|

市場調査レポート

商品コード

1665068

電気自動車熱管理システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Electric Vehicle Thermal Management System (EV TMS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電気自動車熱管理システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月11日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

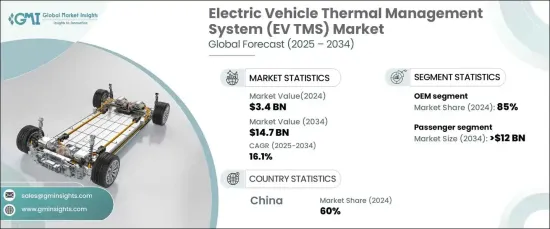

電気自動車熱管理システムの世界市場は、2024年には34億米ドルとなり、2025年から2034年までのCAGRは16.1%と、力強い成長が予測されています。

この市場拡大は、補助金、税制優遇措置、厳しい排出ガス規制などの政府政策により、電気自動車(EV)へのシフトが世界的に加速していることが背景にあります。EVは、温度変化に非常に敏感なバッテリーとパワーエレクトロニクスに大きく依存しているため、これらの重要部品の安全性を確保し、性能を最適化し、寿命を延ばすためには、高度な熱管理システムが不可欠です。

車種別では、市場は主に乗用車と商用車に分けられます。乗用車は2024年に市場の65%を占め、2034年までに120億米ドルを生み出すと予想されています。この優位性は、電気自動車に対する需要の高まりと、エネルギー効率、走行距離、車両性能全般の向上を重視する傾向が強まっていることに起因しています。路上で最も普及しているタイプのEVである乗用車は、熱管理ソリューションの技術的進歩の最前線にあり、バッテリーの寿命を延ばし、ドライバーと同乗者に優れた快適性を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 34億米ドル |

| 予測金額 | 147億米ドル |

| CAGR | 16.1% |

EV TMS市場は販売チャネル別にも区分され、OEM(相手先ブランド製造)分野が2024年に85%の大きなシェアを占める。OEMは、自動車生産時に最先端の熱管理技術を組み込む上で極めて重要な役割を果たしています。EVの普及が進む中、これらのメーカーは革新的で高性能、かつコスト効率の高い熱ソリューションを提供するため、研究開発に多額の投資を行っています。OEMとサプライヤーのコラボレーションは、規制基準への準拠、バッテリー効率の最適化、車両性能全体の向上により、この分野をさらに強化し、市場でのリーダーシップを確固たるものにしています。

中国のEV TMS市場は、2024年には60%という驚異的なシェアを占め、2034年には30億米ドルに達すると予測されています。この目覚ましい成長は、政府の支援政策とインセンティブに後押しされた、EV普及への積極的な推進力によるものです。EV生産と技術革新の世界的リーダーとして、中国は自動車メーカーやサプライヤーから多額の投資を誘致し続けており、研究開発の進展に拍車をかけ、EV革命の最前線における地位を確固たるものにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- EV TMSメーカー

- アフターマーケットクラッチプロバイダー

- ディストリビューター

- OEM

- エンドユーザー

- 利益率分析

- 価格分析

- コスト内訳

- テクノロジーとイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 電気自動車(EV)の普及拡大

- バッテリー技術の進歩

- エネルギー効率と航続距離への注目の高まり

- 政府のインセンティブと排出規制の強化

- 業界の潜在的リスク&課題

- 高度な熱管理システムの高コスト

- 小型軽量車両設計における統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- アクティブクーリング

- パッシブ冷却

- ハイブリッド冷却

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ヒートポンプ

- 電動ポンプ

- ファン

- 熱電モジュール

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- BorgWarner

- Bosch

- Calsonic Kansei

- Continental

- Dana

- Delphi Technologies

- Denso

- Gentherm

- Grayson Thermal Systems

- Hanon Systems

- LG Chem

- MAHLE

- Modine Manufacturing Company

- Renesas Electronics

- Sanden Holdings

- Schaeffler Group

- Tesla

- Thermo King

- Valeo

- Visteon

The Global Electric Vehicle Thermal Management System Market, valued at USD 3.4 billion in 2024, is projected to experience robust growth, with a CAGR of 16.1% from 2025 to 2034. This expansion is fueled by the accelerating global shift toward electric vehicles (EVs), driven by government policies such as subsidies, tax incentives, and stringent emissions regulations. As EVs rely heavily on batteries and power electronics, which are highly sensitive to temperature fluctuations, advanced thermal management systems are essential to ensure safety, optimize performance, and extend the lifespan of these critical components.

In terms of vehicle categories, the market is primarily divided into passenger vehicles and commercial vehicles. Passenger vehicles held a dominant 65% share of the market in 2024 and are expected to generate USD 12 billion by 2034. This dominance is attributed to the growing demand for electric cars and the increasing emphasis on improving energy efficiency, driving range, and overall vehicle performance. As the most prevalent type of EVs on the road, passenger vehicles are at the forefront of technological advancements in thermal management solutions, which enhance battery longevity and provide superior comfort for drivers and passengers alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $14.7 Billion |

| CAGR | 16.1% |

The EV TMS market is also segmented by sales channels, with the original equipment manufacturer (OEM) segment capturing a significant 85% share in 2024. OEMs play a pivotal role in integrating cutting-edge thermal management technologies during vehicle production. With rising EV adoption, these manufacturers are channeling substantial investments into research and development to deliver innovative, high-performance, and cost-efficient thermal solutions. Collaborations between OEMs and suppliers are further strengthening this segment by ensuring compliance with regulatory standards, optimizing battery efficiency, and improving overall vehicle performance, solidifying their leadership in the market.

China's EV TMS market accounted for an impressive 60% share in 2024 and is anticipated to reach USD 3 billion by 2034. This remarkable growth is driven by the nation's aggressive push for EV adoption, bolstered by supportive government policies and incentives. As a global leader in EV production and innovation, China continues to attract significant investments from automakers and suppliers, fueling advancements in research and development and cementing its position at the forefront of the EV revolution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 EV TMS manufacturers

- 3.2.2 Aftermarket clutch providers

- 3.2.3 Distributors

- 3.2.4 OEMs

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of electric vehicles (EVs)

- 3.9.1.2 Advancements in battery technologies

- 3.9.1.3 Rising focus on energy efficiency and vehicle range

- 3.9.1.4 Government incentives and stricter emission regulations

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost of advanced thermal management systems

- 3.9.2.2 Integration complexities in compact and lightweight vehicle designs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active cooling

- 5.3 Passive cooling

- 5.4 Hybrid cooling

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Heat pumps

- 6.3 Electric pumps

- 6.4 Fans

- 6.5 Thermoelectric modules

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery Electric Vehicles (BEV)

- 8.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 8.4 Hybrid Electric Vehicles (HEV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn,Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BorgWarner

- 11.2 Bosch

- 11.3 Calsonic Kansei

- 11.4 Continental

- 11.5 Dana

- 11.6 Delphi Technologies

- 11.7 Denso

- 11.8 Gentherm

- 11.9 Grayson Thermal Systems

- 11.10 Hanon Systems

- 11.11 LG Chem

- 11.12 MAHLE

- 11.13 Modine Manufacturing Company

- 11.14 Renesas Electronics

- 11.15 Sanden Holdings

- 11.16 Schaeffler Group

- 11.17 Tesla

- 11.18 Thermo King

- 11.19 Valeo

- 11.20 Visteon