|

市場調査レポート

商品コード

1833641

子宮内避妊器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Intrauterine Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 子宮内避妊器具の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月10日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

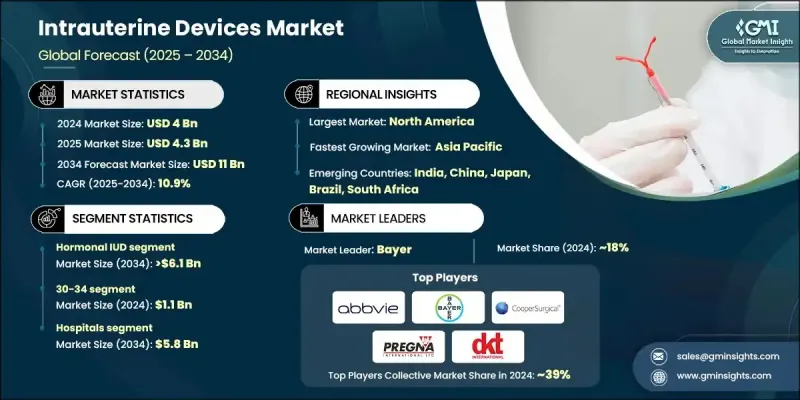

世界の子宮内避妊器具市場は、2024年には40億米ドルと評価され、CAGR 10.9%で成長し、2034年には110億米ドルに達すると推定されています。

この力強い成長軌道の原動力となっているのは、支持的な規制政策、IUDの多様な使用法に関する女性の意識の高まり、そして意図しない妊娠の高い発生率です。IUDは、避妊の役割だけでなく、月経多量出血、子宮内膜症、更年期障害の管理など、より幅広い健康への応用が認められつつあります。教育的取り組みやデジタルヘルスプラットフォームの台頭、リプロダクティブ・ケア情報へのアクセスの改善により、女性は長期的な避妊の選択肢について、より多くの情報を得た上で意思決定できるようになりました。ヘルスケア専門家は、IUDの安全性、有効性、その他の健康上の特典について患者にカウンセリングを行うことで、重要な役割を果たしており、これが世界的な受容を後押ししています。子宮内避妊器具は、小型で柔軟性のあるT字型の避妊具で、信頼性が高く、可逆的で、長時間作用する妊娠予防を提供するように設計されています。鉄を主成分とする非ホルモン性避妊具のような新たな技術革新は、副作用を最小限に抑え、ホルモンを使用しない解決策を提供するために開発されています。これらの技術的進歩は、IUDの展望を変え、女性の選択肢を増やし、長期的な市場拡大を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 40億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 10.9% |

ホルモン性IUDセグメントは2024年に53.8%のシェアを占め、妊娠を予防し月経の健康を改善する効果に支えられています。ホルモン性IUD、特にレボノルゲストレルを放出するIUDは、長期間の保護、低メンテナンス、月経出血の減少や子宮内膜症の症状の緩和といった治療上の利点があるため、広く採用されています。ヘルスケアプロバイダーは、その二重の利点から頻繁にこれらを推奨しており、市場での優位性を強めています。

病院セグメントは2024年に53.2%のシェアを占め、2034年までに58億米ドルを生み出すと予測されています。病院は、熟練した婦人科医や産科医が安全な挿入処置を行うためのアクセスを提供するため、長時間作用型可逆的避妊法を提供する上で不可欠な存在であり続けています。いくつかの地域で産後IUD挿入プロトコルが採用されたことで、アクセスが拡大し、特に妊産婦ヘルスケアシステムがしっかりしている地域では、計画外妊娠の減少に寄与しています。

米国子宮内避妊器具2024年の市場規模は14億4,000万米ドルで、2025年から2034年にかけてCAGR 10.3%で成長すると推定されています。公衆衛生への取り組みや啓蒙活動の活発化により、安全で効果的かつ利便性の高い避妊法としてIUDの使用が奨励されています。毎日のピルのような短期的な代替品よりも長時間作用する可逆的避妊への嗜好の高まりが、米国とカナダの多様な人口動態における採用をさらに加速させています。

子宮内避妊器具業界で活躍する著名な企業には、MONA LISA、Meril、Sebela Pharmaceuticals、DKT、PREGNA、SMB、AbbVie、Prosan、GIMA、Bayer、Medicines360、eurogine、GYNO CARE、CooperSurgical、HLL Lifecare Limitedなどがあります。子宮内避妊器具市場における足場を固めるため、主要企業は副作用を最小限に抑え、使い心地を向上させるよう設計された革新的な素材の開発を含め、ホルモン剤と非ホルモン剤の両方の選択肢を持つ製品ポートフォリオの拡大に注力しています。ヘルスケア組織や政府プログラムとの戦略的提携は、アクセスや採用率を拡大するために進められています。また、月経の健康管理など、避妊以外のIUDの利点について女性を教育する啓発キャンペーンにも多くの企業が投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 好ましい規制シナリオ

- さまざまなIUDの適用に関する女性の意識の高まり

- 望まない妊娠の多さ

- 望まない中絶や妊娠を防ぐための政府の取り組み

- 計画的な妊娠の延期への傾向の高まり

- 業界の潜在的リスク&課題

- デバイスの高コスト

- いくつかの健康問題のリスク

- 保険の適用範囲とアクセスのばらつき

- 市場機会

- 長期避妊の需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- 現在の技術

- 新興技術

- 将来の市場動向

- 払い戻しシナリオ

- 消費者行動と動向

- ブランド分析

- パイプライン分析

- 避妊以外の治療への応用

- 価格分析、2024

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 銅付きIUD

- ホルモン性子宮内避妊器具

第6章 市場推計・予測:年齢別、2021-2034

- 主要動向

- 15~19歳

- 20~24歳

- 25~29歳

- 30~34歳

- 35~39

- 40~44歳

- 45歳以上

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 婦人科クリニック

- 地域医療センター

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AbbVie

- Bayer

- CooperSurgical

- DKT

- eurogine

- GIMA

- GYNO CARE

- HLL Lifecare Limited

- Medicines360

- Meril

- MONA LISA

- PREGNA

- Prosan

- Sebela Pharmaceuticals

- SMB