|

市場調査レポート

商品コード

1716576

NANDフラッシュ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測NAND Flash Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| NANDフラッシュ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月03日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

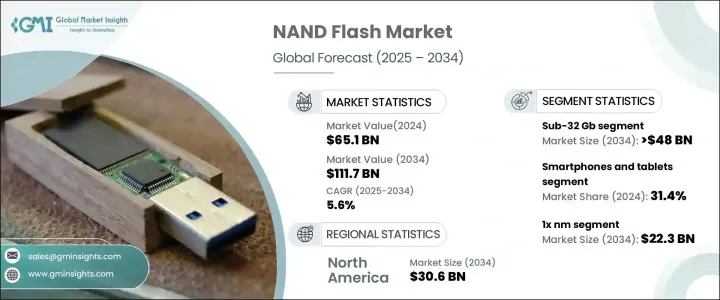

世界のNANDフラッシュ市場は2024年に651億米ドルに達し、2025年から2034年にかけてCAGR 5.6%で成長すると予想されています。

市場成長の主な要因は、3D NAND技術の急速な進歩に加え、コンシューマーエレクトロニクスにおける高性能ストレージソリューションに対する需要の増加です。業界全体でデジタル変革が加速する中、NANDフラッシュメモリはシームレスなデータ処理、高速コンピューティング、大規模ストレージアプリケーションを実現する上で重要な役割を果たしています。コネクテッドデバイスの普及、高解像度メディアの普及、AI主導のアプリケーションへの継続的なシフトは、高度なNANDソリューションの必要性をさらに高めています。クラウド・コンピューティング、エッジ・コンピューティング、IoTの統合も、高密度で電力効率の高いストレージへの需要を高めており、メーカー各社は性能の向上、待ち時間の短縮、エネルギー消費の最適化を実現するイノベーションに注力しています。

消費者は今日、より大容量のストレージとより高速なパフォーマンスをデバイスに求めており、NANDフラッシュ製品に対する大きな需要を牽引しています。各メーカーは、スマートフォン、タブレット、次世代5Gデバイスの進化し続けるニーズをサポートするよう設計された高密度高速メモリ・ソリューションを提供することで対応しています。4Kおよび8Kビデオの消費、モバイルゲーム、AI搭載アプリケーションの急増により、NANDストレージの必要性はかつてないほど高まっています。業界各社は研究開発への投資を続け、自律走行車、スマート家電、産業オートメーションなどの新技術に対応するため、ストレージの効率と耐久性の限界を押し広げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 651億米ドル |

| 予測金額 | 1,117億米ドル |

| CAGR | 5.6% |

NANDフラッシュ市場は、メモリ密度別に32Gb以下、32Gb~128Gb、256Gb~1Tb、1Tb超に区分されます。32Gb未満のセグメントは、組み込みシステム、家電、産業用アプリケーションでの広範な採用により、2034年までに480億米ドルを生み出すと予測されています。特にIoT機器は、コンパクトでコスト効率が高く、エネルギー効率の高いストレージ・ソリューションへの需要が高まる中、このセグメントの成長に貢献しています。このカテゴリのNANDチップは、性能と耐久性が重要なスマート家電、車載インフォテインメントシステム、産業オートメーションでの使用に高い支持を得ています。

用途別では、スマートフォンとタブレットのセグメントが2024年の市場シェア31.4%を占めています。コンテンツ制作の増加、クラウドベースのストレージ、AI主導の機能によってモバイル機器の利用が急増したことが、このセグメントの拡大に大きく寄与しています。最新のスマートフォンは、高解像度の写真、4Kおよび8Kビデオ、高度なゲーム体験を処理するために大容量のストレージを必要とします。モバイル機器が進化し続ける中、このカテゴリーのNANDフラッシュソリューションに対する需要は、予測期間を通じて堅調に推移すると予想されます。

米国のNANDフラッシュ市場は、2034年までに306億米ドルを創出すると予想されます。同国の確立された半導体研究開発部門は、NANDフラッシュ技術の革新を推進し続け、メモリ・ストレージ・ソリューションの世界的リーダーとしての地位をさらに強固なものにしています。大手テクノロジー企業は、データセンター用のNANDフラッシュ・ストレージに大きく依存しており、持続的な需要を確保しています。米国がデジタル経済の最前線に君臨し続ける中、効率的で高密度のストレージ・ソリューションに対するニーズは高まり続け、NANDフラッシュ市場の将来を形作ることになると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 家電製品における高性能ストレージ・ソリューションの需要増加

- データセンターにおけるソリッド・ステート・ドライブ(SSD)の採用増加

- 3D NAND技術の進歩

- AIおよびIoTアプリケーションの拡大

- 自動車産業における需要の高まり

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 競合の増加と価格圧力

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:メモリ密度別、2021年~2034年

- 主要動向

- 32GB未満

- 32 Gb-128 Gb

- 256 Gb-1 Tb

- 1Tb以上

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- スマートフォン、タブレット

- SSDとエンタープライズ・ストレージ

- 家電

- 産業用および車載用

- その他

第7章 市場推計・予測:テクノロジーノード別、2021年~2034年

- 主要動向

- 1x nm

- 1y nm

- 2x nm

- 3x nmとそれ以降

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- ADATA

- Cypress Semiconductor

- Greenliant Systems

- Infineon Technologies

- Intel

- ISSI

- Kingston Technology

- Kioxia

- Macronix International

- Micron Technology

- Netlist

- Phison Electronics

- Powerchip Semiconductor

- Samsung Electronics

- Sandisk

- SK Hynix

- SMIC

- Western Digital

- Winbond Electronics

- Yangtze Memory Technologies Co.(YMTC)

The Global NAND Flash Market reached USD 65.1 billion in 2024 and is expected to grow at a CAGR of 5.6% between 2025 and 2034. The market growth is largely fueled by the increasing demand for high-performance storage solutions in consumer electronics, alongside rapid advancements in 3D NAND technology. As digital transformation accelerates across industries, NAND flash memory plays a crucial role in enabling seamless data processing, high-speed computing, and large-scale storage applications. The rising penetration of connected devices, the proliferation of high-resolution media, and the ongoing shift toward AI-driven applications are further amplifying the need for advanced NAND solutions. Cloud computing, edge computing, and IoT integration have also intensified the demand for high-density, power-efficient storage, prompting manufacturers to focus on innovations that enhance performance, reduce latency, and optimize energy consumption.

Consumers today require larger storage capacities and faster performance in their devices, driving substantial demand for NAND flash products. Manufacturers are responding by delivering high-density, high-speed memory solutions designed to support the ever-evolving needs of smartphones, tablets, and next-generation 5G devices. With the surge in 4K and 8K video consumption, mobile gaming, and AI-powered applications, the necessity for NAND storage has never been higher. Companies in the industry continue to invest in research and development, pushing the boundaries of storage efficiency and endurance to cater to emerging technologies such as autonomous vehicles, smart appliances, and industrial automation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $65.1 Billion |

| Forecast Value | $111.7 Billion |

| CAGR | 5.6% |

The NAND Flash Market is segmented by memory density into several categories, including sub-32 Gb, 32 Gb - 128 Gb, 256 Gb - 1 Tb, and above 1 Tb. The sub-32 Gb segment is projected to generate USD 48 billion by 2034, driven by its widespread adoption in embedded systems, consumer electronics, and industrial applications. IoT devices, in particular, have contributed to the segment's growth as demand for compact, cost-effective, and energy-efficient storage solutions rises. NAND chips in this category are highly favored for use in smart appliances, automotive infotainment systems, and industrial automation, where performance and durability are critical.

Based on applications, the smartphones and tablets segment accounted for a 31.4% market share in 2024. The surge in mobile device usage, driven by increasing content creation, cloud-based storage, and AI-driven functionalities, has significantly contributed to this segment's expansion. Modern smartphones require substantial storage to handle high-resolution photos, 4K and 8K video, and advanced gaming experiences. As mobile devices continue to evolve, the demand for NAND flash solutions in this category is expected to remain strong throughout the forecast period.

The U.S. NAND Flash Market is expected to generate USD 30.6 billion by 2034. The country's well-established semiconductor research and development sector continues to drive innovation in NAND flash technology, further solidifying its position as a global leader in memory storage solutions. Major technology companies rely heavily on NAND flash storage for their data centers, ensuring sustained demand. As the U.S. remains at the forefront of the digital economy, the need for efficient, high-density storage solutions will continue to rise, shaping the future of the NAND flash market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-performance storage solutions in consumer electronics

- 3.2.1.2 Rising adoption of solid-state drives (SSDs) in data centres

- 3.2.1.3 Advancements in 3D NAND technology

- 3.2.1.4 Expansion of ai and IoT applications

- 3.2.1.5 Rising demand in automotive industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions

- 3.2.2.2 Rising competition and price pressure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Memory Density, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Sub-32 Gb

- 5.3 32 Gb - 128 Gb

- 5.4 256 Gb - 1 Tb

- 5.5 Above 1 Tb

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Smartphones and tablets

- 6.3 SSDs and enterprise storage

- 6.4 Consumer electronics

- 6.5 Industrial and automotive

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Technology Node, 2021 - 2034 ($ Mn & Units)

- 7.1 Key trends

- 7.2 1x nm

- 7.3 1y nm

- 7.4 2x nm

- 7.5 3x nm and beyond

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADATA

- 9.2 Cypress Semiconductor

- 9.3 Greenliant Systems

- 9.4 Infineon Technologies

- 9.5 Intel

- 9.6 ISSI

- 9.7 Kingston Technology

- 9.8 Kioxia

- 9.9 Macronix International

- 9.10 Micron Technology

- 9.11 Netlist

- 9.12 Phison Electronics

- 9.13 Powerchip Semiconductor

- 9.14 Samsung Electronics

- 9.15 Sandisk

- 9.16 SK Hynix

- 9.17 SMIC

- 9.18 Western Digital

- 9.19 Winbond Electronics

- 9.20 Yangtze Memory Technologies Co. (YMTC)