|

市場調査レポート

商品コード

2019250

香水市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Perfume Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 香水市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月18日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

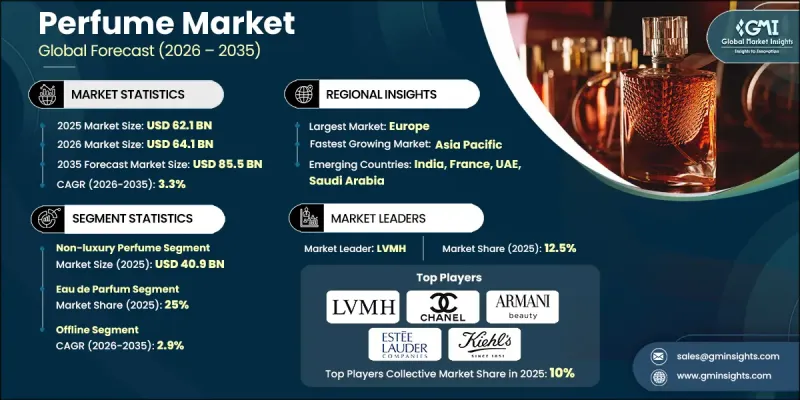

世界の香水市場は2025年に621億米ドルと評価され、CAGR 3.3%で成長し、2035年までに855億米ドルに達すると推定されています。

市場の拡大は、天然成分を使用した特化型香水に対する消費者の関心の高まりと、世界中で香水をより身近なものにしたeコマースプラットフォームの普及によって後押しされています。パーソナルグルーミングサービスの人気上昇やソーシャルメディアプラットフォームの影響も、香水に対する消費者の関心を高めています。また、高度な調合技術や天然・有機成分の採用は、環境意識の高い購入者を惹きつけています。さらに、ユニセックスフレグランスの動向拡大が消費者層を広げている一方、若年層、特にZ世代の嗜好の変化が、新製品の発売に影響を与えています。フローラル系の香り、特にバラを基調とした革新的なバリエーションが顕著な復活を遂げており、これは消費者の嗜好の変遷を反映しています。総じて、消費者の行動の変化、技術革新、および規制の枠組みが、香水業界を再構築し、着実な市場成長を牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 621億米ドル |

| 予測額 | 855億米ドル |

| CAGR | 3.3% |

2025年、ノンラグジュアリー香水セグメントは409億米ドルに達し、2035年までCAGR2.9%で成長すると予想されています。このセグメントの成長は、製品の価格の手頃さと、日常使いのフレグランスに対する需要の高まりに支えられています。消費者は手頃な価格帯の中で多様な選択肢を求める傾向が強まっており、これが着実な拡大を後押ししています。オンライン小売チャネルの成長は、さらにアクセスのしやすさを高め、顧客が幅広い種類のノンラグジュアリー香水を手軽に探せるようにしています。その結果、このセグメントは市場で強固な地位を維持し続けると同時に、中価格帯のフレグランス製品の普及を支えています。

オードパルファム(EDP)セグメントは2025年に25%のシェアを占め、2026年から2035年にかけてCAGR 3.8%で成長すると予測されています。EDPは香料オイルの濃度がバランスよく調整されており、パルファムよりも持続時間が長く、かつ手頃な価格となっています。その手頃な価格と、多様な香りの選択肢が相まって、EDPは特に中間所得層の消費者の間で人気を博しています。身だしなみへの意識の高まりや、フレグランスを通じた自己表現のトレンド拡大が、同セグメントの成長をさらに後押ししています。香りの配合における継続的な革新やターゲットを絞ったマーケティングが功を奏し、世界中で幅広い層を惹きつけています。

米国香水市場は80%のシェアを占め、2025年には147億米ドルの市場規模を記録しました。これは、ニッチでパーソナライズされた香水への消費者の嗜好の変化に加え、環境に優しく持続可能なフレグランスへの関心の高まりに牽引されたものです。ソーシャルメディアプラットフォームや著名人による推奨は、ブランドの認知度を高め続け、購買決定に影響を与えています。フレグランス(香水)の革新と流通の主要拠点である東海岸は、動向形成と市場拡大を支える上で極めて重要な役割を果たしています。富裕層の消費者、革新的なマーケティング戦略、そしてeコマースチャネルの高い普及率の組み合わせにより、米国は世界的に見て主要な市場であり続けることが確実視されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制の枠組み

- 規格および認証

- 環境規制

- 輸出入規制

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーターのファイブフォース分析

- PESTEL分析

- 消費者行動分析

- 購買パターン

- 選好分析

- 地域ごとの消費者行動の差異

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品タイプ別、2022-2035

- 高級香水

- 一般向け香水

第6章 市場推計・予測:香水タイプ別、2022-2035

- パルファムまたはド・パルファム

- オードパルファム(EDP)

- オードトワレ(EDT)

- オー・ド・コロン(EDC)

- その他(オー・フレッシュなど)

第7章 市場推計・予測:香りのタイプ別、2022-2035

- フローラル

- オリエンタル

- ウッディ

- フレッシュ

- その他(グルマン、フルーティなど)

第8章 市場推計・予測:消費者層別、2022-2035

- 男性

- 女性

- ユニセックス

第9章 市場推計・予測:価格別、2022-2035

- 49ドル以下

- 50~149ドル

- 150ドル以上

第10章 市場推計・予測:流通チャネル別、2022-2035

- オンライン

- eコマース

- 企業ウェブサイト

- オフライン

- スーパーマーケット/ハイパーマーケット

- 専門小売店

- その他(個人経営の小売店など)

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ(MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Armani Beauty

- Burberry

- Bvlgari

- Chanel

- Dior

- Estee Lauder

- Gucci

- Hermes

- Kiehl's

- LVMH

- Michael Kors

- Paris Hilton

- Tom Ford

- Victoria's Secret

- Zara