|

市場調査レポート

商品コード

1892896

外来がん治療点滴市場機会、成長要因、業界動向分析、および2026年から2035年までの予測Outpatient Oncology Infusion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 外来がん治療点滴市場機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月15日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

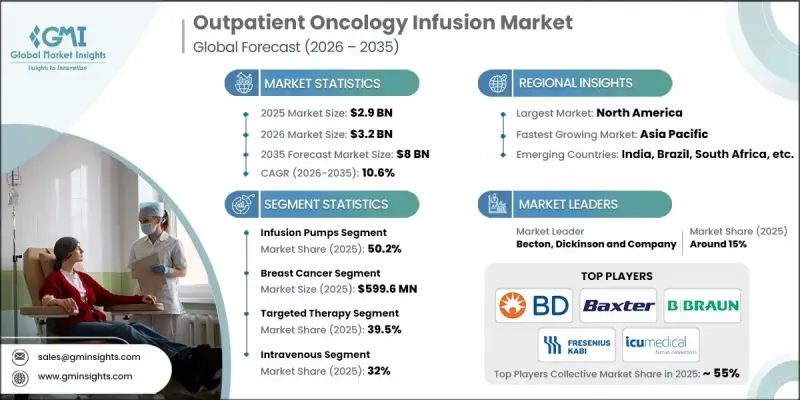

世界の外来がん治療点滴市場は、2025年に29億米ドルと評価され、2035年までにCAGR10.6%で成長し、80億米ドルに達すると予測されています。

市場拡大の背景には、費用対効果の高い外来治療への需要増加、がん罹患率の上昇、がん啓発を推進する政府施策、ならびに点滴技術の発展が挙げられます。さらに、標的療法や免疫療法の導入拡大、価値に基づく医療への移行、遠隔医療を活用した点滴サービスが需要を牽引しております。生活習慣要因、肥満、環境的影響ががん症例数の増加に寄与しており、効果的でアクセスしやすい治療法の必要性が高まっています。外来点滴センターは、入院と比較して全体的なコストを削減しながら、患者様により便利で効率的な治療モデルを提供します。さらに、自動投与、エラー警報、電子健康記録(EHR)との互換性を備えた先進的なスマート点滴ポンプの統合により、安全性と運用効率の両方が向上し、世界中で外来がん点滴サービスの魅力が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 29億米ドル |

| 予測金額 | 80億米ドル |

| CAGR | 10.6% |

輸液ポンプセグメントは2025年に50.2%のシェアを占めました。これらの機器は、携帯可能な設計とスマートシステム統合を特徴とし、患者の快適性を高め、柔軟な投与を可能にし、正確な投与量をサポートします。ポンプの技術的進歩は、外来輸液サービスの成長において中心的な役割を果たしています。

2025年時点で、標的療法セグメントは39.5%のシェアを占めました。これらの療法は、がんに関連する特定の分子経路に作用し、制御された注入によって投与されます。その投与には外来注入センターが好ましく、正確な投与量と患者の反応を監視するための高度な注入装置と熟練した人材の必要性を促進しています。

北米の外来がん点滴市場は2025年に43.1%のシェアを占め、大幅な成長が見込まれています。同地域は先進的な医療インフラ、多数のがん患者、革新的な点滴技術の積極的な導入という利点を有しています。包括的な保険適用範囲と価値に基づく医療への移行により、患者様は入院環境に比べ、より手頃な費用で外来がん治療を受けられるようになりました。外来診療施設におけるスマート輸液ポンプや統合型電子健康記録(EHR)システムの導入は、患者安全性と業務ワークフローを向上させ、市場のさらなる成長を促進しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的に増加するがんの有病率

- 費用対効果の高い外来医療への選好の高まり

- 輸液ポンプにおける技術的進歩

- がん啓発に向けた政府主導の取り組みの急増

- 業界の潜在的リスク&課題

- がん治療の高コスト

- 機会

- 電子健康記録(EHR)との相互運用性を備えたスマート輸液ポンプの導入

- 治療コスト削減に向けたバイオシミラーの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- LAMEA

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- バリューチェーン分析

- 償還シナリオ

- 政策環境

- 疫学シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- LAMEA

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2021-2034

- 輸液ポンプ

- 静脈内セット

- 静脈カニューレ

- 針なしコネクター

第6章 市場推計・予測:用途別、2021-2034

- 肺がん

- 肝臓がん

- 乳がん

- 前立腺がん

- その他のがん

第7章 市場推計・予測:治療法別、2021-2034

- 化学療法

- 標的療法

- 免疫療法

- ホルモン療法

第8章 市場推計・予測:投与経路別、2021-2034

- 筋肉内(IM)

- 静脈内(IV)

- 皮下投与

- その他の投与方法

第9章 市場推計・予測:地域別、2021-2034

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

第10章 企業プロファイル

- B. Braun

- Baxter

- Becton, Dickinson and Company

- Fresenius Kabi

- ICU Medical

- IRADIMED

- Medtronic

- Micrel

- MOOG

- NIPRO

- Penlon

- Teleflex

- Terumo