液体水素-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Liquid Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692454

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

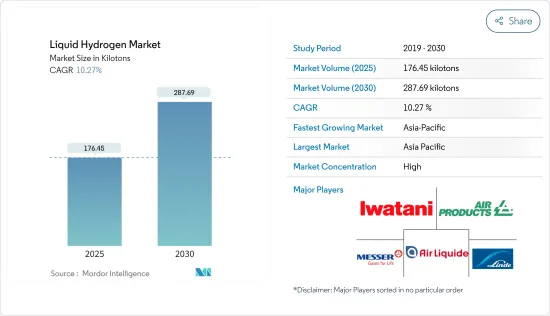

液体水素市場規模は2025年に176.45キロトンと推定され、予測期間(2025年~2030年)のCAGRは10.27%で、2030年には287.69キロトンに達すると予測されます。

COVID-19は、すべての産業が製造プロセスを停止したため、市場にマイナスの影響を与えました。ロックダウン、社会的距離、貿易制裁が世界のサプライ・チェーン・ネットワークに大規模な混乱を引き起こしました。しかし、この状況は2021年には回復しており、予測期間中は市場に利益をもたらすと予想されます。

主なハイライト

- 中期的には、宇宙探査用液体水素の需要拡大と、商用車への水素燃料電池の採用拡大が市場を牽引する主な要因です。

- その反面、取り扱いと貯蔵に関連する高コストが市場成長を抑制する可能性が高いです。

- 海洋燃料としての水素利用が重視されるようになり、航空宇宙産業における技術革新が進んでいることは、今後数年間、市場にとってチャンスとなりそうです。

- アジア太平洋地域が最も高い市場シェアを占めており、予測期間中、この地域が市場を独占する可能性が高いです。

液体水素市場の動向

市場を独占する航空宇宙産業

- 航空宇宙産業は、空港の手荷物取り扱いから水素航空機推進、宇宙産業における極低温エンジンに至るまで、様々な用途への液体水素の応用を意味します。

- 推進用途では、液体水素は液体酸素などの酸化剤と組み合わせて燃料として使用されます。この組み合わせにより、比推力、つまり消費される推進剤の量に対する効率が、既知のロケット推進剤の中で最も高くなります。

- 国際航空運送協会(IATA)によると、民間航空会社の世界売上高は、2021年に4,720億米ドル、2022年に7,270億米ドルと評価され、前年比43.6%の成長率を記録しました。さらに、2023年末には7,790億米ドルに達すると予想されています。

- 航空交通がパンデミックによる減速から回復するにつれ、航空セクターのカーボンニュートラルへの移行を進めるため、温室効果ガス排出規制が各国で強化されています。例えば、米連邦航空局は2022年6月、温室効果ガス排出を抑制するための新たな気候規則を提案しました。この新規則はすでに就航している航空機に適用され、メーカーは空気力学とエンジン効率を改善できるようになります。この規則は、新しい亜音速ジェット機、まだ認証を受けていない大型ターボプロップ機やプロペラ機、2028年1月以降に製造される飛行機に対して効率要件を課すものです。

- 世界中の宇宙計画は、さまざまな航空宇宙事業のロケット燃料として液体水素に依存しています。近年の宇宙計画の伸びが液体水素の需要を牽引しています。

- 2022年、世界各国の宇宙計画に対する政府支出は大幅に増加しました。例えば米国では、政府支出は2021年の545億9,000万米ドルから2022年には619億7,000万米ドルに増加しました。

- 技術進歩の急速な成長は、より高度な衛星への需要を生み出しています。その結果、2022年には186回以上の軌道打ち上げが試みられ、うち180回が成功しました。

- 米航空宇宙局(NASA)によると、1回の打ち上げごとに、シャトルのロケットエンジンは約50万ガロンの冷えた液体水素を消費し、さらに23万9000ガロンが貯蔵のボイルオフや移送作業で枯渇します。1回あたりの消費量の多さと打ち上げ頻度の増加が、液体水素の需要を押し上げています。

- したがって、予測期間中、液体水素の需要は航空宇宙産業で伸びると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、中国、インド、日本などでの液体水素需要の増加により、予測期間中、液体水素の最大市場になると予想されます。

- 中国は、特に航空宇宙産業と自動車産業における代替燃料への強い傾倒により、液体水素にとって強固で有利な市場として位置づけられています。人工衛星の打ち上げやロケットミッションの増加など、航空宇宙分野の大幅な成長に伴い、液体水素の需要は、ロケット燃料に不可欠な役割を果たすため、積極的な急増を目の当たりにしています。

- 中国における燃料電池自動車の販売台数と生産台数の増加も、液体水素ベースの燃料電池の需要拡大に貢献しています。中国汽車工業協会によると、2022年の水素燃料電池車の生産台数と販売台数は、それぞれ3,626台と3,367台で、前年の2倍以上に増加しました。

- 水素燃料は航空機や自動車の動力源としての可能性を示しており、インドでは水素エンジンの進歩に向けた重要な開発や取り組みが行われています。例えば、2023年2月、Reliance Industries LimitedとAshok Leylandは、インド初の水素内燃エンジン(H2-ICE)搭載大型トラックを発売しました。このトラックは、従来のディーゼル内燃機関のアーキテクチャを維持しながら、水素で走行します。積載量19~35トンのH2-ICEトラックは、比較的低いコスト差で、よりクリーンなエネルギーへの迅速な移行を可能にします。

- 自動車検査登録情報協会(AIRIA)によると、2022年3月31日現在、日本で使用されている水素燃料電池自動車は約7,110台で、2021年度の5,280台から増加しました。この水素燃料電池車の大半は水素を燃料とする乗用車です。

- したがって、上記の要因により、アジア太平洋地域における液体水素の需要は予測期間中に増加すると予想されます。

液体水素業界の概要

液体水素市場は高度に統合されています。市場の主要企業(順不同)には、エア・リキード、エア・プロダクツ・アンド・ケミカルズ、リンデPLC、岩谷産業、メッサー・グループGmbHなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 宇宙探査用液体水素の需要拡大

- 商用車における水素燃料電池の採用増加

- 抑制要因

- 取り扱いと貯蔵に伴う高コスト

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 流通

- 極低温タンク

- 高圧チューブトレーラー

- エンドユーザー産業

- 自動車

- 航空宇宙(宇宙を含む)

- 海洋

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 世界のその他の地域

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Air Liquide

- Air Products and Chemicals, Inc.

- Iwatani Corporation

- Linde PLC

- Messer Group GMBH

- Nippon Sanso Holdings Corporation

- Universal Industrial Gases Inc.

第7章 市場機会と今後の動向

- 海洋燃料としての水素利用重視の高まり

- 航空宇宙産業における技術革新の進展

目次

The Liquid Hydrogen Market size is estimated at 176.45 kilotons in 2025, and is expected to reach 287.69 kilotons by 2030, at a CAGR of 10.27% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- In the medium term, the major factors driving the market studied are the growing demand for liquid hydrogen for space exploration and the increasing adoption of hydrogen fuel cells in commercial vehicles.

- On the flip side, the high cost associated with handling and storage is likely to restrain the market growth.

- Growing emphasis on utilizing hydrogen as a marine fuel and increasing innovations in the aerospace industry are likely to act as opportunities for the market in the coming years.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Liquid Hydrogen Market Trends

Aerospace Industry to Dominate the Market

- Aerospace industries imply the application of liquid hydrogen for various applications ranging from airport bagging handling to hydrogen aircraft propulsion to cryogenic engines in the space industry.

- In propulsion applications, liquid hydrogen is used in combination with an oxidizer, such as liquid oxygen, to serve as fuel. This combination yields the highest specific impulse, or efficiency in relation to the amount of propellant consumed, of any known rocket propellant.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 472 billion in 2021 and USD 727 billion in 2022, registering a growth rate of 43.6% Y-o-Y. Furthermore, the revenue is expected to reach USD 779 billion by the end of 2023.

- As air traffic recovers from the pandemic slowdown, the regulations on controlling greenhouse gas emissions are being tightened in different economies to head forward with the transition to carbon neutrality in the aviation sector. For instance, the Federal Aviation Administration, in June 2022, proposed new climate rules for curtailing GHG emissions. The new rules will be applied to planes already in service, allowing manufacturers to improve aerodynamics and engine efficiency. The rules would enforce efficiency requirements for new subsonic jet aircraft, large turboprop and propellor planes that are not yet certified, and planes built after January 2028.

- Space programs across the world rely on liquid hydrogen as the rocket fuel for various aerospace operations. The recent growth in space programs has been driving the demand for liquid hydrogen in recent years.

- In 2022, global government expenditure for space programs in various countries increased considerably. For instance, in the United States, government spending grew from USD 54.59 billion in 2021 to USD 61.97 billion in 2022.

- Rapid growth in technological advancements is creating the demand for more advanced satellites. As a result, in 2022, over 186 attempts of orbital launches, of which 180 were successful.

- According to the National Aeronautics and Space Administration (NASA), for each launch, the rocket engines of each shuttle flight burn about 500,000 gallons of cold liquid hydrogen, with another 239,000 gallons depleted by storage boil-off and transfer operations. The large volume of consumption per operation, coupled with the growing frequency of launches, is propelling the demand for liquid hydrogen.

- Therefore, the demand for liquid hydrogen is expected to grow in the aerospace industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to be the largest market for liquid hydrogen during the forecast period owing to the growing liquid hydrogen demand in China, India, and Japan, among others.

- China's strong inclination toward alternative fuels, particularly in the aerospace and automotive industries, positions the country as a robust and favorablemarket for liquid hydrogen. With substantial growth in the aerospace sector, including increased satellite launches and rocket missions, the demand for liquid hydrogen has witnessed a positive surge due to its essential role in rocket fuel.

- The rising sales and production of fuel cell vehicles in China have also contributed to the growing demand for liquid hydrogen-based fuel cells. According to the China Association of Automobile Manufacturers, the production and sales of hydrogen fuel cell vehicles in 2022 more than doubled compared to the previous year, with 3,626 and 3,367 units produced and sold, respectively.

- Hydrogen fuel presents opportunities for powering aircraft and automobiles, and significant developments and initiatives are taking place in India to advance hydrogen-powered engines. For instance, in February 2023, Reliance Industries Limited and Ashok Leyland launched India's first Hydrogen Internal Combustion Engine (H2-ICE) powered heavy-duty truck. This truck operates on hydrogen while maintaining a conventional diesel combustion engine architecture. With a 19 to 35 tons loading capacity, the H2-ICE truck enables a swift transition to cleaner energy at a relatively lower cost differential.

- According to the Automobile Inspection & Registration Information Association (AIRIA), as of March 31, FY 2022, Japan had approximately 7.11 thousand hydrogen fuel cell vehicles in use, representing an increase from 5.28 thousand in FY 2021. The majority of these hydrogen-fuel cell vehicles are hydrogen-fueled passenger cars.

- Hence, due to the abovementioned factors, the demand for liquid hydrogen in the Asia-Pacific region is expected to increase over the forecast period.

Liquid Hydrogen Industry Overview

The liquid hydrogen market is highly consolidated in nature. Some of the major companies in the market (not in any particular order) include Air Liquide, Air Products and Chemicals Inc., Linde PLC, Iwatani Corporation, and Messer Group GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Liquid Hydrogen for Space Exploration

- 4.1.2 Increasing Adoption of Hydrogen Fuel Cell in Commercial Vehicle

- 4.2 Restraints

- 4.2.1 High Cost Associated with Handling and Storage

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Distribution

- 5.1.1 Cryogenic Tank

- 5.1.2 High-Pressure Tube Trailers

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace (including Outer Space)

- 5.2.3 Marine

- 5.2.4 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Iwatani Corporation

- 6.4.4 Linde PLC

- 6.4.5 Messer Group GMBH

- 6.4.6 Nippon Sanso Holdings Corporation

- 6.4.7 Universal Industrial Gases Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Emphasis on Utilizing Hydrogen as a Marine Fuel

- 7.2 Increasing Innovations in Aerospace Industry

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日