|

|

市場調査レポート

商品コード

1741046

化学液体水素市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Chemical Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 化学液体水素市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

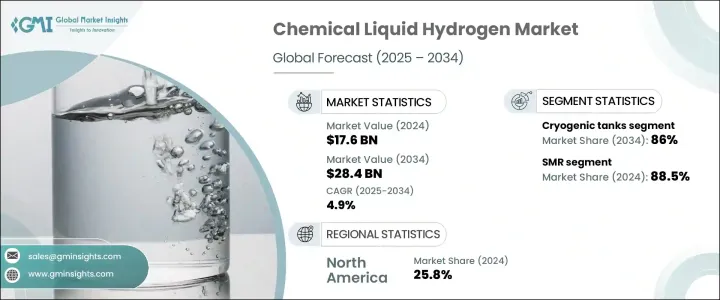

化学液体水素の世界市場規模は、2024年に176億米ドルとなり、化学メーカーが世界の気候変動目標に合わせて低排出ガス原料を追求する中、CAGR 4.9%で成長し、2034年には284億米ドルに達すると予測されています。

世界の産業界が脱炭素戦略に積極的に取り組んでいるため、化学液体水素の需要は加速しています。政府や民間企業は、ネット・ゼロ目標達成の緊急性から、水素インフラに多額の投資を行っています。市場は、再生可能エネルギーコストの低下と技術的ブレークスルーに後押しされ、グリーン水素製造へのシフトを目の当たりにしています。政策支援、投資家の信頼の高まり、戦略的な官民パートナーシップにより、水素開発のための活気あるエコシステムが形成されつつあります。電解槽の進歩、炭素回収技術、スケーラブルな液化システムに対する資金提供の増加は、化学液体水素をより商業的に実現可能で、環境的に持続可能なものにしています。化学、重工業、運輸などの産業部門がクリーンエネルギーへの取り組みを強化するにつれ、利用しやすく柔軟性のある水素ソリューションの必要性がさらに高まっています。この勢いは、今後10年にわたる市場の力強い成長の舞台を整えつつあります。

グリーン水素へのシフトの高まりが、産業用途での採用を促進しています。再生可能エネルギー、特に太陽光発電と風力発電のコスト削減により、電解水素の商業的実現性が高まっています。同時に、電解槽技術と炭素回収システムの進歩により、製造プロセスの効率と持続可能性が向上しています。これらの技術革新により、産業界はより迅速に脱炭素化し、規制の期待に応えることができるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 176億米ドル |

| 予測金額 | 284億米ドル |

| CAGR | 4.9% |

柔軟なインフラと価格設定モデルの導入が進み、水素は産業用ユーザーにとってより利用しやすくなっています。透明性の高いスポット価格は、長期的なコミットメントを必要としないオンデマンド供給を好むバイヤーに新たな機会を創出し、セクターを超えた幅広い参加を促します。この進展は投資家の信頼を高め、クリーン水素イニシアティブへの資金調達を加速させる。官民パートナーシップは、特に液体水素の貯蔵と輸送のためのインフラ整備を進める上で、引き続き役立っています。

水素流通のための大規模なアンモニア変換・液化システムの商業化への取り組みが、牽引力を増しています。こうした開発は、長距離輸送の経済性を向上させ、世界の需要増に対応する一助となっています。しかし、水素関連機器の輸入関税を引き上げる国際貿易政策が進行しているため、将来の製造コストが上昇し、世界のサプライチェーンに摩擦が生じる可能性があります。また、特にクリーン・エネルギー・インフラがまだ立ち上がっていないいくつかの地域では、技術革新が制限され、市場拡大が遅れる可能性があります。

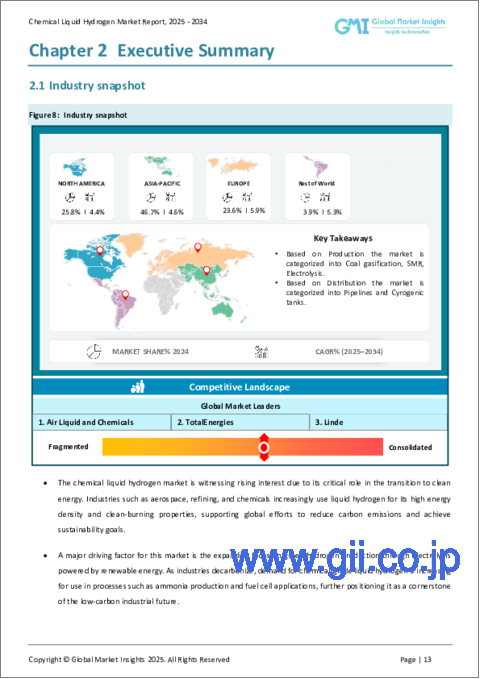

石炭ガス化分野は2024年に11億米ドルを生み出し、2034年までにさらに成長する見通しです。その魅力は、豊富に埋蔵されている石炭を水素に変換し、エネルギーの多様化戦略をサポートすることにあります。エネルギー安全保障が重視され、従来の燃料輸入への依存度が低下する中、この方法への関心は依然として高いです。石炭ベースの水素製造に炭素回収を組み込むことで、プロセスがよりクリーンになり、完全に再生可能な代替エネルギーへの移行の架け橋となります。

流通の面では、パイプラインと極低温タンクが依然として2大輸送方法であり、それぞれが使用事例や地理的ニーズに基づいた明確な利点を提供しています。極低温タンクは、2024年には86%のシェアを占め、化学生産環境において大量の液体水素の貯蔵と移動を可能にする重要な役割を担っていることが明らかになりました。これらのタンクは極低温に耐えるように設計されており、水素を液化した状態で保存し、貯蔵・輸送中のエネルギー損失を最小限に抑えます。このタンクの優位性は、真空断熱材と多層複合材料の技術革新によってさらに裏付けられており、ボイルオフ率を大幅に低減し、全体的な安全性を向上させています。

米国化学液体水素 2024年の市場規模は41億米ドルで、官民の大規模投資に支えられたクリーン・エネルギーへの積極的な国家的後押しがその原動力となっています。連邦政府のインセンティブ、助成金、政策枠組みにより、主要産業地域全体で水素製造・貯蔵施設の急速な開発が可能になりました。化学、重工業、運輸などのセクターからの関心の高まりが、強固な水素サプライチェーンの必要性を後押ししています。

Ballard Power Systems、TotalEnergies、Chart Industries、Messer Group、Linde、Plug Power、ENGIE、Air Products and Chemicals、岩谷産業、ENEOS Corporation、大陽日酸、Air Liquide、Nel ASAなどの企業は、市場シェアを確保するために複数の戦略に注力しています。主な取り組みには、高効率製造技術への投資、エネルギー・化学企業との戦略的提携、モジュール式で拡張性の高い水素プラントの建設などがあります。これらのプレーヤーは、供給監視のためのデジタル統合を優先し、地域のクリーンエネルギー政策に合わせながら、信頼性の高い流通を確保するためのインフラに投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:生産別、2021 –2034

- 主要動向

- 石炭ガス化

- SMR

- 電解

第6章 市場規模・予測:配信別、2021 –2034

- 主要動向

- パイプライン

- 極低温タンク

第7章 市場規模・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 世界のその他の地域

第8章 企業プロファイル

- Air Liquide

- Air Products and Chemicals

- Ballard Power Systems

- Chart Industries

- ENGIE

- ENEOS Corporation

- Hexagon Composites

- Iwatani Corporation

- Linde

- Messer Group

- Nel ASA

- Plug Power

- TotalEnergies

- Taiyo Nippon Sanso Corporation

The Global Chemical Liquid Hydrogen Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 28.4 billion by 2034 as chemical producers pursue low-emission feedstocks to align with global climate targets. Demand for chemical liquid hydrogen is accelerating as industries worldwide move aggressively toward decarbonization strategies. Governments and private players are investing heavily in hydrogen infrastructure, driven by the urgency to meet net-zero goals. The market is witnessing a shift toward green hydrogen production, fueled by lower renewable energy costs and technological breakthroughs. Policy support, growing investor confidence, and strategic public-private partnerships are creating a vibrant ecosystem for hydrogen development. Increasing funding in electrolyzer advancements, carbon capture technologies, and scalable liquefaction systems is making chemical liquid hydrogen more commercially feasible and environmentally sustainable. As industrial sectors such as chemicals, heavy industries, and transportation sectors ramp up their clean energy commitments, the need for accessible and flexible hydrogen solutions is becoming even more critical. This momentum is setting the stage for robust market growth through the next decade.

A growing shift toward green hydrogen is driving adoption across industrial applications. Cost reductions in renewable energy, particularly solar and wind, are making electrolytic hydrogen more commercially viable. Simultaneously, advancements in electrolyzer technology and carbon capture systems are improving the efficiency and sustainability of production processes. These innovations are allowing industries to decarbonize more rapidly and meet regulatory expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $28.4 Billion |

| CAGR | 4.9% |

The increased deployment of flexible infrastructure and pricing models makes hydrogen more accessible to industrial users. Transparent spot pricing creates new opportunities for buyers who prefer on-demand supply without long-term commitments, encouraging broader participation across sectors. This progress boosts investor confidence, accelerating funding for clean hydrogen initiatives. Public-private partnerships continue to help in advancing infrastructure, particularly for liquid hydrogen storage and transportation.

Efforts to commercialize large-scale ammonia conversion and liquefaction systems for hydrogen distribution are gaining traction. These developments are improving the economic viability of long-distance transport, helping meet rising global demand. However, ongoing international trade policies that raise import tariffs on hydrogen-related equipment may inflate future production costs, creating friction in global supply chains. This may also restrict innovation and slow market expansion in several regions, particularly where clean energy infrastructure is still emerging.

The coal gasification segment generated USD 1.1 billion in 2024 and is poised to grow further by 2034. Its appeal lies in converting abundant coal reserves into hydrogen, supporting energy diversification strategies. As more emphasis is placed on energy security and reducing reliance on traditional fuel imports, interest in this method remains strong. Integrating carbon capture into coal-based hydrogen production makes the process cleaner, helping bridge the transition to fully renewable alternatives.

In terms of distribution, pipelines and cryogenic tanks remain the two primary methods for transporting chemical liquid hydrogen, each offering distinct advantages based on use cases and geographic needs. Cryogenic tanks held an 86% share in 2024, underscoring their critical role in enabling the storage and movement of large volumes of liquid hydrogen within chemical production environments. These tanks are engineered to withstand extreme cold temperatures, preserving hydrogen in its liquefied state and minimizing energy losses during storage and transport. Their dominance is further supported by innovations in vacuum insulation and multilayer composite materials, which significantly reduce boil-off rates and improve overall safety.

U.S. Chemical Liquid Hydrogen Market generated USD 4.1 billion in 2024, fueled by an aggressive national push toward clean energy, backed by significant public and private sector investments. Federal incentives, grants, and policy frameworks have enabled the rapid development of hydrogen production and storage facilities across key industrial regions. Increased interest from sectors such as chemicals, heavy industry, and transportation is driving the need for robust hydrogen supply chains.

Companies like Ballard Power Systems, TotalEnergies, Chart Industries, Messer Group, Linde, Plug Power, ENGIE, Air Products and Chemicals, Iwatani Corporation, ENEOS Corporation, Taiyo Nippon Sanso Corporation, Air Liquide, and Nel ASA are focusing on multiple strategies to secure market share. Key initiatives include investing in high-efficiency production technologies, forming strategic alliances with energy and chemical firms, and building modular, scalable hydrogen plants. These players prioritize digital integration for supply monitoring and investing in infrastructure to ensure reliable distribution while aligning with regional clean energy policies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Production, 2021 – 2034 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution, 2021 – 2034 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic tanks

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Air Liquide

- 8.2 Air Products and Chemicals

- 8.3 Ballard Power Systems

- 8.4 Chart Industries

- 8.5 ENGIE

- 8.6 ENEOS Corporation

- 8.7 Hexagon Composites

- 8.8 Iwatani Corporation

- 8.9 Linde

- 8.10 Messer Group

- 8.11 Nel ASA

- 8.12 Plug Power

- 8.13 TotalEnergies

- 8.14 Taiyo Nippon Sanso Corporation