|

市場調査レポート

商品コード

1913318

産業用サイバーセキュリティ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Industrial Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 産業用サイバーセキュリティ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

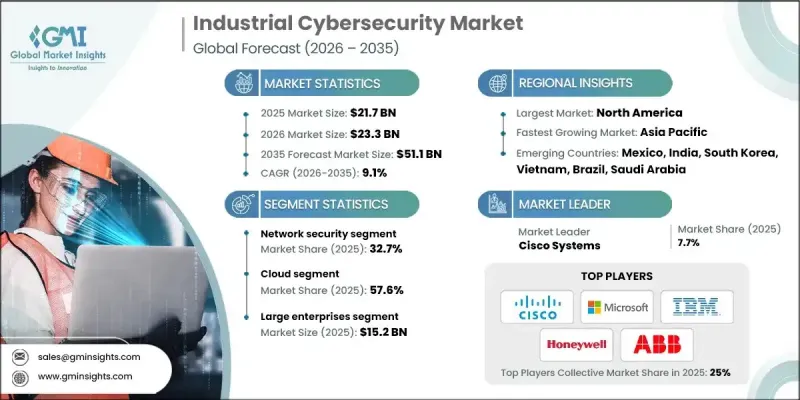

世界の産業用サイバーセキュリティ市場は、2025年に217億米ドルと評価され、2035年までにCAGR 9.1%で成長し、511億米ドルに達すると予測されています。

この成長は、運用システムを標的としたサイバーインシデントの頻度、高度化、および潜在的な影響力の増大によって推進されています。産業オペレーションの相互接続性が高まるにつれ、重要インフラの保護は最優先の戦略的課題となっています。多くの産業環境では依然として重大なセキュリティ上のギャップが存在しており、これにより規制当局の監視が強化され、大規模な経済的・運用上の混乱を回避するため、組織がサイバー防御を強化する圧力が高まっています。人工知能(AI)と機械学習の採用は、脅威の迅速な検知、予測分析、継続的監視を可能にすることで、サイバーセキュリティの枠組みを再構築しています。これらの技術は複雑なワークフロー全体の可視性を向上させ、対応精度を高めます。政府の義務付けやコンプライアンス要件は、重要な産業オペレーション全体でのサイバーセキュリティ導入を加速させており、サイバーセキュリティはインフラ近代化と長期的なリスク管理戦略の中核要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 217億米ドル |

| 予測金額 | 511億米ドル |

| CAGR | 9.1% |

ネットワークセキュリティ分野は2025年に32.7%のシェアを占めました。相互接続されたシステム間でのリアルタイムデータ交換を支える通信チャネルの保護ニーズが高まっていることが、強い需要の背景にあります。業務の継続性は信頼性の高いネットワークに大きく依存しているため、データフローの保護は安全性、生産性、システム安定性を維持する上で不可欠となっています。

クラウド導入セグメントは2025年に57.6%のシェアを占め、2026年から2035年にかけてCAGR10.2%で成長が見込まれます。クラウドベースのサイバーセキュリティソリューションは、多大な初期投資を必要とせずに複数施設にわたる集中管理型保護を実現するため、分散型事業を展開する組織にとって特に魅力的です。

米国の産業用サイバーセキュリティ市場は2025年に71億米ドルに達しました。接続技術の早期導入と産業システム保護への強力な投資が市場リーダーシップを支え、地域別で最も高い産業用サイバーセキュリティ支出を実現しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 重要インフラに対するサイバー攻撃の頻度増加

- 産業用IoT(IIoT)およびスマート製造の導入拡大

- 産業用制御システム(ICS)のデジタル化の進展

- 厳格な政府規制とコンプライアンス要件

- 業界の潜在的リスク&課題

- 熟練した産業用サイバーセキュリティ専門家の不足

- 中小企業におけるサイバーセキュリティ意識の不足

- 市場機会

- AI駆動型脅威検知ソリューションへの需要拡大

- 新興経済国における産業用サイバーセキュリティの拡大

- 産業分野におけるマネージドセキュリティサービスの需要増加

- リアルタイム脅威インテリジェンスおよび監視ソリューションへの需要

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- NISTサイバーセキュリティフレームワーク(CSF)2.0

- NERC CIP

- ISA/IEC 62443

- NIST SP 800-82

- 欧州

- NIS2指令

- IEC 62443

- DORA

- サイバーエッセンシャルズ

- アジア太平洋地域

- 中国のサイバーセキュリティ法(CSL)

- 経済産業省サイバーセキュリティ管理ガイドライン

- シンガポールサイバーセキュリティ法

- SOCI法

- ラテンアメリカ

- ANEELサイバーセキュリティ基準

- ANATELセキュリティ規制

- チリサイバーセキュリティ基本法

- 中東・アフリカ

- 必須サイバーセキュリティ対策(ECC)

- 連邦法令第5号2012(UAE)

- サイバー犯罪法(サウジアラビア)

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 事例研究

- ITおよびOT攻撃の統計

- ITを標的としたサイバー攻撃

- OT(オペレーショナルテクノロジー)を標的としたサイバー攻撃

- IT-OT融合とハイブリッド攻撃

- 高度化・新興産業脅威

- IT・OT攻撃の影響分析

- スキルと人材の動向

- 労働力の供給と需要

- 産業用サイバーセキュリティにおけるスキルギャップ

- 研修および認定プログラム

- スキル開発に向けた政府および業界の取り組み

- 将来展望と機会

- 持続可能性と環境的側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- ソリューション

- ハードウェア

- ソフトウェア

- サービス

- マネージドサービス

- 専門サービス

第6章 市場推計・予測:製品別、2022-2035

- SCADA

- アイデンティティおよびアクセス管理(IAM)

- 統合脅威管理(UTM)

- データ損失防止(DLP)

- IDS/IPS

- SIEM

- DDoS

- その他

第7章 市場推計・予測:導入モデル別、2022-2035

- クラウド

- オンプレミス

- ハイブリッド

第8章 市場推計・予測:企業規模別、2022-2035

- 中小企業

- 大企業

第9章 市場推計・予測:証券別、2022-2035

- ネットワークセキュリティ

- エンドポイントセキュリティ

- アプリケーションセキュリティ

- クラウドセキュリティ

- ワイヤレスセキュリティ

- その他

第10章 市場推計・予測:産業別、2022-2035

- 自動車

- 電子機器

- 食品・飲料

- エネルギー・電力

- 石油・ガス

- 化学

- IT・通信

- 航空宇宙・防衛産業

- その他

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- マレーシア

- インドネシア

- ベトナム

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- Siemens

- Honeywell

- Palo Alto Networks

- Cisco Systems

- Microsoft

- IBM

- Fortinet

- Schneider Electric

- Rockwell Automation

- Claroty

- Nozomi Networks

- Dragos

- Tenable

- ABB

- Thales

- 地域企業

- Armis

- Darktrace

- TXOne Networks

- Waterfall Security

- Radiflow

- Industrial Defender

- Trend Micro

- ABS Group

- Check Point

- Forescout

- 新興企業

- Fox-IT

- ONEKEY

- ACURITY

- Keeper Security

- Underwriters Laboratories