|

市場調査レポート

商品コード

1892769

グリホサート市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Glyphosate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| グリホサート市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月11日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

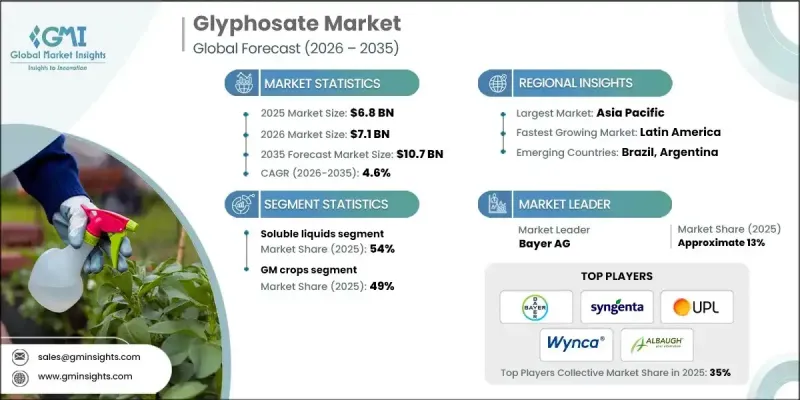

世界のグリホサート市場は、2025年に68億米ドルと評価され、2035年までにCAGR4.6%で成長し、107億米ドルに達すると予測されています。

グリホサートは、管理責任や規制要件の高まりにもかかわらず、作付け前の除草、遺伝子組み換え作物の栽培における作物生育中の使用、収穫後の刈り株管理において、依然として基盤的な役割を担っています。本市場は、保全耕作や不耕起栽培の普及、多作化による集約化、価格に敏感な地域におけるヘクタール当たりのコスト優位性によって支えられています。一方で、欧州の一部地域における耐性問題や規制強化により、ユーザーは精密散布や多様なタンクミックスへの移行を迫られています。中国の技術サプライヤーは生産能力の合理化と環境コンプライアンスの向上を図り、純度基準を高め、安定した長期供給に依存する世界の製剤メーカー向けに価格を安定させています。排水処理と排出ガスの管理強化により、過去の急激な需要変動サイクルは最小限に抑えられ、南北アメリカおよび欧州の製剤メーカーは確実な計画立案が可能となりました。生産者はパルス幅変調、区画制御、無人航空機によるスポット散布、デジタルプラットフォームを導入し、効果と規制順守を維持しながら散布量を最適化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 68億米ドル |

| 予測金額 | 107億米ドル |

| CAGR | 4.6% |

水溶性液体セグメントは2025年に54%のシェアを占め、2035年までCAGR 4.7%で成長すると予測されています。これらの製剤は、取り扱いの容易さ、幅広いタンク混合互換性、吸収性・耐雨性・効果の向上(水路や海岸線管理用の水生生物承認オプションを含む)から好まれています。

遺伝子組換え作物セグメントは2025年に49%のシェアを占め、2035年までCAGR 5%で成長すると予測されています。グリホサートは大豆、トウモロコシ、綿花栽培において依然として不可欠であり、耐性生物型への対応や、永年作物・果樹園における播種前除草処理および指向性ストリップ散布の基盤を形成しています。水生生物および産業用途では、長間隔ラベルおよび水生生物安全製剤が活用されています。

北米グリホサート市場は2025年に23.9%のシェアを占め、成熟かつ高度に専門化された市場であることを反映しています。米国ではEPA承認ラベルに基づき運用され、絶滅危惧種対策として散布時期の厳格化、緩衝地帯の設定、包括的な記録要件が強化されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品構成別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品形態別、2022-2035

- 主要動向

- テクニカル濃縮物(TC-粉末)

- テクニカル・コンセントレート(TK-溶液)

- 水溶性液体濃縮物(SL)

- 水溶性顆粒(SG)

- 即用型液体

- 水生生物用及び特殊製剤

- その他

第6章 市場推計・予測:用途別、2022-2035

- 主要動向

- 遺伝子組換え作物

- 遺伝子組換えトウモロコシ

- 遺伝子組換え綿

- 遺伝子組み換えキャノーラ

- 遺伝子組み換え大豆

- 遺伝子組換えテンサイ

- 遺伝子組み換えアルファルファ

- 非遺伝子組み換え耕作作物

- 穀類

- 油糧作物

- 果物・野菜

- 野菜

- 果物

- 工業用作物

- サトウキビ

- その他の工業用作物

- 非農業用途

- 林業管理

- 芝生・観賞植物

- 水域

- 通行権(ROW)

- 商業・工業用地

- その他

第7章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 大規模商業農家

- 中小規模農家

- 政府・公共機関

- 商業用造園業者

- 産業用植生管理会社

- 住宅消費者

- その他

第8章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- Albaugh, LLC

- Anhui Huaxing Chemical Industry Co., Ltd.

- Arysta LifeScience

- Bayer AG

- Excel Crop Care Limited

- FMC Corporation

- Gharda Chemicals Limited

- Helm AG

- Heranba Industries Limited

- Hubei Xingfa Chemicals Group

- Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

- Jiangsu Yangnong Chemical Co., Ltd.

- Nufarm Limited

- Nutrien Ag Solutions

- Rainbow Agro

- Sinon Corporation(Taiwan)

- Syngenta Group(ChemChina)

- UPL Limited

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Others