ワイヤレス心臓モニタリングシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Wireless Cardiac Monitoring Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740792

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

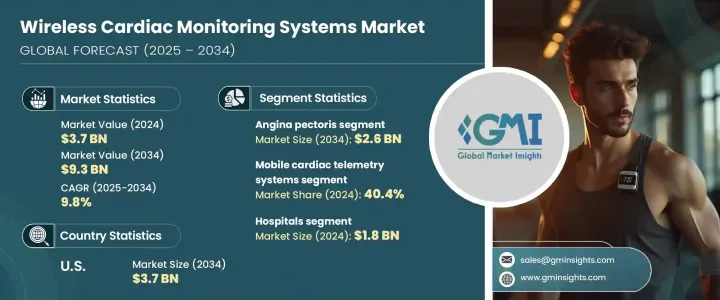

ワイヤレス心臓モニタリングシステムの世界市場規模は、2024年に37億米ドルとなり、リアルタイムの遠隔心臓ケアに対する需要の高まりと、世界の心血管疾患の有病率の増加により、CAGR 9.8%で成長し、2034年には93億米ドルに達すると予測されています。

ワイヤレス心臓モニタリングシステムは、ヘルスケア専門家が心臓の健康をモニターする方法を変革し、継続的な追跡とワイヤレスデータ伝送を可能にしています。これらのシステムは、心房細動、心不全、不整脈などの心臓に関連する疾患の早期発見において、より迅速で正確な臨床対応を可能にするほぼリアルタイムの洞察を提供することにより、重要な役割を果たしています。高齢化社会と慢性疾患を持つ患者において継続的なモニタリングの需要が高まるにつれ、ワイヤレス心臓モニタリングの魅力はより顕著になっています。

技術革新は依然としてこのマーケットの勢いを支える重要な触媒です。新世代のデバイスは現在、リアルタイムのECG伝送、AI対応分析、クラウドプラットフォームとの統合などの高度な機能を提供し、臨床医に心臓データをより効果的に解釈し、迅速に行動する力を与えています。これらのツールは診断の精度を大幅に高め、特に外来や遠隔地での患者の治療成果を向上させる。分散型ケアや在宅モニタリングへのシフトの高まりがこの市場拡大をさらに後押しし、これらのシステムは現代の心臓ケアに不可欠な要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 93億米ドル |

| CAGR | 9.8% |

市場セグメンテーションでは、植え込み型心臓モニター(ICM)、モバイル心臓テレメトリー(MCT)システム、その他のワイヤレス心臓モニター製品に分類されます。2023年時点の世界市場規模は34億米ドルで、2024年の収益シェアはモバイル心臓テレメトリーシステムが40.4%を占めています。MCT機器は、リアルタイムで連続的に心臓リズムをモニタリングし、Bluetoothや携帯電話接続を使用して自律的にアラートを送信することができます。この機能により、異常な心臓活動の即時検出と報告が保証され、従来の短期モニタリングでは見過ごされがちな一過性の不整脈の診断に積極的なアプローチが提供されます。このセグメントの安定した成長は、外来患者での幅広い採用と、ポータブルでコスト効率の高いモニタリング・ソリューションへの嗜好の高まりによって、さらに裏付けられています。このような利点は、長期療養を必要とする患者や、再入院や入院コストの削減に重点を置くヘルスケアシステムにとって特に重要です。

ワイヤレス心臓モニタリングシステムはまた、狭心症のような病態の管理においても重要な役割を果たします。狭心症は、重篤な心臓発作に先行する虚血イベントや不整脈を特定するために、継続的な観察を必要とすることがよくあります。リアルタイムのモニタリングは、症状パターンや誘因の評価を容易にし、より個別化されたタイムリーな介入を可能にします。症状が予測不可能に発生したり、非典型的に現れたりする場合、継続的モニタリングは、静的検査法では見逃す可能性のある重要な洞察を提供し、リスク管理と予防医療戦略を支援します。

最終用途の観点から、市場は病院、専門クリニック、診断センター、在宅ケア環境、その他に区分されます。2024年には、病院分野だけで18億米ドルに達します。高度な循環器科と専門スタッフを擁する病院は、ワイヤレス心臓技術を率先して採用し、診断精度の向上と患者ケア経路の最適化に活用しています。クラウド統合とAI主導のデータ管理をサポートする技術への投資も、こうした施設ではますます一般的になっており、リアルタイム分析と迅速な医療判断を可能にしています。さらに、病院はウェアラブル心電図センサーや埋め込み型デバイスなどの最先端システムを積極的に採用し、質の高いケアの提供と業務の効率化を図っています。

米国のワイヤレス心臓モニタリングシステム市場は、強固なヘルスケア・インフラと心血管疾患の罹患率上昇を背景に、2034年までに37億米ドルを超えると予測されています。同国は、医療技術革新の急速な導入と、規制機関および投資家の双方からの一貫した支援の恩恵を受けています。国内企業や研究開発も、次世代モニタリング・ソリューションの開発において極めて重要な役割を果たしており、市場をさらに前進させています。心臓に関連する健康問題の増加と高度な診断ツールへの需要が、臨床現場や家庭での採用率を押し上げています。

この業界は依然として競合が激しく、Medtronic、Abbott Laboratories、Boston Scientific、iRhythm Technologies、Koninklijke Philips N.V.などの主要企業が世界市場シェアの約40%を占めています。これらの企業は、この急速に進化する市場で優位に立つために、遠隔モニタリング、AI支援診断、シームレスなデータ伝送技術におけるブレークスルーに引き続き注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患(CVD)の有病率の増加

- ワイヤレス心臓モニタリング技術の技術的進歩

- 予防ヘルスケアの重要性の高まり

- 業界の潜在的リスク&課題

- 農村部や未開発地域では入手が限られる

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 埋め込み型心臓モニター(ICM)

- モバイル心臓テレメトリーシステム

- 鉛ベース

- パッチベース

- その他の製品

第6章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 冠動脈疾患

- 狭心症

- 動脈硬化症

- 心不全

- 脳卒中

- その他の適応症

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 専門クリニック

- 診断センター

- 在宅ケア環境

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- AliveCor

- Baxter International

- Biotronik

- Boston Scientific

- InfoBionic

- iRhythm Technologies

- Koninklijke Philips N.V.

- Medtronic

- Nihon Kohden

- SmartCardia

- Vital Connect

目次

The Global Wireless Cardiac Monitoring Systems Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 9.3 billion by 2034, driven by the rising demand for real-time, remote cardiac care and the increasing prevalence of cardiovascular diseases worldwide. Wireless cardiac monitoring systems are transforming how healthcare professionals monitor heart health, allowing continuous tracking and wireless data transmission. These systems play a critical role in the early identification of heart-related conditions such as atrial fibrillation, heart failure, and arrhythmias by providing near real-time insights that enable faster and more precise clinical responses. As demand for continuous monitoring rises in aging populations and patients with chronic conditions, the appeal of wireless cardiac monitoring becomes more pronounced.

Technological innovation remains a key catalyst behind this market's momentum. New-generation devices now offer advanced features such as real-time ECG transmission, AI-enabled analytics, and integration with cloud platforms, empowering clinicians to interpret cardiac data more effectively and act promptly. These tools significantly enhance the accuracy of diagnosis and improve patient care outcomes, especially in outpatient or remote settings. The increasing shift toward decentralized care and home-based monitoring further fuels this market expansion, making these systems an essential component of modern cardiac care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 9.8% |

In terms of product segmentation, the market is categorized into implantable cardiac monitors (ICMs), mobile cardiac telemetry (MCT) systems, and other wireless cardiac monitoring products. As of 2023, the global market was valued at USD 3.4 billion, with mobile cardiac telemetry systems accounting for 40.4% of the revenue share in 2024. MCT devices enable real-time, continuous monitoring of cardiac rhythms and autonomously transmit alerts using Bluetooth or cellular connectivity. This functionality ensures immediate detection and reporting of abnormal heart activity, offering a proactive approach to diagnosing transient arrhythmias that traditional short-term monitoring may overlook. The consistent growth of this segment is further supported by broader adoption in outpatient settings and an increasing preference for portable, cost-efficient monitoring solutions. These benefits are particularly significant for patients requiring long-term care and for healthcare systems focused on reducing hospital readmissions and in-patient costs.

Wireless cardiac monitoring systems also play a vital role in managing conditions like angina pectoris, which often require ongoing observation to identify ischemic events or irregularities that can precede serious cardiac episodes. Real-time monitoring facilitates better evaluation of symptom patterns and triggers, allowing for more personalized and timely interventions. When symptoms occur unpredictably or present atypically, continuous monitoring provides critical insights that static testing methods might miss, thereby supporting risk management and preventive care strategies.

From an end-use perspective, the market is segmented into hospitals, specialty clinics, diagnostic centers, homecare settings, and others. In 2024, the hospital segment alone reached USD 1.8 billion. Hospitals equipped with advanced cardiology departments and specialized staff are leading adopters of wireless cardiac technologies, using them to improve diagnostic precision and optimize patient care pathways. Investments in technologies that support cloud integration and AI-driven data management have also become increasingly common in these facilities, enabling real-time analysis and faster medical decisions. Additionally, hospitals are actively adopting cutting-edge systems, including wearable ECG sensors and implantable devices, to deliver high-quality care and streamline operations.

The United States wireless cardiac monitoring systems market is projected to surpass USD 3.7 billion by 2034, driven by robust healthcare infrastructure and rising incidence of cardiovascular disease. The country benefits from the rapid adoption of medical innovations and consistent support from both regulatory bodies and investors. Domestic companies and research institutes are also playing a pivotal role in developing next-generation monitoring solutions, further advancing the market. The rise in heart-related health concerns and demand for advanced diagnostic tools are pushing adoption rates higher across clinical and home settings.

This industry remains highly competitive, with key players like Medtronic, Abbott Laboratories, Boston Scientific, iRhythm Technologies, and Koninklijke Philips N.V. collectively accounting for around 40% of the global market share. These companies continue to focus on breakthroughs in remote monitoring, AI-assisted diagnostics, and seamless data transmission technologies to stay ahead in this fast-evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased prevalence of cardiovascular diseases (CVDs)

- 3.2.1.2 Technological advancements in wireless cardiac monitoring technologies

- 3.2.1.3 Rising emphasis on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability in rural and underdeveloped areas

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implantable cardiac monitors (ICM)

- 5.3 Mobile cardiac telemetry systems

- 5.3.1 Lead-based

- 5.3.2 Patch-based

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Angina pectoris

- 6.4 Atherosclerosis

- 6.5 Heart failure

- 6.6 Stroke

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Diagnostic centers

- 7.5 Home care settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AliveCor

- 9.3 Baxter International

- 9.4 Biotronik

- 9.5 Boston Scientific

- 9.6 InfoBionic

- 9.7 iRhythm Technologies

- 9.8 Koninklijke Philips N.V.

- 9.9 Medtronic

- 9.10 Nihon Kohden

- 9.11 SmartCardia

- 9.12 Vital Connect

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日