|

|

市場調査レポート

商品コード

1858963

創薬における人工知能の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Artificial Intelligence in Drug Discovery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 創薬における人工知能の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年10月14日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

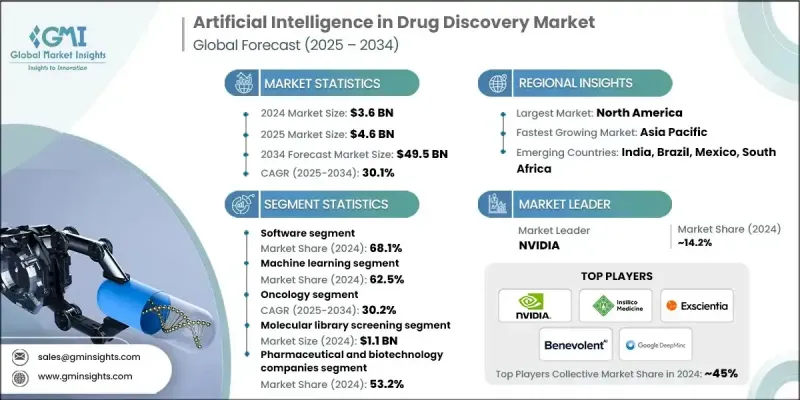

世界の創薬における人工知能市場は、2024年には36億米ドルと評価され、CAGR 30.1%で成長し、2034年には495億米ドルに達すると推定されています。

この例外的な成長は、複雑で慢性的な健康状態の罹患率の上昇と、AI主導型プラットフォームを用いた医薬品開発プロセスの合理化に対する製薬会社の関心の高まりが相まってもたらされています。より迅速で正確な探索プロセスへの要求が、バイオテクノロジー企業や研究機関を、ディープラーニングや予測分析などの先進技術を研究開発ワークフローに統合するよう後押ししています。さらに、データ統合における継続的なイノベーション、デジタルインフラの成長、利害関係者の意識の高まりが、採用を加速させています。特に技術先進地域では、AIスタートアップと製薬メーカーとの協業が拡大しており、治療薬の特定・開発方法が再構築され、ヘルスケア・エコシステム全体に新たな可能性が広がっています。創薬領域におけるAIの役割には、自然言語処理、生成アルゴリズム、ディープラーニングツールなどの高度な技術を使用して、標的の検証を強化し、リード化合物を最適化し、効率的な臨床試験計画をサポートすることが含まれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 36億米ドル |

| 予測金額 | 495億米ドル |

| CAGR | 30.1% |

2024年のソフトウェア分野のシェアは68.1%。この優位性は主に、化合物スクリーニングや構造活性予測といった医薬品開発の初期段階で広く採用されていることによる。ソフトウェアベースのAIツールは現在、自動化、正確性、拡張性を提供する上で不可欠であり、効率的な研究開発ワークフローに対する製薬企業の需要の高まりに対応しています。NLPやニューラルネットワークのようなコア技術の急速な進歩は、精密医療においてソフトウェアが提供できることの限界を押し広げています。

機械学習分野は、創薬の様々な段階において幅広く活用されていることから、2024年には62.5%のシェアを占めています。このセグメントには、教師あり学習モデルと教師なし学習モデル、その他のMLアルゴリズムが含まれます。クラウドコンピューティングの改善とオープンソースフレームワークの利用可能性により、より柔軟で高速かつスケーラブルなモデルのトレーニングと展開が可能になっています。製薬大手とAIに特化した企業との継続的なコラボレーションは、モデル設計のイノベーションを刺激し続け、探索パイプライン全体にわたる予測ツールとリアルタイム分析の開発を加速させています。

北米創薬における人工知能2024年の市場シェアは47.6%で、強力な研究開発投資、広範なデジタルインフラ、AI統合を支援する有利な規制枠組みに後押しされています。デジタル治療薬に関する政府の支援イニシアティブと規制の明確化が市場成長を後押ししています。米国とカナダでは、ハイテク企業と製薬企業との主要な提携により、先進的な創薬ソリューションの開発が進展し、AIプラットフォームの地域的な普及が進んでいます。

世界の創薬における人工知能市場の主要企業は、Exscientia、BenevolentAI、Orakl Oncology、AVAYL、Atomwise、Aevai Health、Cyclica、Examol、IBM Corporation、NVIDIA Corporation、Microsoft、Insilico Medicine、Deep Genomics、DenovAI Biotech、chAIron、Aureka Biotechnologies、LinkGevity、9Bio Therapeutics、Helical、Google(DeepMind)、Deargenです。世界の創薬における人工知能市場で競争力を確保するため、企業は技術革新、戦略的提携、データ主導の製品開発に注力しています。大手企業は、標的同定、分子生成、臨床成功率を高める独自のAIアルゴリズムの開発に投資しています。バイオベンチャーと製薬大手との提携は、大規模なデータセット、ドメイン知識、スケーラブルなコンピューティングリソースへのアクセスを可能にし、より一般的になりつつあります。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 複雑で慢性的な疾患の増加

- ヘルスケアにおけるデータ爆発とデジタル化

- AIアルゴリズムと計算能力の進歩

- ハイテク企業と製薬企業の協力関係の拡大

- 業界の潜在的リスク&課題

- データの質と統合の問題

- 規制と倫理的懸念

- 市場機会

- 個別化医療と精密医療の拡大

- 分子設計におけるジェネレーティブAIの出現

- 促進要因

- 成長可能性分析

- 規制情勢

- 今後の市場動向

- 技術的情勢

- 現在の技術

- 新興技術

- 特許分析

- 投資と資金調達の状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- 提携と協力

- 新製品発表

- 拡張計画

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソフトウェア

- オンプレミス

- クラウドベース

- サービス

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- 機械学習

- ディープラーニング

- 教師あり学習

- 教師なし学習

- その他の機械学習技術

- その他の技術

第7章 市場推計・予測アプリケーションタイプ別、2021-2034

- 主要動向

- 分子ライブラリースクリーニング

- ターゲット同定

- 薬剤の最適化と再利用

- 新薬創製

- 前臨床試験

- その他の用途

第8章 市場推計・予測治療領域別、2021-2034

- 主要動向

- がん領域

- 神経変性疾患

- 炎症性疾患

- 感染症

- 代謝性疾患

- 希少疾患

- 心血管疾患

- その他の治療領域

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 製薬・バイオテクノロジー企業

- 調査受託機関(CRO)

- その他のエンドユース

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 9Bio Therapeutics

- Aevai Health

- Atomwise

- Aureka Biotechnologies

- AVAYL

- BenevolentAI

- chAIron

- Cyclica

- Deargen

- Deep Genomics

- DenovAI Biotech

- Examol

- Exscientia

- Google(DeepMind)

- Helical

- IBM Corporation

- Insilico Medicine

- LinkGevity

- Microsoft

- NVIDIA Corporation

- Orakl Oncology