|

市場調査レポート

商品コード

1664845

冷凍食品加工機械の市場機会、成長促進要因、産業動向分析、2024年~2032年予測Frozen Food Processing Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

カスタマイズ可能

|

|||||||

| 冷凍食品加工機械の市場機会、成長促進要因、産業動向分析、2024年~2032年予測 |

|

出版日: 2024年12月02日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

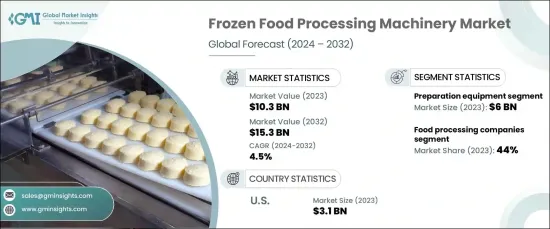

世界の冷凍食品加工機械市場は、2023年に103億米ドルとなり、2024年から2032年にかけて4.5%のCAGRで堅調に成長すると予測されています。

この成長を牽引しているのは、自動化、人工知能(AI)、機械学習の進歩であり、これらは効率を高めコストを削減することで食品加工機械に革命をもたらしています。急速冷凍や極低温法などの冷凍技術の革新は、食感や栄養素を保持することによって食品の品質を維持する上で極めて重要な役割を果たしています。これは、冷凍果物、野菜、魚介類の需要増に対応する上で極めて重要です。

クイック・サービス・レストラン(QSR)の拡大とオンライン・フード・デリバリー部門の活況が、冷凍食品業界の成長に拍車をかけています。これらの部門は冷凍製品に大きく依存しており、高い需要を満たすための高度な加工機械の必要性に拍車をかけています。さらに、スーパーマーケットとハイパーマーケットの世界の普及は、小売部門の冷凍食品への依存を加速させています。小売業者は、進化する消費者の選好に対応し、製品の品質を確保するため、最先端の設備への投資をますます増やしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024年~2032年 |

| 開始金額 | 103億米ドル |

| 予測金額 | 153億米ドル |

| CAGR | 4.5% |

著しい進歩にもかかわらず、特に新興市場の小規模メーカーは、顕著な障害に直面しています。近代的な設備にかかる高額な初期費用と予算の制約が相まって、最先端の機械へのアクセスが制限されることが多いです。サプライチェーンの混乱は、重要な部品や包装資材の入手をさらに複雑にし、生産の遅れにつながります。このような課題は、このダイナミックな市場で競争しようと努力する中小企業にとって、大きな障壁となります。

機械のタイプ別では、2023年に調製機器が市場を独占し、60億米ドルの収益を上げました。この分野は、2024年から2032年まで約4.7%のCAGRで安定的に成長すると予測されています。調理機器は、スライス、切断、混合、粉砕用のツールで構成され、冷凍食品製造において重要な役割を果たします。これらの機器は、製品の品質を維持し、冷凍工程を最適化するために不可欠な、サイズと形状の一貫性を確保します。

2023年の市場シェアは食品加工会社が約44%を占めており、この動向は2032年まで同様の成長軌道を描くと予想されます。賞味期限が延長されたコンビニエンスフードの需要の高まりが、こうした企業の増産につながっています。その結果、高性能機械への投資が急増し、企業は高まる消費者の期待に応えることができるようになりました。

米国は依然として冷凍食品加工機械市場の支配的プレーヤーであり、2023年の市場規模は31億米ドルでした。同市場は、冷凍技術の絶え間ない技術革新によって、2024年から2032年にかけてCAGR4.9%で拡大すると予測されています。これらの進歩は生産効率を高め、製品品質を向上させ、米国食品加工業界の高まるニーズを支えています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 冷凍食品需要の高まり

- 技術の進歩

- 業界の潜在的リスク・課題

- 高い設備投資

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:機械タイプ別、2021年~2032年

- 主要動向

- プレパレーション機器

- カッター

- ブレンダー

- スライサー

- グラインダー

- その他(ピーラーなど)

- 冷凍機器

- ブラストフリーザー

- スパイラルフリーザー

- プレートフリーザー

- 個別急速凍結(IQF)装置

- その他(トンネルフリーザーなど)

- 包装機器

- 包装機

- 袋詰機

- カートニングマシン

- その他(真空包装機など)

- その他(保管機器、コンベアなど)

第6章 市場推計・予測:技術別、2021年~2032年

- 主要動向

- 機械式冷凍

- 低温冷凍

第7章 市場推計・予測:操作モード別、2021年~2032年

- 主要動向

- 半自動

- 自動

第8章 市場推計・予測:用途別、2021年~2032年

- 主要動向

- 果物・野菜

- 乳製品

- 肉、鶏肉、魚介類

- 調理済み食品(RTE)

- ベーカリー製品

- スナック菓子

- その他(スープ、ソースなど)

第9章 市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 食品加工企業

- 外食・フードサービス

- 小売・スーパーマーケット

- その他(物流センターなど)

第10章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Air Products and Chemicals, Inc.

- Alfa Laval AB

- Bühler Group

- GEA Group AG

- Griffith Foods Inc.

- Hoshizaki Corporation

- Intralox

- JBT Corporation

- Marel

- OctoFrost Group

- SPX FLOW, Inc.

- Starfrost(UK)Ltd.

- Tetra Pak International S.A.

- The Middleby Corporation

The Global Frozen Food Processing Machinery Market was valued at USD 10.3 billion in 2023 and is projected to grow at a robust CAGR of 4.5% from 2024 to 2032. Driving this growth are advancements in automation, artificial intelligence (AI), and machine learning, which are revolutionizing food processing machinery by enhancing efficiency and cutting costs. Innovations in freezing technologies, such as quick freezing and cryogenic methods, are playing a pivotal role in maintaining food quality by preserving texture and nutrients. This is crucial for meeting the rising demand for frozen fruits, vegetables, and seafood.

The expansion of quick-service restaurants (QSRs) and the booming online food delivery sector are fueling the frozen food industry's growth. These sectors rely heavily on frozen products, spurring the need for advanced processing machinery to meet high demand. Additionally, the global proliferation of supermarkets and hypermarkets is accelerating the retail sector's reliance on frozen foods. Retailers are increasingly investing in state-of-the-art equipment to cater to evolving consumer preferences and ensure product quality.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $10.3 Billion |

| Forecast Value | $15.3 Billion |

| CAGR | 4.5% |

Despite significant advancements, smaller manufacturers, especially in emerging markets, face notable obstacles. High upfront costs for modern equipment, coupled with budget constraints, often limit their access to cutting-edge machinery. Supply chain disruptions further complicate the availability of critical components and packaging materials, leading to production delays. These challenges pose substantial barriers for smaller players striving to compete in this dynamic market.

In terms of machinery type, preparation equipment dominated the market in 2023, generating USD 6 billion in revenue. This segment is anticipated to grow at a steady CAGR of approximately 4.7% from 2024 to 2032. Preparation equipment-comprising tools for slicing, cutting, blending, and grinding-plays a critical role in frozen food production. These machines ensure consistency in size and shape, which is essential for maintaining product quality and optimizing freezing processes.

Food processing companies accounted for approximately 44% of the market share in 2023, and this trend is expected to continue with a similar growth trajectory through 2032. The rising demand for convenience foods with extended shelf lives has led to increased production among these companies. Consequently, investments in high-performance machinery have surged, enabling companies to meet growing consumer expectations.

The United States remains a dominant player in the frozen food processing machinery market, valued at USD 3.1 billion in 2023. The market is forecasted to expand at a CAGR of 4.9% from 2024 to 2032, driven by continuous innovation in freezing technologies. These advancements are enhancing production efficiency, improving product quality, and supporting the growing needs of the US food processing industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for frozen foods

- 3.6.1.2 Technological advancements

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital investment

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Machinery Type, 2021-2032 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Preparation equipment

- 5.2.1 Cutters

- 5.2.2 Blenders

- 5.2.3 Slicers

- 5.2.4 Grinders

- 5.2.5 Others (Peelers, Etc)

- 5.3 Freezing Equipment

- 5.3.1 Blast freezers

- 5.3.2 Spiral freezers

- 5.3.3 Plate freezers

- 5.3.4 Individual Quick Freezing (IQF) Equipment

- 5.3.5 Others (Tunnel Freezers, Etc)

- 5.4 Packaging equipment

- 5.4.1 Wrapping machines

- 5.4.2 Bagging machines

- 5.4.3 Cartoning machines

- 5.4.4 Others (Vacuum Packaging Machines, Etc)

- 5.5 Others (Storage Equipment, Conveyors, Etc)

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2032 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Mechanical freezing

- 6.3 Cryogenic freezing

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2021-2032 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Semi-Automatic

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Application, 2021-2032 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Fruits & vegetables

- 8.3 Dairy products

- 8.4 Meat, poultry, & seafood

- 8.5 Ready-to-Eat (RTE) meals

- 8.6 Bakery products

- 8.7 Snacks

- 8.8 Others (Soups, Sauces, Etc)

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2032 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Food processing companies

- 9.3 Restaurants and foodservice

- 9.4 Retail & supermarkets

- 9.5 Others (Distribution Centers, Etc)

Chapter 10 Market Estimates & Forecast, By Region, 2021-2032 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Air Products and Chemicals, Inc.

- 11.2 Alfa Laval AB

- 11.3 Bühler Group

- 11.4 GEA Group AG

- 11.5 Griffith Foods Inc.

- 11.6 Hoshizaki Corporation

- 11.7 Intralox

- 11.8 JBT Corporation

- 11.9 Marel

- 11.10 OctoFrost Group

- 11.11 SPX FLOW, Inc.

- 11.12 Starfrost (UK) Ltd.

- 11.13 Tetra Pak International S.A.

- 11.14 The Middleby Corporation