|

市場調査レポート

商品コード

1833622

半導体チューブおよび継手の市場機会と促進要因、産業動向分析、2025年~2034年予測Semiconductor Tubing and Fittings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 半導体チューブおよび継手の市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月01日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

概要

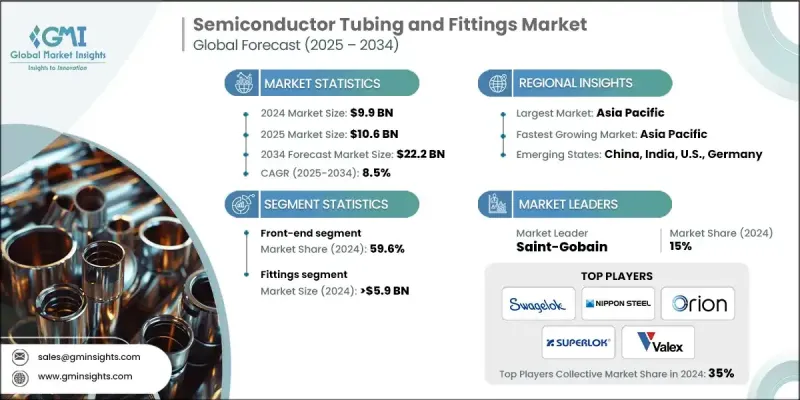

Global Market Insights Inc.が発行した最新レポートによると、世界の半導体チューブおよび継手市場は2024年に99億米ドルと推定され、CAGR 8.5%で2025年の106億米ドルから2034年には222億米ドルに成長すると予測されています。

半導体プロセスでは、安全かつクリーンに輸送しなければならない攻撃的な化学薬品や特殊ガスが使用されます。このため、PFA、PTFE、PVDF製など、耐薬品性に優れた高純度チューブや継手の需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 99億米ドル |

| 予測金額 | 222億米ドル |

| CAGR | 8.5% |

フロントエンド半導体の採用増加

2024年には、純度と精度が譲れないウエハー製造プロセスによって、フロントエンド分野が大きなシェアを占めています。この段階では、プロセスの完全性を維持するために超清浄チューブと耐腐食性継手を必要とする複雑な薬液供給システムが含まれます。工場が極端な汚染管理基準の下で操業しているため、特にチップメーカーがより小さなノードとより複雑なアーキテクチャに移行するにつれて、前工程の流体処理コンポーネントに対する需要は急増し続けています。

継手の牽引力

わずかな漏れや材料の劣化でさえ半導体製造プロセス全体を危険にさらす可能性があるため、継手セグメントは2024年に大きな収益を上げました。継手は、侵食性の化学薬品に耐え、さまざまな圧力下でも漏れのない接続を維持し、長期にわたって安定した状態を保つことが期待されています。同市場では、高純度金属とエンジニアリング・プラスチックで作られた、精密設計された溶接可能なクイック・コネクト・フィッティングへの好みが高まっています。

アジア太平洋地域が有利な地域として浮上する

アジア太平洋半導体チューブおよび継手市場は2024年に大きなシェアを占める。台湾、韓国、中国、日本などの国々には、高純度の流体処理システムを必要とする大手鋳造メーカーや集積デバイスメーカー(IDM)があります。政府の支援によるチップ製造への投資や、地元およびグローバル企業による積極的な生産能力拡大が、超清浄チューブおよび継手の必要性に拍車をかけています。市場成長の原動力となっているのは、ウエハー生産量の増加、新工場の建設、OEMと部品サプライヤーの戦略的提携です。

半導体チューブおよび継手市場の主要企業は、Rensa Tubes、Swagelok、Advance Fittings Corp、FITOK Group Co Ltd、イハラサイエンス株式会社、Valex Corp、Orion、FUJIKIN、Masterflex Group、Superlok、Dibert Valve &Fitting Co Inc、Saint-Gobain、APT、Nippon Steel Corp、Heraeus Covanticsです。

半導体チューブおよび継手市場における足場を固めるため、企業はイノベーション、パートナーシップ、地域拡大戦略を組み合わせて採用しています。大手企業は、耐薬品性、温度安定性、パーティクル発生ゼロを強化した次世代材料を開発するため、研究開発に多額の投資を行っています。また、リードタイムを短縮し、サービス対応力を向上させるため、主要顧客拠点の近くにクリーンルーム製造施設を建設または拡張している企業も多いです。半導体OEMや製造装置メーカーとの戦略的提携により、チューブや継手のサプライヤーは、システムレベルの設計によりシームレスに統合できるようになりました。さらに、製品ポートフォリオを多様化し、特に半導体投資が急増しているアジアや北米を中心とした新たな地域市場に参入するため、企業は合併や買収を進めています。こうした積極的な戦略は、高度な技術と品質に敏感な市場での差別化に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 半導体産業の成長

- 技術的進歩

- 研究開発活動の増加

- 業界の潜在的リスク&課題

- 特殊材料の高コスト

- 製造と品質管理の複雑さ

- 機会

- 先端材料の開発

- カスタマイズとモジュール式ソリューション

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- チューブ

- 金属管

- フッ素ポリマーチューブ

- 石英管

- 複合チューブ

- 特殊ポリマーチューブ

- 継手

- 圧縮継手

- フレア継手

- フェイスシール継手

- 溶接継手

- 超高純度(UHP)継手

- クイックコネクトフィッティング

- ねじ込み継手

- その他

第6章 市場推計・予測:工程別、2021-2034

- 主要動向

- フロントエンド

- バックエンド

第7章 市場推計・予測:機器種別、2021-2034

- 主要動向

- 半導体設計

- マスク/レチクル製造

- ウエハー製造・加工

- 表面調整

- 組み立てと梱包

- テスト/検査

- 製造施設

- 熱処理

- 証言録取

- その他

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Advance Fittings Corp

- APT

- Dibert Valve &Fitting Co Inc

- FITOK Group Co Ltd

- FUJIKIN

- Heraeus Covantics

- Ihara Science Corporation

- Masterflex Group

- Nippon Steel Corp

- Orion

- Rensa Tubes

- Saint-Gobain

- Superlok

- Swagelok

- Valex Corp