|

市場調査レポート

商品コード

1664877

冷凍システムの市場機会、成長促進要因、産業動向分析、2024年~2032年予測Refrigeration System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

カスタマイズ可能

|

|||||||

| 冷凍システムの市場機会、成長促進要因、産業動向分析、2024年~2032年予測 |

|

出版日: 2024年12月04日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

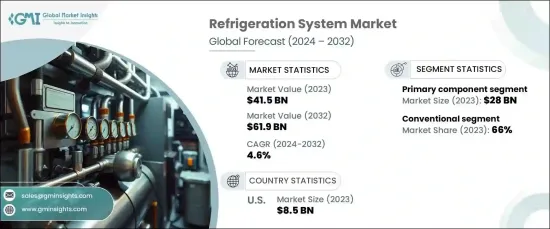

世界の冷凍システム市場は、2023年に415億米ドルとなり、2024年から2032年にかけて4.6%の安定したCAGRで成長すると予測されています。

この成長の原動力となっているのは、食品・飲料、医薬品、化学など、信頼性の高い冷凍が製品保存や規制遵守に重要な役割を果たす主要産業における需要の増加です。最先端技術の進歩とエネルギー効率の高い冷凍ソリューションへのシフトが、市場をさらに前進させています。

冷凍システム市場は一次部品と補助部品に区分されます。2023年、一次部品セグメントは280億米ドルを占め、2032年までCAGR 4.7%で成長すると予測されています。このセグメントの主導的地位は、効率的な冷凍サイクルを確保する上でコンプレッサー、蒸発器、凝縮器が不可欠な役割を果たすことに起因しています。あらゆる冷凍システムの心臓部であるコンプレッサーは、エネルギー消費の大半を占めており、性能向上とエネルギーコスト削減のための継続的な技術革新に拍車をかけています。一方、エバポレーターとコンデンサーは熱伝達において極めて重要な役割を果たしており、一貫した温度制御と信頼性の高いシステム性能を保証しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024年~2032年 |

| 開始金額 | 415億米ドル |

| 予測金額 | 619億米ドル |

| CAGR | 4.6% |

冷蔵タイプに基づき、市場は従来型システムとスマートシステムに分類されます。従来型冷凍システムは2023年に66%の市場シェアを占め、2032年には404億米ドルに達すると予測されます。普及の原動力は、手頃な価格と低いメンテナンス要件であり、特にコストに敏感な市場において、中小企業にとって好ましい選択肢となっています。その他の特典として、従来型システムには確立されたサプライチェーンと技術的専門知識があるため、シームレスな導入が可能です。技術インフラが未発達な地域では、スマート冷凍技術がまだ広く普及していない可能性のある高度なフレームワークを必要とするため、これらのシステムに大きく依存することが多いです。

北米の冷凍システム市場は米国がリードしており、2023年の評価額は85億米ドルで、2032年までのCAGRは4.6%と予想されています。米国市場の優位性は、製品の品質と厳しい規制への対応のために冷蔵を優先する強力な産業・商業部門に支えられています。同国の確立されたコールドチェーン網、厳格な食品安全基準、医薬品保管は、さらなる成長促進要因です。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 高まる環境規制と持続可能性への取り組み

- 技術の進歩と低GWP冷媒へのシフトの増加

- コールドチェーン物流に対する需要の高まり

- 業界の潜在的リスク・課題

- 高い初期投資と運用コスト

- 技術的ハードルと安全性への配慮

- 成長促進要因

- 技術概要

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2032年

- 主要動向

- 主要コンポーネント

- コンプレッサー

- レシプロコンプレッサー

- スクリューコンプレッサー

- 遠心圧縮機

- スクロールコンプレッサー

- コンデンサー

- 空冷コンデンサー

- 水冷式コンデンサー

- 蒸発式コンデンサー

- 蒸発器

- プレート式蒸発器

- チューブ式蒸発器

- フィン付き蒸発器

- 制御システム

- コンプレッサー

- 補助コンポーネント

- ソレノイドバルブ

- 圧力調整器

- 高圧レギュレーター

- 低圧レギュレーター

- フィルター

- 熱交換器

- プレート式熱交換器

- シェル&チューブ式熱交換器

- フィン付き熱交換器

- 膨張弁

- その他

第6章 市場推計・予測:冷凍カテゴリー別、2021年~2032年

- 主要動向

- スマート

- 従来型

第7章 市場推計・予測:用途別、2021年~2032年

- 主要動向

- 商業

- ハイパーマーケット・スーパーマーケット/食品小売業

- ホスピタリティ

- ヘルスケア施設

- その他(娯楽・レジャー、花卉など)

- 産業

- 食品・飲料加工

- 化学・石油化学

- 製薬

- 電子・その他製造業

- 冷蔵倉庫

- エネルギー・公益事業

- その他(冶金、半導体など)

- 運輸

- トラック冷凍

- コンテナ輸送

- 海上船舶

- その他(航空宇宙システム、鉄道輸送など)

第8章 市場推計・予測:ユーザー別、2021年~2032年

- 主要動向

- OEM

- 建設業者

- 流通業者

第9章 市場推計・予測:流通チャネル別、2021年~2032年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ポーランド

- ポルトガル

- ロシア

- デンマーク

- スウェーデン

- ハンガリー

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- インドネシア

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ

第11章 企業プロファイル

- BITZER Kühlmaschinenbau GmbH

- Carrier Global Corporation

- Daikin Industries Ltd.

- Danfoss A/S

- Dorin

- Embraco(Nidec Corporation)

- Emerson Electric Co.

- Frick India Limited

- GEA

- Grundfos

- Hitachi

- Hussmann Corporation

- Ingersoll-Rand, Plc.

- Johnson Controls

- Lennox International

- Tecumseh Products Company

The Global Refrigeration System Market was valued at USD 41.5 billion in 2023 and is projected to grow at a steady CAGR of 4.6% from 2024 to 2032. This growth is fueled by increasing demand across key industries such as food and beverage, pharmaceuticals, and chemicals, where reliable refrigeration plays a critical role in product preservation and regulatory compliance. Advancements in cutting-edge technologies and the shift toward energy-efficient refrigeration solutions are further driving the market forward.

The refrigeration system market is segmented into primary and auxiliary components. In 2023, the primary component segment accounted for USD 28 billion and is forecasted to grow at a CAGR of 4.7% through 2032. This segment's leading position is attributed to the indispensable roles of compressors, evaporators, and condensers in ensuring efficient refrigeration cycles. Compressors, the heart of any refrigeration system, dominate energy consumption, spurring ongoing innovations to boost performance and reduce energy costs. Meanwhile, evaporators and condensers play a pivotal role in heat transfer, ensuring consistent temperature control and reliable system performance.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $41.5 Billion |

| Forecast Value | $61.9 Billion |

| CAGR | 4.6% |

Based on refrigeration type, the market is categorized into conventional and smart systems. Conventional refrigeration systems held a 66% market share in 2023 and are projected to reach USD 40.4 billion by 2032. Their widespread adoption is driven by affordability and low maintenance requirements, making them a preferred option for small and medium-sized enterprises, especially in cost-sensitive markets. Additionally, conventional systems benefit from established supply chains and technical expertise, enabling seamless implementation. Regions with underdeveloped technological infrastructure often rely heavily on these systems, as smart refrigeration technologies require advanced frameworks that may not yet be widely accessible.

The United States leads the refrigeration system market in North America, with a valuation of USD 8.5 billion in 2023 and an anticipated CAGR of 4.6% through 2032. The dominance of the U.S. market is underpinned by its strong industrial and commercial sectors, which prioritize refrigeration for product quality and compliance with stringent regulations. The country's well-established cold chain network, strict food safety standards, and pharmaceutical storage are additional growth drivers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing environmental regulations and sustainability initiatives

- 3.6.1.2 Technological progress and increasing shift towards low-GWP refrigerants

- 3.6.1.3 Rising demand for cold chain logistics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment and operational costs

- 3.6.2.2 Technical hurdles and safety considerations

- 3.6.1 Growth drivers

- 3.7 Technological overview

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2032 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Primary component

- 5.2.1 Compressors

- 5.2.1.1 Reciprocating compressors

- 5.2.1.2 Screw compressors

- 5.2.1.3 Centrifugal compressors

- 5.2.1.4 Scroll compressors

- 5.2.2 Condensers

- 5.2.2.1 Air-cooled condensers

- 5.2.2.2 Water-cooled condensers

- 5.2.2.3 Evaporative condensers

- 5.2.3 Evaporators

- 5.2.3.1 Plate evaporators

- 5.2.3.2 Tube evaporators

- 5.2.3.3 Finned evaporators

- 5.2.4 Control systems

- 5.2.1 Compressors

- 5.3 Auxiliary components

- 5.3.1 Solenoid valves

- 5.3.2 Pressure regulators

- 5.3.2.1 High-pressure regulators

- 5.3.2.2 Low-pressure regulators

- 5.3.3 Filters

- 5.3.4 Heat exchangers

- 5.3.4.1 Plate heat exchangers

- 5.3.4.2 Shell and tube heat exchangers

- 5.3.4.3 Finned heat exchangers

- 5.3.5 Expansion valves

- 5.3.6 Others

Chapter 6 Market Estimates & Forecast, By Refrigeration Category, 2021-2032 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Smart

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Application, 2021-2032 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Commercial

- 7.2.1 Hypermarket & supermarket /food retailers

- 7.2.2 Hospitality

- 7.2.3 Healthcare facilities

- 7.2.4 Others (entertainment & leisure, floral, etc.)

- 7.3 Industrial

- 7.3.1 Food & beverage processing

- 7.3.2 Chemical & petrochemical

- 7.3.3 Pharmaceutical

- 7.3.4 Electronics& other manufacturing

- 7.3.5 Cold storage warehouses

- 7.3.6 Energy & utility

- 7.3.7 Others (metallurgy, semiconductor, etc.)

- 7.4 Transportation

- 7.4.1 Truck refrigeration

- 7.4.2 Container shipping

- 7.4.3 Maritime vessels

- 7.4.4 Others (aerospace system, rail transport, etc.)

Chapter 8 Market Estimates & Forecast, By User, 2021-2032 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Constructer

- 8.4 Distributors

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2032 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021-2032 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 United Kingdom

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Poland

- 10.3.8 Portugal

- 10.3.9 Russia

- 10.3.10 Denmark

- 10.3.11 Sweden

- 10.3.12 Hungary

- 10.3.13 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Rest of APAC

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 BITZER Kühlmaschinenbau GmbH

- 11.2 Carrier Global Corporation

- 11.3 Daikin Industries Ltd.

- 11.4 Danfoss A/S

- 11.5 Dorin

- 11.6 Embraco (Nidec Corporation)

- 11.7 Emerson Electric Co.

- 11.8 Frick India Limited

- 11.9 GEA

- 11.10 Grundfos

- 11.11 Hitachi

- 11.12 Hussmann Corporation

- 11.13 Ingersoll-Rand, Plc.

- 11.14 Johnson Controls

- 11.15 Lennox International

- 11.16 Tecumseh Products Company