|

市場調査レポート

商品コード

1636159

北米の液体水素-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)North America Liquid Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の液体水素-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

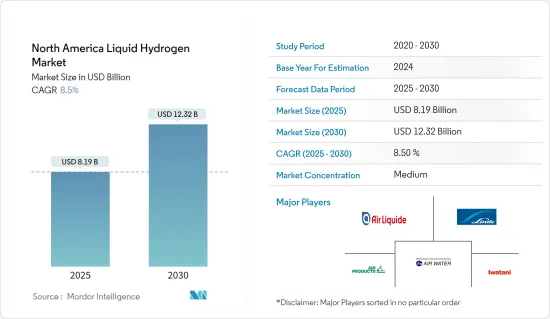

北米の液体水素市場規模は2025年に81億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.5%で、2030年には123億2,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、世界のエネルギー産業の脱炭素化への注目の高まり、自動車産業やその他のエンドユーザー産業の成長と拡大といった要因が、予測期間中の北米の液体水素市場を牽引すると予想されます。

- 一方、液体水素の輸送に伴うコスト高が、液体水素市場の成長にとって大きな課題となることが予想されます。液体水素の大規模貯蔵に伴う複雑さは、この市場の成長範囲をさらに制限します。

- 海洋燃料としての液体水素への注目の高まりと、航空宇宙産業における技術革新の進展は、北米の液体水素市場に有利な成長機会をまもなくもたらすと予想されます。

- 予測期間中、米国が北米の液体水素市場を独占すると予想されます。これは、宇宙探査用の液体水素の需要が増加していることと、商用車への水素燃料電池の採用が増加していることによる。

北米の液体水素市場動向

自動車セグメントが著しい成長を遂げる

- 北米の液体水素市場は、自動車産業におけるクリーン燃料への需要の高まりにより、大きな成長が見込まれています。液体水素は、貯蔵と輸送に優れているため、より大きな利点があります。

- 自動車用途では、固体高分子形燃料電池のような新技術を使用することで、CO2を排出することなく、二次エネルギー源として液体水素を使用することができます。

- 2022年には、米国が北米地域で最も多くの水素ステーションを持つことになります。同国では約54カ所の水素ステーションが稼動しており、カナダ(9カ所)がこれに続きます。さらに、米国の水素経済へのロードマップによると、2030年までに米国内に4,300カ所の大型水素ステーションが建設される予定です。これは、2019年に稼働している大型水素ステーション数の70倍近くになります。

- さらに、米国燃料電池・水素エネルギー協会(FCHEA)によると、2030年までに、米国には4,300カ所の大型水素燃料ステーションが設置されると予想されています。しかし、2050年までには、輸送用燃料が米国の水素需要の最大量を占めるようになると予想されています。化石燃料を動力とする自動車からの汚染は直接環境に排出され、健康被害を引き起こします。

- 例えば、2022年5月、Air Liquideは先週ラスベガスに新しい液体水素製造施設と物流センターを開設し、モビリティセグメントにおける燃料としての液体水素の新たな需要を取り込むことを目指しています。水素は電気自動車のように充電のためのダウンタイムが必要ないため、海運やロジスティクスのセグメントで燃料として人気を集めています。新プラントでは、天然ガスから水素を取り出す水蒸気メタン改質を用いて、4万台の自動車に燃料として十分な水素を製造することができます。このようなプロジェクトは、自動車セグメントで液体水素の積極的な需要を生み出す可能性が高いです。

- したがって、上記の要因に基づき、自動車セグメントは予測期間中、北米の液体水素市場で大きな需要を示すことになると予想されます。

市場を独占する米国

- 北米地域における石油・ガス下流部門の成長は、予測期間中の水素需要にプラスの影響を与えると予想されます。2023年8月現在、米国の製油所における水素純供給能力は709万9,000バレルです。

- 米国ではシェール革命により、主にメキシコ湾岸で石油精製能力がかつてないほど拡大しました。その結果、石油・ガスセクターでは、プロジェクト数や投資額が着実に増加しています。水素は、ハイドロ脱硫と呼ばれる化学分離プロセスで生産される燃料から硫黄分を除去するために使用されます。

- また、米国エネルギー情報局(EIA)は、石油精製における水素の純投入量を8,091万9,000バレルと報告し、2021年比で5.2%の伸びを記録しました。水素はまた、アンモニアやメタノールの生成、化学品や工業用途への工業用熱の供給にも広く使用されています。

- 米国は、宇宙開発計画から始まり、輸送、据置型電力、携帯型電力用途での商用化を可能にする技術に至るまで、水素と関連技術の研究開発の最前線に立ってきました。長年にわたり、エネルギー省(DOE)は、Spark M. Matsunaga Hydrogen Research, Development, and the Energy Policy Act of 2005(EPACT)を含むいくつかの法的権限に沿って、水素と関連技術に関する強力な研究開発活動を確立してきました。

- Air Productsは2022年10月、約5億米ドルを投資して、ニューヨーク州マセナのグリーンフィールドでグリーン(再生可能)液体水素を製造するNissan35トンの施設と、液体水素の流通・販売事業を建設・所有・運営することを計画しています。この施設の商業運転は2026~2027年に開始される予定です。

- 2024年1月、Plug Powerは10億米ドルを超える政府資金を確保しました。ジョージア州の工場で液体グリーン水素の生産を開始しました。こうした新興国市場の開拓は、予測期間中、北米の液体水素市場に好影響を与えると考えられます。

- したがって、上記の要因から、予測期間中、米国が北米の液体水素市場を独占すると予想されます。

北米の液体水素産業概要

北米の液体水素市場は、半固有市場です。市場の主要企業(順不同)には、Air Liquide S.A.、Linde plc、Air Products and Chemicals Inc.、Air Water Inc.、Iwatani Corporationが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 世界エネルギーの脱炭素化への注目の高まり

- 自動車産業の拡大

- 抑制要因

- 液体水素の輸送に伴う高コスト

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 流通

- 容器

- タンク

- エンドユーザー

- 自動車

- 化学・石油化学

- 航空宇宙

- その他

- 地域

- 米国

- カナダ

- その他の北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- AIR WATER INC

- Iwatani Corporation

- Linde plc

- Universal Industrial Gases, Inc.

- Messer Group GmbH

- Engie SA

- Market Player Ranking

第7章 市場機会と今後の動向

- 海洋燃料としての液体水素への注目の高まりと航空宇宙産業における技術革新の増加

目次

Product Code: 50001782

The North America Liquid Hydrogen Market size is estimated at USD 8.19 billion in 2025, and is expected to reach USD 12.32 billion by 2030, at a CAGR of 8.5% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing focus on the decarbonization of the global energy industry along with growth and expansion of the automobile industry and other end-user verticals are expected to drive the North America liquid hydrogen market during the forecast period.

- On the other hand, high costs associated with the transportation of liquid hydrogen is expected to pose a major challenge to the growth of the liquid hydrogen market. Complexities involved in storing liquid hydrogen on a large scale will further restrict the scope of growth for this market.

- Nevertheless, rising emphasis on liquid hydrogen as a marine fuel and increasing innovations in the aerospace industry is expected to create lucrative growth opportunities for the liquid hydrogen market in North America soon.

- United States is expected to dominate the North America liquid hydrogen market during the forecast period. Owing to the growing demand for liquid hydrogen for space exploration and the increasing adoption of hydrogen fuel cells in commercial vehicles.

North America Liquid Hydrogen Market Trends

Automotive Segment to Witness Significant Growth

- North America's liquid hydrogen market is expected to grow significantly due to the rising demand for clean fuel in the automotive industry. Liquid hydrogen offers more significant advantages because of its storage and transportation qualities.

- In an automotive application, liquid hydrogen can be used as a secondary energy source without emitting any CO2 using new technologies like Proton Exchange Membrane fuel cells to produce electricity for an electric drive and a direct fuel for ICE (internal combustion engines).

- In 2022, United States has the most significant number of hydrogen fueling stations in the North American region. There are about 54 operational hydrogen refueling stations in the country, followed by Canada (9 stations). Furthermore, as per the road map to a US hydrogen economy, 4,300 large hydrogen fueling stations in the United States were expected by 2030. This would be close to 70 times the number of operational large fueling stations in 2019.

- Moreover, according to United States Fuel Cell & Hydrogen Energy Association (FCHEA), by the year 2030, the country is expected to have 4,300 large hydrogen fueling stations. However, by 2050, transportation fuels are expected to account for the greatest volume of United States hydrogen demand becuase pollution all around the globe is increasing from vehicles and transportation over time. Pollution from fossil fuel-powered vehicles is emitted directly into the environment, which causes health risks.

- For instance, in May 2022, Air Liquide opened a new liquid hydrogen production facility and logistics center in Las Vegas last week, aiming to capitalize on emerging demand for liquid hydrogen as a fuel in the mobility sector. Hydrogen is gaining traction as a fuel within the shipping and logistics arena because it does not require downtime for charging like electric-powered vehicles. The new plant is capable of producing enough hydrogen to fuel 40,000 vehicles, using steam methane reforming, which derives hydrogen from natural gas. Such projects are likely to create positive demand for liquid hydrogen in automotive segment.

- Therefore, based on the above-mentioned factors, automotive segment is expected to witness significant demand in the North America liquid hydrogen market during the forecast period.

United States to Dominate the Market

- The growth of the oil and gas downstream sector in the North American region is expected to impact the demand for hydrogen during the forecast period positively. As of August 2023, the United States refinery net input of hydrogen capacity stands at 7,099 thousand barrels.

- The shale revolution in the United States has resulted in an unprecedented oil refining capacity creation and expansion, primarily along the Gulf Coast. As a result, steady growth in the number of projects and investments has been witnessed in the oil and gas sector. Hydrogen is used to remove the sulfur content from the fuels produced in a chemical separation process called hydro-desulphurization.

- Also, the United States Energy Information Administration (EIA) reported the net input of hydrogen in oil refining as 80,919 thousand barrels, recording a growth of 5.2% as compared to 2021 levels. Hydrogen is also used extensively in the generation of ammonia and methanol and in providing industrial heat for chemicals and industrial applications.

- The United States has been at the forefront of hydrogen and related technology R&D, from its inception in the space program to enabling technology commercialization in transportation, stationary power, and portable-power applications. Over the years, the Department of Energy (DOE) has established robust R&D activities on hydrogen and related technology aligned with several statutory authorities, including the Spark M. Matsunaga Hydrogen Research, Development, and the Energy Policy Act of 2005 (EPACT).

- Air Products, in October 2022, planned to invest about USD 500 million to build, own and operate a 35 tonne/day facility to produce green (renewable) liquid hydrogen at a greenfield site in Massena, New York, as well as liquid hydrogen distribution and dispensing operations. Commercial operation of this facility is expected to commence in 2026-2027.

- In January 2024, Plug Power secured over USD one billion in government funding. It commenced producing liquid green hydrogen at its Georgia plant. Such developments are likely to create positive impact on the North America liquid hydrogen market during the forecast period.

- Therefore, based on the above-mentioned factors, United States is expected to dominate the liquid hydrogen market in North America during the forecast period.

North America Liquid Hydrogen Industry Overview

The North America liquid hydrogen market is semi consolidated in nature. Some of the major players in the market (in no particular order) include Air Liquide S.A., Linde plc, Air Products and Chemicals Inc., Air Water Inc., and Iwatani Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Focus on the Decarbonization of Global Energy

- 4.5.1.2 Expansion of Automobile Industry

- 4.5.2 Restraints

- 4.5.2.1 High Costs Associated with Transportation of Liquid Hydrogen

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Distribution

- 5.1.1 Containers

- 5.1.2 Tanks

- 5.2 End-User

- 5.2.1 Automotive

- 5.2.2 Chemicals and Petrochemicals

- 5.2.3 Aerospace

- 5.2.4 Other End-Users

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Air Liquide S.A.

- 6.3.2 Air Products and Chemicals, Inc.

- 6.3.3 AIR WATER INC

- 6.3.4 Iwatani Corporation

- 6.3.5 Linde plc

- 6.3.6 Universal Industrial Gases, Inc.

- 6.3.7 Messer Group GmbH

- 6.3.8 Engie SA

- 6.4 Market Player Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Emphasis on Liquid Hydrogen as a Marine Fuel and Increasing Innovations in the Aerospace Industry