|

|

市場調査レポート

商品コード

1573717

メディカルライティングにおけるAI市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年AI in Medical Writing Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| メディカルライティングにおけるAI市場、機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年08月27日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

メディカルライティングにおけるAI世界市場は、2023年に7億5,870万米ドルと評価され、2024年から2032年にかけて13.1%のCAGRで成長すると予測されています。

この成長は、メディカルライティングの合理化、医療データの急増、インテリジェントなジェネレーティブAIソフトウェアソリューションの出現に起因しています。

先進的な機械学習モデルは文書作成を変革し、複雑な医学用語をより深く理解し表現することを可能にしています。これらのモデルは現在、文書の解釈と作成における精度の向上と文脈の関連性を誇っています。さらに、AI主導の分析によってデータ分析が合理化され、より洞察に満ちたデータ中心の医療文書が作成されるようになっています。特筆すべき傾向として、個別化医療におけるAIの応用が増加しており、AIツールは個々の患者データに合わせたカスタマイズされた患者教育資料や治療計画を作成しています。

同市場は、臨床ライティング、科学ライティング、薬事ライティング、患者ドキュメンテーションに分類されています。2023年には、臨床ライティングセグメントがフロントランナーとして浮上し、2億8,500万米ドルを稼ぎ出します。臨床ライティングは、詳細な報告書やプロトコールなど、新薬や医療機器の承認や監督に欠かせない重要な文書を作成します。臨床試験中に生成される複雑な性質と膨大な量の臨床データを考慮すると、正確な文書化が最も重要です。これにより、規制基準の遵守が保証され、正確なデータ分析と解釈が支援されます。

メディカルライティングにおけるAI市場は、製薬・バイオテクノロジー企業、学術・研究機関、医療機器メーカーなど、さまざまなエンドユーザーにサービスを提供しています。2023年には製薬・バイオテクノロジー企業が市場をリードし、2032年までに3億1,960万米ドルを達成すると予測されています。AIを活用したメディカルライティング分野での優位性は、医薬品開発および規制プロセスにおける広範な文書化需要に起因しています。臨床試験、前臨床試験、規制当局への申請など、多くのデータが寄せられる中、これらの企業は研究を強化し、製品の承認を確保するために綿密な文書化を必要としています。

2023年、北米はメディカルライティングにおけるAI市場で2億8,260万米ドルの売上を記録し、2024年から2032年までのCAGRは12.4%と予測されています。さらに、企業による投資と資金調達の活発化が、この地域の市場成長を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ヘルスケアにおけるAI導入の増加

- 医療データ量の増加

- 効率化とコスト削減への要求の高まり

- 技術の進歩

- 熟練メディカルライターの不足

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- データプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- 規制状況

- スタートアップのシナリオ

- 技術展望

- ポーター分析

- PESTEL分析

- 医療分野におけるAI

- 今後の市場動向

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2032年

- 主要動向

- 臨床ライティング

- レギュラトリーライティング

- 患者ドキュメンテーション

- サイエンティフィックライティング

第6章 市場推計・予測:展開モード別、2021年~2032年

- 主要動向

- クラウドベース

- オンプレミス

第7章 市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 製薬・バイオテクノロジー企業

- 医療機器メーカー

- 学術・研究機関

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

第9章 企業プロファイル

- Artos

- Cactus Communications

- CureMetrix, Inc.

- Elsevier

- Epic Systems Corporation

- Freyr

- GENINVO

- GNS Healthcare, Inc.

- IBM Corporation

- NVIDIA Corporation

- Parexel International(MA)Corporation

- Pearson

- TrialAssure

- Trilogy Writing and Consulting GmbH

- Yseop

The Global AI in Medical Writing Market was valued at USD 758.7 million in 2023 and is projected to grow at a CAGR of 13.1% from 2024 to 2032. This growth can be attributed to a heightened emphasis on streamlining medical writing, a surge in medical data, and the emergence of intelligent generative AI software solutions.

Advanced machine learning models are transforming document generation, allowing for a deeper comprehension and articulation of intricate medical language. These models now boast enhanced accuracy and contextual relevance in document interpretation and production. Furthermore, AI-driven analytics are streamlining data analysis, leading to more insightful and data-centric medical writing. A notable trend is the rising application of AI in personalized medicine, where AI tools craft customized patient education materials and treatment plans tailored to individual patient data.

The AI in medical writing industry is classified into type, deployment mode, end-use, and region.

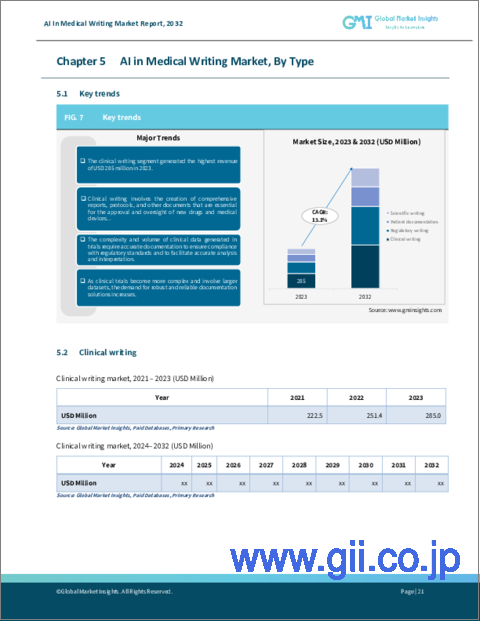

The market categorizes its offerings into clinical writing, scientific writing, regulatory writing, and patient documentation. In 2023, the clinical writing segment emerged as the front runner, raking in USD 285 million. Clinical writing encompasses the formulation of detailed reports, protocols, and other pivotal documents crucial for the endorsement and supervision of novel drugs and medical devices. Given the intricate nature and vast volume of clinical data produced during trials, precise documentation is paramount. This ensures adherence to regulatory benchmarks and aids in accurate data analysis and interpretation.

AI in medical writing market serves various end-users, including pharmaceutical and biotechnology firms, academic and research institutions, medical device manufacturers, and others. In 2023, pharmaceutical and biotechnology companies led the market and are projected to achieve USD 319.6 million by 2032. This dominance in the AI-driven medical writing arena stems from their extensive documentation demands in drug development and regulatory processes. With data pouring in from clinical trials, preclinical studies, and regulatory submissions, these entities necessitate meticulous documentation to bolster their research and secure product endorsements.

In 2023, North America commanded a revenue of USD 282.6 million in the AI in medical writing market, with projections of a 12.4% CAGR from 2024 to 2032 fueled by its sophisticated healthcare infrastructure and a pronounced embrace of technology. Moreover, heightened investments and funding from companies are propelling regional market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of AI in healthcare

- 3.2.1.2 Growing volume of medical data

- 3.2.1.3 Increasing demand for efficiency and cost reduction

- 3.2.1.4 Technological advancements

- 3.2.1.5 Shortage of skilled medical writers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Start-up scenarios

- 3.6 Technology landscape

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 AI in medical applications

- 3.10 Future market trends

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical writing

- 5.3 Regulatory writing

- 5.4 Patient documentation

- 5.5 Scientific writing

Chapter 6 Market Estimates and Forecast, By Deployment Mode, 2021 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates and Forecast, By End-use, 2021 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 Medical device companies

- 7.4 Academic and research institutes

- 7.5 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Artos

- 9.2 Cactus Communications

- 9.3 CureMetrix, Inc.

- 9.4 Elsevier

- 9.5 Epic Systems Corporation

- 9.6 Freyr

- 9.7 GENINVO

- 9.8 GNS Healthcare, Inc.

- 9.9 IBM Corporation

- 9.10 NVIDIA Corporation

- 9.11 Parexel International (MA) Corporation

- 9.12 Pearson

- 9.13 TrialAssure

- 9.14 Trilogy Writing and Consulting GmbH

- 9.15 Yseop