|

市場調査レポート

商品コード

1665403

スマートテールゲート市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Smart Tailgate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スマートテールゲート市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月27日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

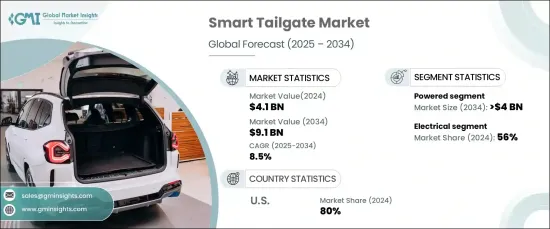

スマートテールゲートの世界市場は、2024年に41億米ドルと評価され、2025~2034年にかけてCAGR 8.5%で成長すると予測されています。

この拡大は、先進的車載オートメーションと利便性機能に対する需要の増加が主要要因です。自動車メーカー各社は、革新的な技術を取り入れるために車両インターフェースを継続的に強化しています。自動開閉機能を備えたスマートテールゲートシステムは、ハンズフリーアクセスを提供し、重い荷物を管理するユーザーにとって特に有用です。ユーザーフレンドリーで技術先進的なソリューションの重視は、現代の自動車における利便性の向上を求める消費者の嗜好と一致しています。

さらに、SUVやクロスオーバーなどの大型車の人気が高まっていることも、スマートテールゲートの採用を大幅に後押ししています。これらのシステムは、障害物を検知するセンサを統合することで、負傷や損傷のリスクを低減するため、安全性とセキュリティの強化も市場の成長を後押ししています。自動車の安全機能が進化し続けていることは、機能性とユーザー満足度の向上におけるこれらの技術の重要性を浮き彫りにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 41億米ドル |

| 予測金額 | 91億米ドル |

| CAGR | 8.5% |

市場は、手動、電動、ハンズフリーオプションにセグメント化され、2024年の市場シェアは電動式が50%以上を占めました。2034年までに、このセグメントは40億米ドルを超えると予測され、便利でハイテクな車両機能に対する消費者の欲求の高まりを反映しています。電動スマートテールゲートの自動車への統合は、進化する期待に応え、競合を強化しようとする自動車メーカーの努力を示すものです。

スマートテールゲートの機構には、電気、油圧、空気圧があります。2024年の市場シェアは電気システムが56%を占め、操作しやすくエネルギー効率の高いソリューションを求める消費者の需要が牽引しています。これらのシステムは、ボタン操作による開閉などの機能により、テールゲートの制御を簡素化します。シームレスでコードレスな操作は、スマートでエコフレンドリー車への嗜好の高まりに沿いつつ、効率性とアクセシビリティを向上させています。キーレスエントリーやリモートコントロールのような先進技術の組み込みは、ユーザーの利便性をさらに高め、電動スマートテールゲートシステムの魅力を強化しています。

北米では、米国が2024年のスマートテールゲート市場の80%という驚異的なシェアを占めています。キャンプやドライブ旅行などのアウトドアレクリエーション活動の増加により、先進的機能を搭載した自動車への需要が高まっています。消費者は自動車を購入する際に利便性と安全性を優先するため、スマートテールゲートは付加価値の高いものとなっています。これらのシステムは、トランクへのアクセスを容易にし、外出する個人のニーズに応えます。アウトドア志向のライフスタイルや長期のドライブ旅行へのシフトは、地域全体におけるスマートテールゲートシステムの普及を引き続き促進しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 原料サプライヤー

- 部品サプライヤー

- メーカー

- 流通チャネル

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- コスト分析

- 影響要因

- 促進要因

- 自動車の快適性機能の増加

- 消費者の利便性への期待の高まり

- 自動車の技術的進歩

- 自動車高級品セグメントの成長

- 産業の潜在的リスク・課題

- 高い製造コスト

- 技術的な複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:オファリング別、2021~2034年

- 主要動向

- 手動

- 電動

- ハンズフリー

第6章 市場推定・予測:車種別、2021~2034年

- 主要動向

- ハッチバック

- セダン

- SUV車

第7章 市場推定・予測:メカニズム別、2021~2034年

- 主要動向

- 電動

- 油圧

- 空気圧

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Aisin Seiki

- Aptiv

- Bosch

- Brose

- Continental

- Ficosa

- Hella

- Huf Holding

- Johnson

- Kiekert

- Lear

- Magna

- Mitsuba

- Stabilus

- Zhejiang

The Global Smart Tailgate Market, valued at USD 4.1 billion in 2024, is projected to grow at a CAGR of 8.5% from 2025 to 2034. This expansion is largely driven by the increasing demand for advanced in-vehicle automation and convenience features. Automotive manufacturers are continuously enhancing vehicle interfaces to incorporate innovative technologies. Smart tailgate systems with automated opening and closing functions offer hands-free access, making them particularly useful for users managing heavy loads. The emphasis on user-friendly, tech-forward solutions aligns with consumer preferences for greater convenience in modern vehicles.

Additionally, the rising popularity of larger vehicles, such as SUVs and crossovers, has significantly boosted the adoption of smart tailgates. Safety and security enhancements also propel market growth, as these systems reduce the risk of injury or damage by integrating sensors to detect obstacles. The ongoing evolution of vehicle safety features highlights the importance of these technologies in improving functionality and user satisfaction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 8.5% |

The market, segmented by offering into manual, powered, and hands-free options, saw the powered segment dominate with over 50% of the market share in 2024. By 2034, this segment is anticipated to surpass USD 4 billion, reflecting the growing consumer appetite for convenient, high-tech vehicle features. The integration of powered smart tailgates into vehicles demonstrates automakers' efforts to meet evolving expectations and enhance their competitive edge.

Mechanisms for smart tailgates include electrical, hydraulic, and pneumatic systems. Electrical systems held a 56% market share in 2024, driven by consumer demand for easily operable and energy-efficient solutions. These systems simplify tailgate control with features like button-operated opening and closing. The seamless, cordless operation improves efficiency and accessibility while aligning with the growing preference for smart, eco-friendly vehicles. The incorporation of advanced technologies like keyless entry and remote control further enhances user convenience and reinforces the appeal of electrical smart tailgate systems.

In North America, the United States dominated the regional smart tailgate market with an impressive 80% share in 2024. The rise in outdoor recreational activities, including camping and road trips, has led to increased demand for vehicles equipped with advanced features. Consumers prioritize convenience and safety when purchasing vehicles, making smart tailgates a valuable addition. These systems facilitate effortless access to the trunk, catering to the needs of individuals on the go. The shift towards outdoor-oriented lifestyles and longer road trips continues to drive the penetration of smart tailgate systems across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Distribution channel

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing vehicle comfort features

- 3.9.1.2 Rising consumer convenience expectations

- 3.9.1.3 Technological advancements in vehicles

- 3.9.1.4 Growing automotive luxury segment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing costs

- 3.9.2.2 Technical complexity

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Powered

- 5.4 Hands-Free

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUVs

Chapter 7 Market Estimates & Forecast, By Mechanism, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Electrical

- 7.3 Hydraulic

- 7.4 Pneumatic

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aisin Seiki

- 9.2 Aptiv

- 9.3 Bosch

- 9.4 Brose

- 9.5 Continental

- 9.6 Ficosa

- 9.7 Hella

- 9.8 Huf Holding

- 9.9 Johnson

- 9.10 Kiekert

- 9.11 Lear

- 9.12 Magna

- 9.13 Mitsuba

- 9.14 Stabilus

- 9.15 Zhejiang