|

市場調査レポート

商品コード

1667150

スーパージャンクションMOSFETの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Super Junction MOSFET Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スーパージャンクションMOSFETの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月31日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

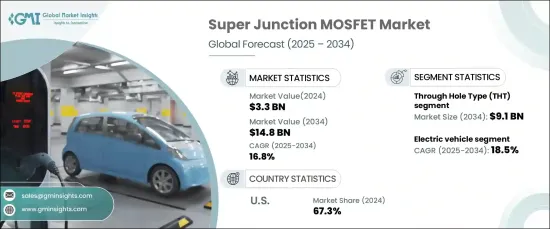

スーパージャンクションMOSFETの世界市場は、2024年に33億米ドルとなり、2025年から2034年にかけてCAGR16.8%で拡大すると予測されています。

この急成長は、さまざまな産業でエネルギー効率が重視されるようになったことが主な要因です。スーパージャンクションMOSFETは、伝導損失とスイッチング損失を最小限に抑え、システム全体の効率を高める上で重要な役割を果たしています。これらのデバイスは、再生可能エネルギー、産業オートメーション、電気自動車など、電力密度の向上とエネルギー消費量の削減が不可欠なエネルギー集約型分野で不可欠です。高電圧アプリケーションの進歩とともに、パワーエレクトロニクスにおけるエネルギー効率の高い技術の採用が拡大していることが、スーパージャンクションMOSFETの需要を引き続き押し上げています。通信、自動車、データセンターなどの業界では、効率的なエネルギー変換、信頼性の高い性能、コンパクトなシステム設計をサポートするため、これらのコンポーネントの導入が増加しています。市場の軌跡は、持続可能でエネルギー効率の高いイノベーションを目指す世界の動向に沿った高度なパワーソリューションの必要性を反映しています。

市場はタイプ別にスルーホールタイプ(THT)と表面実装タイプ(SMT)に区分されます。THT分野は、その耐久性と高電力放散への対応力により、2034年までに91億米ドルに達すると予測されています。これらのMOSFETは、機械的強度と堅牢な熱管理を必要とする要求の厳しいアプリケーションに最適です。一般的な使用事例としては、電源、車載システム、産業機器などがあります。小型化技術へのシフトにもかかわらず、THT MOSFETは過酷な環境での大電流アプリケーションに不可欠であり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 33億米ドル |

| 予測金額 | 148億米ドル |

| CAGR | 16.8% |

逆に、SMT MOSFETは、そのコンパクトな設計と高周波シナリオでの優れた性能で人気を集めています。これらの部品は、コンシューマーエレクトロニクス、通信、再生可能エネルギーシステムなど、スペース効率と放熱が重要なアプリケーションで優れています。SMTデバイスは寄生インダクタンスを低減し、回路性能を向上させるため、高度な熱管理を必要とする最新の高密度電子システムに適しています。

アプリケーションの面では、スーパージャンクションMOSFETは、エネルギー・電力システム、インバータ、産業用セットアップ、電気自動車などで幅広く使用されています。電気自動車分野が最も急成長し、2025年から2034年のCAGRは18.5%と予測されています。これらのMOSFETは、EVパワートレイン、充電ステーション、バッテリー管理システムのエネルギー効率を高め、車両全体の性能を最適化します。

北米では米国が市場を独占し、2024年の地域別売上高の67.3%を占めました。成長の原動力となっているのは、再生可能エネルギー、EVインフラ、産業オートメーションへの投資であり、クリーンエネルギーを推進する政府の取り組みや厳しい効率化規制もその一例です。これらの要因によって、スーパージャンクションMOSFET技術の継続的な進歩と採用のための強固なエコシステムが形成されています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- エネルギー効率に対する需要の高まり

- パワーエレクトロニクスアプリケーションの急成長

- 半導体技術の進歩

- 自動車部門の成長と再生可能エネルギーシステムへのシフト

- 無停電電源システムの生産拡大

- 業界の潜在的リスク・課題

- 高い製造コストと複雑な製造工程

- 技術の進歩と急速な技術革新サイクル

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- スルーホールタイプ

- 表面実装タイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- エネルギー・電力

- コンシューマーエレクトロニクス

- インバーター・UPS

- 電気自動車

- 産業システム

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Alpha and Omega Semiconductor

- Diodes Incorporated

- Fuji Electric

- Infineon Technologies

- KEC Corporation

- Microchip Technology

- Mitsubishi Electric

- Nantong Hornby Electronic Co., Ltd.

- Nexperia

- NXP Semiconductors

- ON Semiconductor

- OS ELECTRONICS Co., Ltd.

- Renesas Electronics

- Richtek Technology Corporation

- ROHM Semiconductor

- SemiHow

- STMicroelectronics

- Texas Instruments

- Toshiba Corporation

- Vishay Intertechnology

The Global Super Junction MOSFET Market, valued at USD 3.3 billion in 2024, is anticipated to expand at a CAGR of 16.8% from 2025 to 2034. This rapid growth is largely attributed to increasing emphasis on energy efficiency across various industries. Super junction MOSFETs play a crucial role in minimizing conduction and switching losses, enhancing overall system efficiency. These devices are indispensable in energy-intensive sectors such as renewable energy, industrial automation, and electric vehicles, where improving power density and reducing energy consumption are vital. The growing adoption of energy-efficient technologies in power electronics, along with advancements in high-voltage applications, continues to propel the demand for super junction MOSFETs. Industries such as telecommunications, automotive, and data centers are increasingly deploying these components to support efficient energy conversion, reliable performance, and compact system designs. The market's trajectory reflects the need for advanced power solutions in line with global trends toward sustainable and energy-efficient innovations.

The market is segmented by type into Through Hole Type (THT) and Surface Mount Type (SMT). The THT segment is forecasted to reach USD 9.1 billion by 2034, driven by its durability and ability to handle high power dissipation. These MOSFETs are ideal for demanding applications requiring mechanical strength and robust thermal management. Common use cases include power supplies, automotive systems, and industrial equipment. Despite the shift toward miniaturized technologies, THT MOSFETs remain vital for high-current applications in harsh environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $14.8 Billion |

| CAGR | 16.8% |

Conversely, SMT MOSFETs are gaining traction for their compact design and superior performance in high-frequency scenarios. These components excel in applications where space efficiency and heat dissipation are critical, such as consumer electronics, telecommunications, and renewable energy systems. SMT devices reduce parasitic inductance and improve circuit performance, making them suitable for modern, high-density electronic systems that require advanced thermal management.

On the application front, super junction MOSFETs are extensively used in energy and power systems, inverters, industrial setups, and electric vehicles. The electric vehicle segment is expected to exhibit the fastest growth, with a projected CAGR of 18.5% between 2025 and 2034. These MOSFETs enhance the energy efficiency of EV powertrains, charging stations, and battery management systems, optimizing overall vehicle performance.

In North America, the United States dominates the market, accounting for 67.3% of regional revenue in 2024. Growth is fueled by investments in renewable energy, EV infrastructure, and industrial automation, alongside government initiatives promoting clean energy and stringent efficiency regulations. These factors create a robust ecosystem for the continued advancement and adoption of super junction MOSFET technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for energy efficiency

- 3.6.1.2 Rapid growth in power electronics applications

- 3.6.1.3 Advancements in semiconductor technology

- 3.6.1.4 Growing automotive sector and shift towards renewable energy system

- 3.6.1.5 Expansion in the production of uninterruptible power systems

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High manufacturing costs and complex production processes

- 3.6.2.2 Technological advancements and rapid innovation cycles

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Through hole type

- 5.3 Surface mount type

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Energy and power

- 6.3 Consumer electronics

- 6.4 Inverter and UPS

- 6.5 Electric vehicle

- 6.6 Industrial system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alpha and Omega Semiconductor

- 8.2 Diodes Incorporated

- 8.3 Fuji Electric

- 8.4 Infineon Technologies

- 8.5 KEC Corporation

- 8.6 Microchip Technology

- 8.7 Mitsubishi Electric

- 8.8 Nantong Hornby Electronic Co., Ltd.

- 8.9 Nexperia

- 8.10 NXP Semiconductors

- 8.11 ON Semiconductor

- 8.12 OS ELECTRONICS Co., Ltd.

- 8.13 Renesas Electronics

- 8.14 Richtek Technology Corporation

- 8.15 ROHM Semiconductor

- 8.16 SemiHow

- 8.17 STMicroelectronics

- 8.18 Texas Instruments

- 8.19 Toshiba Corporation

- 8.20 Vishay Intertechnology