半導体材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Semiconductor Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851742

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

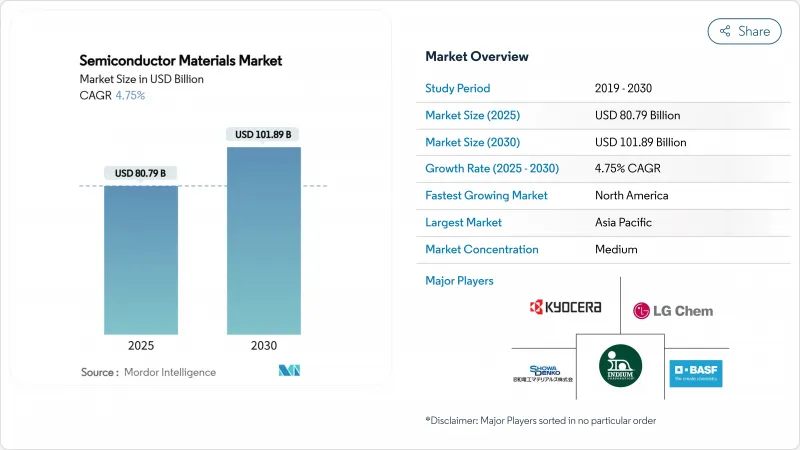

半導体材料の市場規模は2025年に807億9,000万米ドルに達し、2030年には1,018億9,000万米ドルに拡大し、予測期間中にCAGR 4.75%で進展すると予測されています。

AIに最適化されたアーキテクチャの継続と自動車の電動化により、従来のシリコンは基礎物理学の限界に近づきつつあり、材料要件が再構築されつつあります。先進パッケージング材料は、チップレット設計と3Dスタッキングアーキテクチャが新しい相互接続と熱ソリューションを必要とするため、CAGR 11.8%で加速しています。ファブリケーション材料は2024年の売上高シェアで63%を占め、依然として優位を保っているが、価値創造は下流に移行しつつあり、パッケージングの革新がシステム性能を形成するようになっています。また、電気自動車のワイドバンドギャップパワーデバイスへの軸足や、北米と欧州の国内材料サプライチェーンにインセンティブを与える戦略的リショアリングプログラムも需要を後押ししています。重要な化学物質をめぐる地政学的緊張(2019年の日本のフッ化水素規制が最も顕著)は、多様な調達戦略の重要性を強調しています。

世界の半導体材料市場の動向と洞察

デジタル化主導のファブ拡張

2027年までの300mmファブ設備に予定されている4,000億米ドルは、半導体史上最大の生産能力増強に相当します。テキサス・インスツルメンツだけでも米国の7つのファブで600億米ドルを投じており、マイクロンは国内メモリー設備で2,000億米ドルを計画しています。.各先端ファブでは、ウエハー1枚当たりの特殊化学薬品の消費量が前世代より40%増加しており、サプライヤーは複数の地域で超高純度生産を拡大する必要に迫られています。

5G/AIエンドデバイスの普及

AIアクセラレータは前例のない帯域幅と熱エンベロープを押し広げ、パッケージ・チップあたりの材料費は従来のプロセッサの3倍になります。HBMスタックは、スルーシリコン・ビア銅ピラーや超薄型ダイアタッチフィルムに依存しており、銀を多く含む配合が要求されます。富士フイルムは、2030年までに半導体材料で5,000億円の売上を目標としており、これは主にAI中心のノードに合わせたEUVフォトレジストによるものです。車載分野では、LG ChemのSiCパワーモジュール用高性能銀ペーストが、AI主導のモビリティが温度と電圧の両方の要求をいかに高めるかを例証しています。

コンシューマー・エレクトロニクスの循環性

半導体パッケージング材料セグメントは、2023年に15.5%減少したが、2024年には回復し、スマートフォンやPCの減速が化学品需要に迅速に波及することを示しています。四半期で最大30%の在庫変動は、大量生産の消費者向け製品に専念するサプライヤーを圧迫します。自動車、産業、インフラへの多角化は、この変動を緩和するものではあるが、解消するものではないです。AIによって強化された消費者向け機器の出現は、周期的な振幅を減少させるかもしれないが、材料費のインフレが主要な収益テコとして販売台数の増加に取って代わるため、新たな予測の複雑さをもたらすかもしれないです。

セグメント分析

ウエハー製造用材料は、ウエハー1枚当たり何百ものエッチング、成膜、平坦化工程を反映し、2024年の売上高の63%を占める。ウェットケミカル、電子ガス、CMP消耗品が最大のコストプールを形成しています。金額ベースでは、半導体材料市場のこのスライスは2024年に500億米ドル以上に相当します。先進パッケージングは、チップレット分割がメタライゼーション密度と熱界面性能を有機ラミネートの能力を超えて押し上げるため、現在は規模が小さいもの、CAGR 9.2%で拡大しています。そのため、半導体材料市場は、パッケージング原材料のCAGR 11.8%に支えられ、マルチダイアーキテクチャ用に設計された基板、アンダーフィル、モールドコンパウンドに傾斜しています。

この軸足によって、業界の勢力図も再構築されます。ファブリケーションサプライヤーは規模の恩恵を受けるが、成長曲線はより平坦になります。例えば、BT樹脂ベースの基板は、従来のFR-4よりも微細なラインとスペースを実現し、AIアクセラレータの性能向上を可能にします。プロセス・ノードとパッケージ・アーキテクチャの両方にまたがる材料ベンダーは、ウエハのスタート時点とモジュールの完成時点の両方で費用を獲得することで、クロスサイクルでの回復力を獲得しています。

ウェットプロセス用化学薬品は、洗浄、剥離、エッチングにおけるその普遍的な役割により、2024年の支出額の24%を占め、最大の材料クラスであり続けた。ノードの移行が進むにつれて、ドーズ量は増加し、最先端ファブでは28nmラインよりもウェーハ1枚当たり40%多く酸と塩基が使用されています。フッ化水素や三フッ化窒素を含む特殊ガスは、地政学的な供給規制に直面しています。日本の2019年の輸出規制により、韓国へのフッ化水素の出荷が96.8%削減され、台湾、ベルギー、米国での二重調達が急速に進んでいます。

CMPスラリーおよびパッドは、設計が縮小するごとに平坦化ステップ数が増加するため、安定した上昇を示しています。フォトレジストはEUVの採用とともに進化しており、新しいポリマープラットフォームは、ラインエッジの粗さを劣化させることなく13.5nmの光子照射に耐えなければならないです。基板の技術革新は、300mmシリコンだけでなく、高品質SiCブールやパワーデバイス用200mmGaNウエハーにまで広がっています。これらのシフトを総称して、半導体材料市場は再形成されつつあり、サプライヤーは純度、持続可能性、コストのバランスを取る必要に迫られています。

半導体材料市場は、用途別(ファブリケーション、パッケージング)、材料タイプ別(ウエハー基板、スペシャリティ、その他)、エンドユーザー産業別(コンシューマーエレクトロニクス、通信、その他)、技術ノード別、ファブオーナーシップ別(IDM、ピュアプレイ、その他)、地域別に区分されています。市場予測は金額(米ドル)で提供されます。

地域分析

アジア太平洋地域は、台湾、韓国、日本、中国本土の製造エコシステムが密集しているため、2024年の売上高の55%を占めました。しかし、この地域の集中は、2019年のフッ化水素事件で証明されたように、サプライチェーンを輸出規制のショックにさらします。日本のサプライヤーは、5億4,500万米ドルを投じて新たな化学工場を建設し、高純度ラインの現地管理を確保するために買収を行うことで、回復力を強化しています。

北米は最も急成長している地域であり、520億米ドルのCHIPS法奨励金を背景に2030年までCAGR 6.4%で前進します。インテル、TSMC、サムスンは合わせて年間2,000万枚以上のウエハー生産能力を構築しており、エア・リキード(アイダホ州に2億5,000万米ドル)、エンテグリス(コロラド・スプリングスに7,500万米ドル)の並行投資も活発化しています。国内でのパッケージングとテストの拡大はリードタイムを短縮し、この地域で生産されるはんだボール合金と先進基板の需要を刺激しています。環境規制当局も同時にPFASフリーの化学物質の採用を加速させており、地域のイノベーターに足がかりを与えています。

欧州は、2030年までに世界シェア20%を達成するため、チップス法を活用しています。メルク、BASF、リンデは、ドイツとフランスの新工場をサポートするため、超高純度硫酸とアンモニアラインをアップグレードしています。インドは成熟ノードとOSATの第二のハブとして台頭しており、グリーンフィールド投資で特殊ガスメーカーを惹きつけています。中東とアフリカはまだ発展途上だが、再生可能エネルギー・プロジェクトに関連した電力機器組立の現地化という主権者の努力から恩恵を受ける可能性があります。これらの動きを総合すると、半導体材料市場は地理的に再分配され、地政学的リスクが緩和される一方で、冗長性によって総支出が増加します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- デジタル化主導の工場拡張

- 5G/AIエンドデバイスの普及

- 自動車の電動化とADAS

- 先端ノード投資(5nm)

- チップレットと異種統合BOMアップリフト

- 地域化主導の安全在庫政策

- 市場抑制要因

- コンシューマーエレクトロニクスの循環性

- 新規化学物質のための高い資本集約度

- PFAS化学物質に関する環境規制

- APACにおけるフッ化水素の供給安全保障

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- ファブリケーション

- プロセスケミカルズ

- フォトマスク

- 電子ガス

- フォトレジストアンシラリー

- スパッタリングターゲット

- シリコン

- その他のファブリケーション材料

- パッケージング

- 基板

- リードフレーム

- セラミックパッケージ

- ボンディングワイヤ

- 封止樹脂

- ダイ・アタッチ材料

- その他のパッケージング材料

- ファブリケーション

- 材料タイプ別

- ウエハー基板

- 特殊ガス

- ウェットプロセス化学品

- フォトレジストおよび付属品

- CMPスラリーおよびパッド

- 先進パッケージング材料

- エンドユーザー業界別

- コンシューマー・エレクトロニクス

- 通信分野

- 製造/ 産業用IoT

- 自動車

- エネルギーとユーティリティ

- その他

- 技術ノード別

- 45nm以上

- 28-45 nm

- 14-22 nm

- 7-10 nm

- 5nm未満

- ファブ所有別

- IDM

- ピュアプレイ鋳造

- ファブレス(鋳造所経由で購入した材料)

- OSAT/組立・テスト

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- DuPont de Nemours, Inc.

- BASF SE

- Showa Denko Materials Co., Ltd.

- Tokyo Ohka Kogyo Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Merck KGaA(EMD Electronics)

- LG Chem Ltd.

- Henkel AG and Co. KGaA

- Indium Corporation

- SUMCO Corporation

- JSR Corporation

- KYOCERA Corporation

- Versum Materials(Merck)

- Caplinq Europe B.V.

- Nichia Corporation

- International Quantum Epitaxy Plc.

- Sumitomo Chemical Co., Ltd.

- DOW Inc.

- Air Liquide Electronics

- Linde plc Electronics

- SK Materials Co., Ltd.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日