|

市場調査レポート

商品コード

1892823

盗難車両回収市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Stolen Vehicle Recovery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 盗難車両回収市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月08日

発行: Global Market Insights Inc.

ページ情報: 英文 206 Pages

納期: 2~3営業日

|

概要

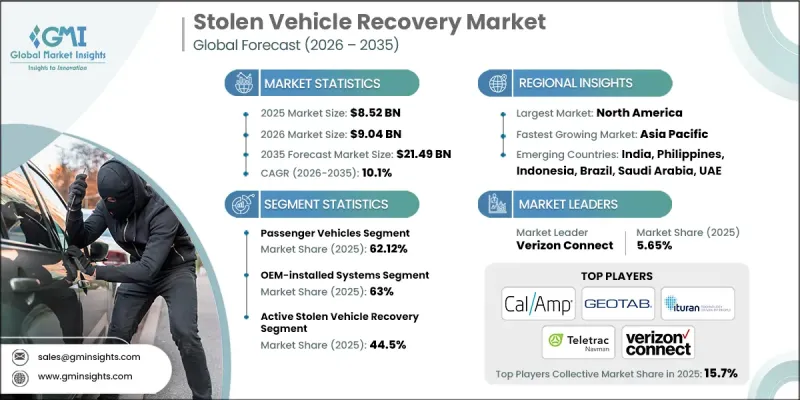

世界の盗難車両回収市場は、2025年に85億2,000万米ドルと評価され、2035年までにCAGR10.1%で成長し、214億9,000万米ドルに達すると予測されています。

市場拡大の背景には、コネクテッドカーアーキテクチャ、インテリジェントテレマティクス、組み込みセキュリティモジュールの急速な普及があり、これにより盗難車両回収(SVR)のエコシステムが変革されています。現代のSVRシステムは、GNSS測位、セルラーおよびIoT接続、AIベースの分析機能を統合し、リアルタイム車両追跡、ジオフェンシング、遠隔エンジン停止、行動異常検知を実現します。自動車メーカー、保険会社、フリート運営者は、盗難損失の削減、回収の迅速化、ドライバーの安全強化のために、統合型SVRソリューションへの依存度を高めています。これらの技術は、手動介入を最小限に抑え、継続的な車両監視をサポートし、乗用車および商用車両の両方におけるサイバーセキュリティを強化します。戦略的投資、プラットフォーム統合、業界横断的なパートナーシップが競合情勢を再構築しています。主要なテレマティクスプロバイダーは高感度GNSSモジュール、次世代IoTモデム、クラウドベースの指令センターを導入している一方、自動車部品サプライヤーは暗号化通信、妨害対策センサー、相互運用可能なAPIに注力し、世界の普及を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 85億2,000万米ドル |

| 予測金額 | 214億9,000万米ドル |

| CAGR | 10.1% |

乗用車セグメントは2025年に62.12%のシェアを占め、2035年までCAGR9.8%で成長すると予測されています。車両盗難への懸念の高まり、コネクテッドカーの普及、中所得層および高級車所有者の増加が、個人車両向けGPS追跡、ジオフェンシング、遠隔エンジン停止システムの導入を促進しています。

OEM搭載システムセグメントは2025年に63%のシェアを占め、2026年から2035年にかけてCAGR 10.4%で成長すると予測されています。工場出荷時搭載のテレマティクスおよびコネクテッドカープラットフォームは、高い信頼性、精度、車両電子機器との統合性を提供します。OEMソリューションは、メーカーのコネクテッドカーエコシステムを通じて、リモートイモビライゼーション、ジオフェンシング、不正操作警報、自動盗難通知などの機能を直接実現し、アフターマーケット設置の必要性を低減します。

米国における盗難車両回収(SVR)市場は2025年に85%のシェアを占め、28億9,000万米ドルの規模となりました。この成長は、テレマティクスの普及拡大、IoT接続性、AIを活用した分析技術の進展により推進されており、都市部における車両盗難率の上昇や複雑化する犯罪ネットワークへの対応が背景にあります。フリート事業者、保険会社、OEM各社は、財務損失の軽減、回収の迅速化、ドライバーの安全向上を目的として、高度なSVRプラットフォームの導入を加速させています。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 自動車盗難率の上昇と高度化する自動車盗難ネットワーク

- 拡大する技術革新(GPS、IoT、AI/機械学習)

- SVR設置に対する保険優遇措置の拡充

- 拡大するフリート運営、ライドシェアリング、物流セクター

- 業界の潜在的リスク&課題

- SVR導入およびサブスクリプションの高コスト

- データプライバシーとサイバーセキュリティに関する懸念事項

- 市場機会

- 新興市場における拡大(自動車所有台数の増加に伴い)

- スマートシティ構想および公共安全ネットワークとの統合

- AIを活用した予測分析および付加価値サービスの開発

- OEM、保険会社、フリート管理者間の戦略的パートナーシップ

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- GPSベースの追跡技術

- 無線周波数(RF)技術

- ハイブリッド技術システム

- 新興技術

- ジオフェンシング及び仮想境界技術

- 5Gネットワーク統合

- モノのインターネット(IoT)及びLPWAN技術

- 現在の技術動向

- 特許分析

- 価格分析

- 地域別

- サブスクリプションおよびサービス価格設定

- コスト内訳分析

- 製造・組立コスト

- ソフトウェア及びプラットフォーム開発費用

- ネットワーク及び接続コスト

- 顧客獲得コスト(CAC)

- 設置・稼働費用

- 研究開発費

- 持続可能性と環境影響分析

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- ビジネスケースとROI分析

- 総所有コスト(TCO)フレームワーク

- ROI算出調査手法

- 導入スケジュールとマイルストーン

- リスク評価と軽減策

- 消費者行動と普及動向

- 導入ライフサイクル分析

- セグメント別技術採用曲線

- 地域別の採用パターン

- 世代別の採用差異

- 季節的・時間的普及パターン

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:車両別、2022-2035

- 主要動向

- 乗用車

- ハッチバック車

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第6章 市場推計・予測:設備別、2022-2035

- 主要動向

- OEM搭載システム

- アフターマーケット

第7章 市場推計・予測:技術別、2022-2035

- 主要動向

- GPSベースの追跡システム

- 無線周波数(RF)システム

- セルラーおよびテレマティクスプラットフォーム

- ハイブリッドシステム(GPS+RF)

- その他

第8章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 個人車両所有者

- フリート所有者

- 保険会社

- 政府・法執行機関

- その他

第9章 市場推計・予測:用途別、2022-2035

- 主要動向

- 盗難車両の回収

- フリート管理およびセキュリティ

- 保険テレマティクスおよび使用量ベース保険(UBI)

- 自動車ディーラー向けソリューション

- 資産・設備追跡

- その他

第10章 市場推計・予測:サービスモデル別、2022-2035

- 主要動向

- ハードウェア+サブスクリプション

- 統合サービスプラン

- 単品購入

- 企業/フリート向けライセンシング

第11章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域(MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界プレイヤー

- CalAmp

- General Motors

- Geotab

- Robert Bosch

- Spireon

- Verizon Communications

- Vodafone Automotive

- 地域プレイヤー

- Ituran Location &Control

- MiX Telematics

- Netstar(Altron)

- Samsara

- Teletrac Navman

- TomTom International

- 新興企業

- 3 Si Security Systems

- Ford Pro

- Lytx

- Matrack

- Powerfleet

- Quartix Technologies

- RecovR

- StarChase

- Telematica

- TRACKMATIC

- Trimble

- Zubie