|

|

市場調査レポート

商品コード

1544620

4PL(Fourth Party Logistics)市場、市場機会、成長促進要因、産業動向分析と予測、2024年~2032年Fourth-Party Logistics (4PL) Market, Opportunity, Growth Drivers, Industry Trend Analysis and Forecast, 2024-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 4PL(Fourth Party Logistics)市場、市場機会、成長促進要因、産業動向分析と予測、2024年~2032年 |

|

出版日: 2024年07月08日

発行: Global Market Insights Inc.

ページ情報: 英文 270 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

4PL(Fourth Party Logistics)市場規模は、人工知能(AI)、機械学習、ビッグデータ分析などの先進技術の統合により、2024年から2032年にかけてCAGR6.5%以上で成長します。

フォーブスによると、企業によるAIの世界の採用は2017年以降2倍以上に増加し、堅調なペースで成長を続けており、今後数年間でさらに拡大する見込みです。AIと機械学習により、4PLプロバイダーは予測的洞察を提供し、意思決定プロセスを自動化し、物流業務をリアルタイムで最適化することができます。ビッグデータ分析は、サプライチェーンのダイナミクスに対する深い洞察を提供し、需要予測、在庫管理、輸送の合理化を支援することで、ビジネスをさらに強化します。

企業がサプライチェーンの効率性向上に努める中、先進技術を活用してリアルタイム分析と予測機能を提供する4PLプロバイダーに注目が集まっています。これらのイノベーションにより、企業は潜在的な混乱を予測し、配送ルートを最適化し、全体的な物流パフォーマンスを向上させることができます。予測的洞察は、需要パターンの予測や在庫レベルの管理をより効果的に行い、ルートの最適化は輸送コストを削減し、配送時間を改善するのに役立ちます。これらのテクノロジーの統合は、様々な業界のロジスティクス戦略を再構築し、市場の評価を高めています。

4PLロジスティクス業界は、エンドユーザー、業務モデル、ソリューション、形態、地域によって分類されます。

製造業セグメントは、複雑なサプライチェーンを処理するための効率的で統合されたロジスティクス管理の必要性によって、2032年まで急速に成長します。製造業者は、業務の合理化、コスト削減、サプライチェーンの可視性向上のために4PLプロバイダーを活用しています。これらのロジスティクス・パートナーは、サプライチェーン・プランニング、調達、倉庫管理、輸送を包括する高度なソリューションを提供し、メーカーは効率性と拡張性の向上の恩恵を受けながら、コアコンピタンスに集中することができます。

4PLプロバイダーは、サプライチェーンプロセスを管理するだけでなく、技術的進歩や革新的な戦略を通じてサプライチェーンプロセスを変革します。4PL事業者は、人工知能、機械学習、ビッグデータ分析などの技術を活用して、予測的洞察力を提供し、ルートを最適化し、意思決定能力を高めています。ロジスティクス管理に積極的なアプローチを採用することで、業界のイノベーターは効率性と有効性の新たなベンチマークを設定し、4PL市場の進化を促進しています。

欧州の4PL業界は2024年から2032年にかけて急成長を遂げます。欧州の企業は、より高い柔軟性、効率性、費用対効果の必要性から、複雑なサプライチェーンをナビゲートするために4PLプロバイダーを利用するようになっています。4PLプロバイダーは、地域ごとの専門知識を活かして、国内外の企業の具体的なニーズに対応するオーダーメードのソリューションを提供しています。さらに、インフラとテクノロジーへの大規模な投資が、欧州における4PLサービスの成長をさらに後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- インバウンド物流

- アウトバウンド・ロジスティクス

- 顧客からサプライヤーへの返品プロセス

- 顧客から顧客への返品プロセス

- 付加価値倉庫・配送(VAWD)

- 在庫管理と最適化

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- eコマースと小売の成長

- シームレスなサプライチェーンへの需要

- テクノロジーとデジタル化の重視

- 世界化とクロスボーダー貿易

- 業界の潜在的リスク&課題

- サプライチェーンのコントロールが限定的

- 外部パートナーへの依存度の高さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソリューション別、2021年~2032年

- 主要動向

- サプライチェーン最適化

- 輸送管理

- 在庫管理

- 倉庫管理

- オーダーフルフィルメント

- 貨物輸送

- 物流管理

第6章 市場推計・予測:業務モデル別、2021年~2032年

- 主要動向

- シナジー+組織

- ソリューション・インテグレーター

- 業界イノベーター

第7章 市場推計・予測:形態別、2021年~2032年

- 主要動向

- 航空

- 海上

- 鉄道・道路

第8章 市場推計・予測:エンドユーザー別、2021年~2032年

- 主要動向

- 飲食品

- ヘルスケア

- 小売業

- 自動車

- 製造業

- その他

第9章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ

第10章 企業プロファイル

- Agility Logistics

- CEVA Logistics

- DB Schenker

- DHL Supply Chain

- DSV Panalpina

- Expeditors International

- FedEx Supply Chain

- Geodis

- Hellmann Worldwide Logistics

- Kintetsu World Express

- Kuehne+Nagel

- Maersk(A.P. Moller-Maersk)

- Nippon Express

- Ryder System

- Sinotrans

- TMC, a division of C.H. Robinson

- Toll Group

- UPS Supply Chain Solutions

- XPO Logistics

- Yusen Logistics

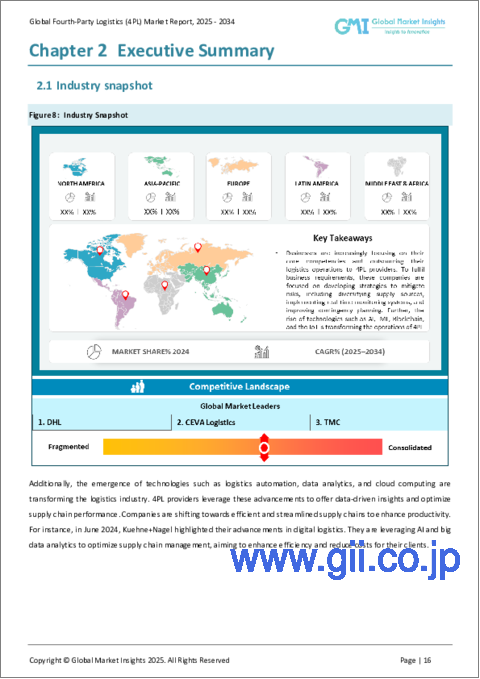

The Fourth-Party Logistics (4PL) Market Size will grow at over 6.5% CAGR during 2024-2032, driven by the integration of advanced technologies such as artificial intelligence (AI), machine learning, and big data analytics. According to Forbes, the global adoption of AI by enterprises has more than doubled since 2017 and continues to grow at a robust pace, with promising prospects for even greater expansion in the coming years. AI and machine learning enable 4PL providers to offer predictive insights, automate decision-making processes, and optimize logistics operations in real-time. Big data analytics further empowers businesses by providing deep insights into supply chain dynamics, helping to forecast demand, manage inventory, and streamline transportation.

As businesses strive to enhance their supply chain efficiency, they are turning to 4PL providers that leverage advanced technologies to offer real-time analytics and predictive capabilities. These innovations enable companies to anticipate potential disruptions, optimize delivery routes, and improve overall logistics performance. Predictive insights help in forecasting demand patterns and managing inventory levels more effectively, while route optimization reduces transportation costs and improves delivery times. The integration of these technologies is reshaping logistics strategies across various industries, adding to market valuation.

The fourth-party logistics industry is classified based on end-user, operational model, solution, mode, and region.

The manufacturing segment will grow rapidly through 2032, driven by the need for efficient, integrated logistics management to handle complex supply chains. Manufacturers are leveraging 4PL providers to streamline their operations, reduce costs, and enhance supply chain visibility. These logistics partners offer advanced solutions that encompass supply chain planning, procurement, warehousing, and transportation, allowing manufacturers to focus on their core competencies while benefiting from improved efficiency and scalability.

The industry innovator segment will witness steady growth through 2032, as 4PL providers not only manage but also transform supply chain processes through technological advancements and innovative strategies. 4PL players are harnessing technologies such as artificial intelligence, machine learning, and big data analytics to offer predictive insights, optimize routes, and enhance decision-making capabilities. By adopting a proactive approach to logistics management, industry innovators are setting new benchmarks for efficiency and effectiveness, driving the evolution of the 4PL market.

Europe fourth-party logistics industry will witness rapid growth over 2024-2032. European businesses are increasingly turning to 4PL providers to navigate the complexities of the supply chain, driven by the need for greater flexibility, efficiency, and cost-effectiveness. The 4PL providers are capitalizing on their regional expertise to offer tailored solutions that address the specific needs of local and international businesses. Additionally, the significant investments in infrastructure and technology are further fueling the growth of 4PL services in Europe.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Inbound logistics

- 3.2.2 Outbound logistics

- 3.2.3 Client to supplier return process

- 3.2.4 Customer to client return process

- 3.2.5 Value-added Warehousing and Distribution (VAWD)

- 3.2.6 Inventory management and optimization

- 3.3 Profit margin analysis

- 3.4 Technology and innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growth of e-commerce and retail

- 3.8.1.2 Demand for seamless supply chains

- 3.8.1.3 Focus on technology and digitalization

- 3.8.1.4 Globalization and cross-border trade

- 3.8.2 Industry pitfalls and challenges

- 3.8.2.1 Limited control over supply chain

- 3.8.2.2 High dependency on external partners

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Solution, 2021 - 2032 ($Bn)

- 5.1 Key trends

- 5.2 Supply chain optimization

- 5.3 Transportation management

- 5.4 Inventory management

- 5.5 Warehouse management

- 5.6 Order fulfillment

- 5.7 Freight forwarding

- 5.8 Distribution management

Chapter 6 Market Estimates and Forecast, By Operational Model, 2021 - 2032 ($Bn)

- 6.1 Key trends

- 6.2 Synergy plus organization

- 6.3 Solution integrator

- 6.4 Industry innovator

Chapter 7 Market Estimates and Forecast, By Mode, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 Air

- 7.3 Sea

- 7.4 Rail and road

Chapter 8 Market Estimates and Forecast, By End User, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.3 Healthcare

- 8.4 Retail

- 8.5 Automotive

- 8.6 Manufacturing

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2032 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.4.7 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Agility Logistics

- 10.2 CEVA Logistics

- 10.3 DB Schenker

- 10.4 DHL Supply Chain

- 10.5 DSV Panalpina

- 10.6 Expeditors International

- 10.7 FedEx Supply Chain

- 10.8 Geodis

- 10.9 Hellmann Worldwide Logistics

- 10.10 Kintetsu World Express

- 10.11 Kuehne+Nagel

- 10.12 Maersk (A.P. Moller-Maersk)

- 10.13 Nippon Express

- 10.14 Ryder System

- 10.15 Sinotrans

- 10.16 TMC, a division of C.H. Robinson

- 10.17 Toll Group

- 10.18 UPS Supply Chain Solutions

- 10.19 XPO Logistics

- 10.20 Yusen Logistics