ナノセラミックパウダー- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Nanoceramic Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1686220

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

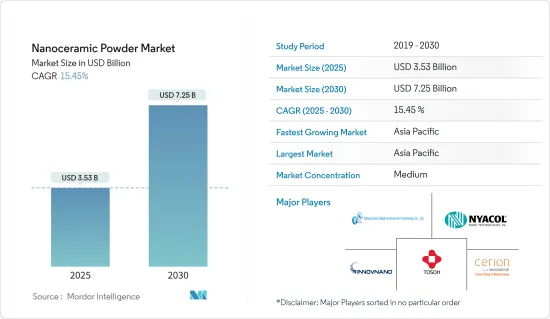

ナノセラミックパウダー市場規模は2025年に35億3,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは15.45%で、2030年には72億5,000万米ドルに達すると予測されます。

主なハイライト

- COVID-19パンデミックは様々な産業に影響を与え、ナノセラミックスパウダーの需要に大きな影響を与えました。需要の変動は、サプライチェーンの混乱、経済活動の低下、消費者行動の変化によるものでした。ナノセラミックスパウダーの需要は、運輸、化学、工業分野で減少傾向が見られ、影響を受けました。しかし、規制が撤廃されて以来、業界は回復しています。

- 市場研究を推進する重要な要因は、エレクトロニクス産業での広範な使用です。さらに、ヘルスケア分野での需要の増加と高性能セラミックコーティングがナノセラミックパウダー市場を牽引しています。

- ナノセラミックパウダーの高い加工コストと健康と安全性の問題は、2024年から2029年の間にナノセラミックパウダーの成長にマイナスの影響を与えると予想されます。

- 炭化ケイ素と窒化ガリウムの用途の増加と、宇宙探査や太陽電池のような先端技術における機会が、市場に新たな成長機会をもたらすと予想されます。

- 2024年から2029年にかけては、アジア太平洋地域が市場を独占すると予想されます。電気・電子部門は、投資の増加と輸出機会によって支えられており、これが成長の原動力となっています。

ナノセラミックパウダー市場動向

電気・電子産業からの需要増加

- 過去20年間、ナノセラミックスに関する膨大な量の研究が行われ、学術界と産業界にいくつかの好結果をもたらしました。その結果、これらの先端材料は、エレクトロニクス分野で幅広い用途を持つようになりました。

- 誘電性、強磁性、圧電性、磁気抵抗、超伝導などの特性を持つナノセラミックパウダーは、電力トランスミッション・デバイス、工業用コンデンサー、高エネルギー貯蔵デバイスなどの用途に最適です。

- ナノセラミックパウダーはエレクトロニクス産業で使用されており、携帯電話、ポータブル・コンピューティング・デバイス、ゲーム・システム、その他のパーソナル・エレクトロニクス・デバイスの高速コンピューティング・チップの製造時に伝統的に使用されています。

- ナノセラミックアルミナは、より高い電圧に耐えることができるため、デバイスのサイズに応じて形状をカスタマイズすることができ、エレクトロニクス分野で最も一般的に使用されています。

- 世界のコンシューマー・エレクトロニクス産業は、携帯電話、ポータブル・コンピューティング・デバイス、ゲーム・システム、その他のパーソナル・エレクトロニクス・デバイスの一貫した需要の増加により、長年にわたり世界中で急成長を遂げています。日本電子情報技術産業協会によると、2023年1~8月の電子製品の総生産額は6兆9,372億3,300万円でした。

- 国家統計局のデータによると、中国の集積回路生産量は2023年4月に281億個に達しました。中国のスマートフォンユーザー数は急速に増加しています。同国のスマートフォンユーザー数は、2023年末までに8億6,820万人に達すると予想されます。

- ASEANはアジア太平洋で最も急成長しているコンシューマー・エレクトロニクス分野です。電気・電子機器製造業は、ASEANで最も顕著なセクターのひとつです。同地域からの輸出総額の約30~35%をこの分野が占めています。ラジオ、コンピューター、携帯電話など、世界の消費者向け電子製品のほとんどは、ASEAN諸国で製造・組み立てられています。

- 北米、特に米国では、エレクトロニクス産業は緩やかな成長が見込まれています。新技術を駆使した製品に対する需要の増加が、今後の市場拡大を後押しすると予想されます。

- 世界のコンシューマー・エレクトロニクス市場は、最新技術のガジェットが人気を博していることから、ここ数年で顕著な成長を遂げています。ホームオートメーションや個人支援機器との融合が、市場に注目すべき成長をもたらしています。

- 電子情報技術産業協会によると、2023年1~9月の電子製品生産額は7兆8,917億2,000万円(~528億6,490万米ドル)でした。

- 前述の要因はすべて、2024年から2029年にかけて市場の需要を増加させる可能性が高いです。

アジア太平洋が市場を独占する見込み

- 世界需要の50%以上を占めるアジア太平洋は、ナノセラミックパウダー材料の最も有望な市場であり、近い将来市場を独占する可能性が高いです。この支配は、同地域のエレクトロニクス産業や医療産業からの需要が増加していることに起因しています。

- 中国はこの地域のナノセラミックパウダー需要の33%以上を占めています。同国はまた、ナノセラミックパウダーの主要な世界市場の一つでもあります。ナノセラミックパウダーの持続的な需要は、堅調なエレクトロニクス、航空宇宙、防衛(A&D)分野を通じて見られます。

- 中国は世界最大のエレクトロニクス生産基地の一つであり、韓国、シンガポール、台湾などの既存の川上メーカーに厳しい競合を提供しています。スマートフォン、OLEDテレビ、タブレット端末などの電子製品は、需要の点で、消費者向け電子機器市場で最も高い成長率を示しています。中国国家統計局によると、2023年4月の中国における家電・コンシューマーエレクトロニクスの小売売上高は、ほぼ610億人民元(85億2,000万米ドル)に達しました。

- さらに、インド・ブランド・エクイティ財団(IBEF)によると、インドの電子機器製造業は2025年までに5,200億米ドルに達すると予想されています。さらに、インドは2025年までに世界第5位の家電・エレクトロニクス産業になると予想されています。インドの電気・電子機器生産は、Make in India、National Policy of Electronics、Net Zero Imports in Electronics、Zero Defect Zero Effectといった、国内製造業の成長、輸入依存度の低下、輸出の活性化、製造業へのコミットメントを提供する政策による政府の取り組みにより、急速に増加すると予想されています。

- この地域はまた、中国とインドが生産能力の最大化に貢献し、ASEAN諸国も市場拡大に加わっていることから、最大の自動車メーカーでもあります。中国は世界最大の自動車市場であり、世界の自動車セクターにおいて極めて重要な役割を果たしています。2022年、中国の自動車生産台数は2,702万台に達し、前年(2,609万台)に比べ3%増加しました。中国での生産台数の多さは、この盛んな産業を支えるナノセラミックパウダーを含む自動車材料の需要が旺盛であることを示しています。

- さらに、中国は最大の航空機メーカーのひとつであり、国内航空旅客の最大市場のひとつでもあります。さらに、同国の航空機部品・組立製造部門は急速に成長しており、200社以上の小規模航空機部品メーカーが存在します。

- ナノセラミックパウダーの使用は、軍用機の高級装備品や部品、エンジン、戦闘機で重要であるため、ナノセラミックパウダーの市場は2024年から2029年まで、この地域で有望視されています。

- 中国政府は毎年国防費を発表しています。中国は2023年3月に1兆5,500億人民元(2,248億米ドル)の国防予算を発表しました。これは、2022年の1兆4,500億人民元(2,296億米ドル)予算から名目上7.2%の増加です。

- 全体として、中国とインドの一貫した成長により、ナノセラミックス粉末の需要は今後数年間、地域全体でより速いペースで増加すると予想されます。アジア太平洋の巨大成長は、世界のナノセラミックパウダー市場の拡大にかなり貢献しています。

ナノセラミックパウダー産業概観

世界のナノセラミックパウダー市場は寡占的で部分的に統合されており、少数の企業が市場を独占しています。主要企業には、Tosoh Corporation、Beijing DK Nano Technology、NYACOL Nano Technologies Inc.、Innovnano-Materiais Avancados SA、Cerion LLCなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エレクトロニクス産業での普及

- ヘルスケア分野からの需要増加

- 高性能セラミック・コーティングの需要増加

- 抑制要因

- 高い加工コスト

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 特許分析

- 原材料分析

第5章 市場セグメンテーション

- タイプ

- 酸化物粉末

- 炭化物粉末

- 窒化物粉末

- ホウ素粉末

- その他のタイプ

- エンドユーザー産業

- 電気・電子

- 工業用

- 輸送

- 医療

- 化学

- 防衛

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 北米

- 米国

- カナダ

- メキシコ

- 世界のその他の地域

- アジア太平洋

第6章 競合情勢

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ABM Advance Ball Mill Inc.

- Beijing DK Nano Technology Co. Ltd

- Cerion LLC

- Inframat Advanced Materials LLC

- Innovnano-materiais Avancados SA

- Nanophase Technologies Corporation

- NYACOL Nano Technologies Inc.

- Tosoh Corporation

- Trunnano

第7章 市場機会と今後の動向

- 宇宙探査や太陽電池のような先端技術におけるビジネスチャンス

- 炭化ケイ素と窒化ガリウムの用途拡大

目次

The Nanoceramic Powder Market size is estimated at USD 3.53 billion in 2025, and is expected to reach USD 7.25 billion by 2030, at a CAGR of 15.45% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic had a diverse effect on different industries, significantly impacting the demand for nanoceramics powder. The demand fluctuations were due to disruption in supply chains, reduced economic activity, and changed consumer behavior. The demand for nanoceramics powder was affected as the transportation, chemical, and industrial sectors witnessed a decreasing trend. However, since restrictions were removed, the industry has been recovering.

- A significant factor driving the market study is widespread use in the electronics industry. Additionally, increasing demand in the healthcare sector and high-performance ceramic coatings drive the nanoceramics powder market.

- The high processing costs of nanoceramic powder and health and safety issues are expected to negatively affect the growth of the nanoceramic powder between 2024 and 2029.

- Increasing applications of silicon carbide and gallium nitride and opportunities in advanced technologies, like space exploration and photovoltaic solar cells, are expected to provide new growth opportunities for the market.

- Asia-Pacific is expected to dominate the market from 2024 to 2029. The electrical and electronics sector is supported by increasing investments and export opportunities, which drive this growth.

Nanoceramic Powder Market Trends

Increasing Demand from the Electrical and Electronics Industry

- Over the last 20 years, there has been a huge amount of study into nanoceramics that has resulted in some positive outcomes for academia and industry. As a result, these advanced materials have a wide range of uses in electronics.

- Nanoceramic powders with properties like dielectricity, ferromagnetism, piezoelectricity, magnetoresistance, and superconductivity make them a perfect fit for applications in power transmission devices, industrial capacitors, high-energy storage devices, and others.

- Nanoceramic powders are used in the electronics industry, and they are traditionally used during the production of high-speed computing chips in cellular phones, portable computing devices, gaming systems, and other personal electronic devices.

- Nanoceramic alumina is most commonly used in electronics, as it can withstand a much higher voltage, so its shape can be customized based on the device size.

- The global consumer electronics industry has been growing rapidly across the world over the years due to the consistently increasing demand for cellular phones, portable computing devices, gaming systems, and other personal electronic devices. According to the Japan Electronics and Information Technology Industries Association, the total production of electronic products accounted for JPY 6,937,233 million in the first 8 months of 2023.

- According to data from the National Bureau of Statistics, China's integrated circuit production volume reached 28.1 billion units in April 2023. The number of smartphone users in China is growing rapidly. The number of smartphone users in the country is expected to reach 868.2 million by the end of 2023.

- ASEAN has the fastest-growing consumer electronics segment in Asia-Pacific. Electrical and electronics manufacturing is one of the most prominent sectors in ASEAN. The sector accounts for about 30-35% of the total exports from the region. Most global consumer electronic products, such as radio, computers, and cellular phones, are manufactured and assembled in ASEAN countries.

- In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. An increase in the demand for new technological products is expected to help the market expansion in the future.

- The global consumer electronics market has witnessed notable growth in the past few years as the latest technological gadgets are gaining popularity. Home automation and integrating devices with personal assistance have provided noteworthy growth to the market.

- According to the Japan Electronics and Information Technology Industries Association, the production of electronic products accounted for JPY 7,891,720 million (~USD 52,864.9 million) in the first nine months (i.e., January- September) of 2023.

- All the aforementioned factors are likely to increase the demand for the market between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

- With over 50% of the global demand, Asia-Pacific is the most promising market for nanoceramic powder materials, which is likely to dominate the market in the near future. This domination can be attributed to the rising demand from the electronics and medical industries in the region.

- China accounts for over 33% of the demand for nanoceramic powder in this region. The country is also one of the major global markets for nanoceramic powder. Sustained demand for nanoceramic powder is witnessed here through its robust electronics, aerospace, and defense (A&D) sectors.

- China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. According to the National Bureau of Statistics of China, retail sales of household appliances and consumer electronics in China amounted to almost CNY 61 billion (USD 8.52 billion) in April 2023.

- Moreover, according to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect Zero Effect, which offer a commitment to growth in domestic manufacturing, lowering import dependence, energizing exports, and manufacturing.

- The region is also the largest manufacturer of automobiles, with China and India contributing to maximum production capacity and ASEAN countries joining the expanding market. China is the largest automobile market globally and plays a pivotal role in the global automotive sector. In 2022, vehicle production in China reached a notable total of 27.02 million units, marking a 3% increase compared to the previous year (26.09 million units). The substantial production volume in China signifies a robust demand for automotive materials, including nanoceramic powder, to support this thriving industry.

- Moreover, China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with the presence of over 200 small aircraft parts manufacturers.

- Since the use of nanoceramic powder is important in high-grade military equipment and parts of military aircraft, engines, and fighter jets, the market for nanoceramic powder looks promising from 2024 to 2029 in the region.

- The Chinese government announces defense expenditure information annually. China announced a defense budget of CNY 1.55 trillion (USD 224.8 billion) in March 2023. This represents a nominal 7.2% increase from the CNY 1.45 trillion (USD 229.6 billion) budget in 2022.

- Overall, with the consistent growth in China and India, the demand for nanoceramics powder is expected to increase at a faster pace in the overall region in the coming years. The huge growth of Asia-Pacific is quite instrumental in the expansion of the global nanoceramics powder market.

Nanoceramic Powder Industry Overvview

The global nanoceramic powder market is oligopolistic and partially consolidated, with few players dominating the market. The major companies include Tosoh Corporation, Beijing DK Nano Technology Co. Ltd, NYACOL Nano Technologies Inc., Innovnano-Materiais Avancados SA, and Cerion LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Widespread Use in the Electronics Industry

- 4.1.2 Increasing Demand from the Healthcare Sector

- 4.1.3 Increasing Demand for High-performance Ceramic Coatings

- 4.2 Restraints

- 4.2.1 High Processing Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

- 4.6 Raw Material Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Oxide Powder

- 5.1.2 Carbide Powder

- 5.1.3 Nitride Powder

- 5.1.4 Boron Powder

- 5.1.5 Other Types

- 5.2 End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Industrial

- 5.2.3 Transportation

- 5.2.4 Medical

- 5.2.5 Chemical

- 5.2.6 Defense

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 North America

- 5.3.3.1 United States

- 5.3.3.2 Canada

- 5.3.3.3 Mexico

- 5.3.4 Rest of the World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABM Advance Ball Mill Inc.

- 6.3.2 Beijing DK Nano Technology Co. Ltd

- 6.3.3 Cerion LLC

- 6.3.4 Inframat Advanced Materials LLC

- 6.3.5 Innovnano-materiais Avancados SA

- 6.3.6 Nanophase Technologies Corporation

- 6.3.7 NYACOL Nano Technologies Inc.

- 6.3.8 Tosoh Corporation

- 6.3.9 Trunnano

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Opportunities in Advanced Technologies, Like Space Exploration and Photovoltaic Solar Cell

- 7.2 Increasing Applications of Silicon Carbide and Gallium Nitride

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日