI-based accident detection

- 3.9.1.4 Increasing need for fleet management

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Data and privacy concerns

- 3.9.2.2 High initial cost

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 OBD device/ tracker and advance tracker

- 5.2.2 Standalone tracker

- 5.3 Software

- 5.3.1 Fleet management platforms

- 5.3.2 Data analytics tools

- 5.3.3 Mapping and navigation systems

- 5.3.4 Real-time tracking software

- 5.3.5 Others

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Wired

- 6.3 Wireless

Chapter 7 Market Estimates & Forecast, By Communication Tracker, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Cellular networks

- 7.3 Satellite

- 7.4 Dual mode

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Transportation & logistics

- 9.3 Construction

- 9.4 Oil & gas

- 9.5 Mining

- 9.6 Emergency services

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AT&T Intelligence

- 11.2 ATrack Technology

- 11.3 CalAmp

- 11.4 Concox Information Technology

- 11.5 Continental

- 11.6 Garmin

- 11.7 Geotab

- 11.8 Laipac Technology

- 11.9 Laird

- 11.10 Meitrack

- 11.11 Queclink Wireless Solutions

- 11.12 Sensata

- 11.13 Starcom Systems

- 11.14 Suntech International

- 11.15 Teletrac Navman

- 11.16 Teltonika

- 11.17 TomTom International

- 11.18 Trackimo

- 11.19 Vamosys

- 11.20 Verizon Communications

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日