|

市場調査レポート

商品コード

1698236

バッテリー熱管理システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Battery Thermal Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| バッテリー熱管理システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月04日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

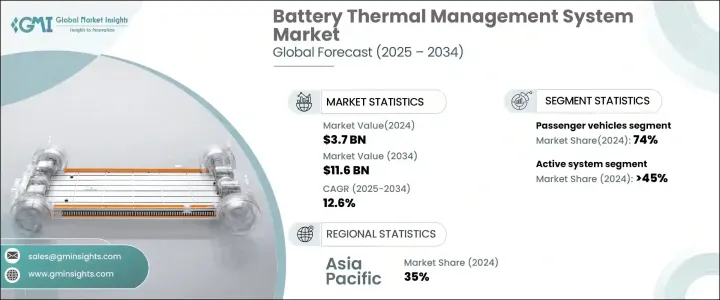

バッテリー熱管理システムの世界市場規模は37億米ドルで、電気自動車(EV)の生産台数の増加やバッテリー技術の進歩に牽引され、2025年から2034年にかけてCAGR 12.6%で拡大すると予測されています。

高性能かつ長寿命のバッテリーへの需要が高まり続ける中、メーカーはバッテリーの効率、安全性、長寿命を確保する革新的な熱管理ソリューションに注力しています。

EVへのシフトが勢いを増す中、バッテリー熱管理システムはバッテリー性能を最適化する上で重要なコンポーネントとなっています。これらのシステムは、温度を調整し、過熱を防ぎ、バッテリー寿命を延ばし、エネルギー効率、充電速度、安全性といった主要な懸念事項に対処します。バッテリーの安全性に関する政府の厳しい規制と急速充電技術の採用増加が、市場の成長をさらに促進しています。さらに、EV充電インフラの拡大とバッテリー冷却技術の継続的な研究開発(R&D)は、業界プレーヤーに有利な機会を生み出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 116億米ドル |

| CAGR | 12.6% |

市場は、アクティブシステム、パッシブシステム、ハイブリッドシステムなど、熱管理システムのタイプによって区分されます。2024年には、主にバッテリーパック内の温度を効果的に調整する能力により、アクティブシステムセグメントが45%の圧倒的な市場シェアを占める。アクティブ・システムは、最適な温度条件を維持するために液体または空冷機構を使用するため、高性能バッテリーに適しています。一方、自然冷却方式に依存するパッシブ・システムは、バッテリーの安全性と効率を高める上でアクティブ・システムを補完するため、2034年までCAGR 14%で成長すると予測されています。また、アクティブ冷却機構とパッシブ冷却機構の両方を統合したハイブリッド・システムも、優れた温度調整機能を備えていることから、人気を集めています。

車種別では、バッテリー熱管理システム市場は乗用車と商用車に分類されます。2024年には、EVの普及と効率的なバッテリー冷却ソリューションのニーズが高まり、乗用車が74%という大きな市場シェアを占める。航続距離の延長と充電時間の短縮が好まれるようになり、乗用車には高度な熱管理システムが不可欠となっています。しかし、商用車はより速い成長率が見込まれており、2034年までのCAGRは13%と予測されています。電気トラック、バス、配達用バンの需要の高まりと、持続可能な輸送を推進する政府の取り組みが、この分野での熱管理ソリューションの採用を後押ししています。

アジア太平洋地域はバッテリー熱管理システム市場の主要プレーヤーとして台頭し、2024年には35%のシェアを占める。中国がこの地域をリードし、熱管理ソリューションの生産と消費の両方を牽引しています。中国、台湾、インドには確立されたサプライチェーンと大手バッテリーメーカーが存在し、市場拡大を後押ししています。EVの急速な普及は、都市化や政府の支援政策と相まって、同地域のバッテリー熱管理システムの需要をさらに加速させています。業界各社は、競争情勢における市場ポジションを強化するため、技術的進歩、戦略的パートナーシップ、製造拡大に注力しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料プロバイダー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 最終顧客

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 使用事例

- 影響要因

- 促進要因

- 電気自動車(EV)需要の高まり

- バッテリー技術の進歩

- 急速充電ステーションの普及拡大

- EVインフラへの投資の増加

- 業界の潜在的リスク&課題

- 初期コストの高さ

- 統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:オファリング別、2021年~2034年

- 主要動向

- アクティブシステム

- パッシブシステム

- ハイブリッドシステム

第6章 市場推計・予測:バッテリー別、2021年~2034年

- 主要動向

- リチウムイオン電池

- ニッケル水素電池

- 鉛蓄電池

- 固体電池

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 小型商用車

- 商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド車(HEV)

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aptiv PLC

- BASF

- Bosch

- Continental

- Dana Limited

- Gentherm

- Hanon Systems

- Hitachi

- Infineon

- Johnson Control

- MAHLE GmbH

- Marelli

- Modine

- Modine Manufacturing

- Sanden Corporation

- Schaeffler

- Valeo

- Vitesco Technologies

- VOSS Automotive

- ZF Friedrichshafen

The Global Battery Thermal Management System Market was valued at USD 3.7 billion and is projected to expand at a CAGR of 12.6% between 2025 and 2034, driven by the rising production of electric vehicles (EVs) and advancements in battery technologies. As the demand for high-performance and long-lasting batteries continues to rise, manufacturers are focusing on innovative thermal management solutions that ensure battery efficiency, safety, and longevity.

With the shift towards EVs gaining momentum, battery thermal management systems have become a critical component in optimizing battery performance. These systems regulate temperature, prevent overheating, and enhance battery lifespan, addressing key concerns such as energy efficiency, charging speed, and safety. Stringent government regulations on battery safety and the increasing adoption of fast-charging technology are further fueling market growth. Additionally, the expansion of EV charging infrastructure and continuous research and development (R&D) in battery cooling technologies are creating lucrative opportunities for industry players.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 12.6% |

The market is segmented by the type of thermal management system, including active, passive, and hybrid systems. In 2024, the active system segment held a dominant 45% market share, primarily due to its ability to regulate temperature effectively within the battery pack. Active systems use liquid or air cooling mechanisms to maintain optimal thermal conditions, making them a preferred choice for high-performance batteries. Meanwhile, passive systems, which rely on natural cooling methods, are projected to grow at a CAGR of 14% through 2034 as they complement active systems in enhancing battery safety and efficiency. Hybrid systems, which integrate both active and passive cooling mechanisms, are also gaining traction due to their ability to provide superior temperature regulation.

By vehicle type, the battery thermal management system market is categorized into passenger vehicles and commercial vehicles. In 2024, passenger vehicles accounted for a substantial 74% market share, driven by the increasing adoption of EVs and the need for efficient battery cooling solutions. The growing preference for longer driving ranges and faster charging times has made advanced thermal management systems indispensable for passenger vehicles. However, commercial vehicles are expected to witness a faster growth rate, with a projected CAGR of 13% through 2034. The rising demand for electric trucks, buses, and delivery vans, along with government initiatives promoting sustainable transportation, is propelling the adoption of thermal management solutions in this segment.

Asia Pacific emerged as a key player in the battery thermal management system market, holding a 35% share in 2024. China leads the region, driving both production and consumption of thermal management solutions. The presence of well-established supply chains and major battery manufacturers in China, Taiwan, and India is boosting market expansion. The rapid increase in EV adoption, coupled with urbanization and supportive government policies, is further accelerating demand for battery thermal management systems in the region. Industry players are focusing on technological advancements, strategic partnerships, and manufacturing expansion to strengthen their market position in the competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Use cases

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for electric vehicles (EVs)

- 3.9.1.2 Advancements in battery technology

- 3.9.1.3 Increasing adoption of fast-charging stations

- 3.9.1.4 Growing investment in EV infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs

- 3.9.2.2 Complexity in integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active system

- 5.3 Passive system

- 5.4 Hybrid system

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion battery

- 6.3 Nickel-Metal Hydride (NiMH) battery

- 6.4 Lead-acid battery

- 6.5 Solid-state battery

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles Light

- 7.3.1 Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery Electric Vehicles (BEVs)

- 8.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 8.4 Hybrid Electric Vehicles (HEVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv PLC

- 10.2 BASF

- 10.3 Bosch

- 10.4 Continental

- 10.5 Dana Limited

- 10.6 Gentherm

- 10.7 Hanon Systems

- 10.8 Hitachi

- 10.9 Infineon

- 10.10 Johnson Control

- 10.11 MAHLE GmbH

- 10.12 Marelli

- 10.13 Modine

- 10.14 Modine Manufacturing

- 10.15 Sanden Corporation

- 10.16 Schaeffler

- 10.17 Valeo

- 10.18 Vitesco Technologies

- 10.19 VOSS Automotive

- 10.20 ZF Friedrichshafen