|

|

市場調査レポート

商品コード

1426989

データセンター・アクセラレータ市場規模:プロセッサタイプ別、タイプ別、用途別、最終用途別、地域別展望&予測 2024年~2032年Data Center Accelerator Market Size - By Processor Type, Type, Application, End-Use, Regional Outlook & Forecast, 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| データセンター・アクセラレータ市場規模:プロセッサタイプ別、タイプ別、用途別、最終用途別、地域別展望&予測 2024年~2032年 |

|

出版日: 2023年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 284 Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

世界のデータセンター・アクセラレータ市場は、人工知能(AI)や機械学習(ML)用途の導入とともに、効率的なデータ処理に対する需要の急増によって、2024年から2032年の間にCAGR 25%で成長すると予測されています。

最近のニールセンIQの調査によると、米国の消費者の78%が持続可能なライフスタイルを優先しています。エネルギー効率に優れた処理に重点を置いて設計されたアクセラレータは、組織が二酸化炭素排出量と運用コストの削減を求める中で、人気を集めています。この動向は、データセンターが環境に与える影響に対する意識の高まりと一致しており、企業はエネルギー消費を最小限に抑えながら高性能を提供するアクセラレータへの投資を促しています。さらに、金融、ヘルスケア、研究などの業界でハイパフォーマンス・コンピューティング(HPC)用途の需要が高まっていることも、市場の成長に寄与しています。

GPU分野は、多様な用途を高速化するためにデータセンターでGPUの採用が増加していることから、調査期間中に大きく成長すると見られています。グラフィックス・プロセッシング・ユニット(GPU)は、グラフィックスのレンダリングという従来の役割を超えて進化し、並列処理タスクに不可欠なものとなっています。さらに、GPUの並列アーキテクチャは、AIやMLアルゴリズムを含む最新の用途の並列化ワークロードの処理に適しています。

クラウド・アクセラレータ分野は、デジタル・トランスフォーメーションを目指す企業にとってクラウドの導入が戦略的必須事項であり続けるため、2032年まで大幅に拡大する見通しです。クラウド・アクセラレータは、クラウドベースの用途のパフォーマンスと効率を強化し、企業がスケーラビリティと柔軟性のメリットを活用できるようにするために不可欠です。

アジア太平洋地域のデータセンター・アクセラレータ市場は、急速な技術導入、急速な都市化、デジタル経済の成長により、2032年まで急成長が見込まれています。中国、インド、日本などの国々は、データセンター・インフラへの投資の増加と先進技術の採用により、業界の収益に貢献しています。さらに、データ集約的な用途やサービスの需要が、同地域におけるデータセンター・アクセラレータの必要性を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 データセンター・アクセラレーター業界考察

- エコシステム分析

- テクノロジーとイノベーションの展望

- 特許分析

- データセンター・インフラへの影響

- サーバーアーキテクチャとワークロードの変化

- 特殊な冷却および電源ソリューションの必要性

- データセンターの運用と管理への影響

- 主要ニュースとイニシアチブ

- 提携/協力

- 合併/買収

- 投資

- 製品発表とイノベーション

- 規制状況

- 影響要因

- 促進要因

- 世界のオンラインサービスの利用拡大

- さまざまな業界における先端技術への需要の世界の高まり

- 北米と欧州で高まるハイパフォーマンス・コンピューティング需要

- 欧州とアジア太平洋地域でハイパースケールデータセンターの設立が増加

- アジア太平洋地域におけるクラウド・コンピューティングとIoTの普及

- 業界の潜在的リスク&課題

- 特殊なインフラの必要性

- 原材料と熟練労働者のコスト上昇

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 各社の市場シェア

- 主要市場プレーヤーの競合分析

- Advanced Micro Devices, Inc.

- Dell Inc.

- Intel Corporation

- Marvell Technology Inc.

- NVIDIA Corporation

- Qualcomm Incorporated

- Synopsys Inc.

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 データセンター・アクセラレータ市場推計・予測:プロセッサタイプ別

- 主要動向:プロセッサタイプ別

- 中央演算処理装置(CPU)

- グラフィカル・プロセッシング・ユニット(GPU)

- FPGA(フィールド・プログラマブル・ゲート・アレイ)

- 特定用途向け集積回路(ASIC)

第6章 データセンター・アクセラレータ市場推定・予測:タイプ別

- 主要動向:タイプ別

- HPCアクセラレーター

- クラウドアクセラレーター

第7章 データセンター・アクセラレータ市場推定・予測:用途別

- 主要動向:用途別

- ディープラーニング

- パブリッククラウドインタフェース

- エンタープライズインターフェース

第8章 データセンター・アクセラレータ市場の推定・予測:エンドユーザー別

- 主要動向:エンドユーザー別

- IT&テレコム

- ヘルスケア

- BFSI

- 政府機関

- エネルギー

- 製造業

- その他

第9章 データセンター・アクセラレータ市場推計・予測:地域別

- 主要動向:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ポーランド

- ベネルクス

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- 中東・アフリカ

- GCC

- 南アフリカ

第10章 企業プロファイル

- Achronix Semiconductor

- Advanced Micro Devices, Inc

- Advantech Co., Ltd.

- Dell Inc.

- GYRFALCON TECHNOLOGY INC.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Intel Corporation

- Lattice Semiconductor

- Lenovo Ltd.

- Marvell Technology Inc.

- Microchip Technology Inc.

- Micron Technology, Inc.

- NEC Corporation

- NVIDIA Corporation

- Qualcomm Incorporated

- Skyworks Solutions Inc.

- Synopsys Inc

- Western Digital Corporation

- Xilinx Inc

Data Tables

- TABLE 1 Global data center accelerator market 360 degree synopsis, 2018-2032

- TABLE 2 Data center accelerator market, 2018 - 2023,

- TABLE 3 Data center accelerator market, 2024 - 2032,

- TABLE 4 Data center accelerator TAM, 2024 - 2032

- TABLE 5 Data center accelerator market, by region, 2018 - 2023 (USD Million)

- TABLE 6 Data center accelerator market, by region, 2024 - 2032 (USD Million)

- TABLE 7 Data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 8 Data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 9 Data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 10 Data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 11 Data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 12 Data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 13 Data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 14 Data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 15 Vendor matrix

- TABLE 16 Patent analysis

- TABLE 17 Industry impact forces

- TABLE 18 Company market share, 2023

- TABLE 19 Competitive analysis of major market players, 2023

- TABLE 20 Central processing unit (CPU) market, 2018 - 2023 (USD Million)

- TABLE 21 Central processing unit (CPU) market, 2024 - 2032 (USD Million)

- TABLE 22 Graphical Processing Unit (GPU) market, 2018 - 2023 (USD Million)

- TABLE 23 Graphical Processing Unit (GPU) market, 2024 - 2032 (USD Million)

- TABLE 24 Field Programmable Gate Array (FPGA) market, 2018 - 2023 (USD Million)

- TABLE 25 Field Programmable Gate Array (FPGA) market, 2024 - 2032 (USD Million)

- TABLE 26 Application Specific Integrated Circuit (ASIC) market, 2018 - 2023 (USD Million)

- TABLE 27 Application Specific Integrated Circuit (ASIC) market, 2024 - 2032 (USD Million)

- TABLE 28 HPC accelerator market, 2018 - 2023 (USD Million)

- TABLE 29 HPC accelerator service market, 2024 - 2032 (USD Million)

- TABLE 30 Cloud accelerator market, 2018 - 2023 (USD Million)

- TABLE 31 Cloud accelerator market, 2024 - 2032 (USD Million)

- TABLE 32 Deep learning training market, 2018 - 2023 (USD Million)

- TABLE 33 Deep learning training market, 2024 - 2032 (USD Million)

- TABLE 34 Public cloud interface market, 2018 - 2023 (USD Million)

- TABLE 35 Public cloud interface market, 2024 - 2032 (USD Million)

- TABLE 36 Enterprise interface market, 2024 - 2032 (USD Million)

- TABLE 37 Enterprise interface market, 2018 - 2023 (USD Million)

- TABLE 38 IT & Telecom market, 2018 - 2023 (USD Million)

- TABLE 39 IT & Telecom market, 2024 - 2032 (USD Million)

- TABLE 40 Healthcare market, 2018 - 2023 (USD Million)

- TABLE 41 Healthcare market, 2024 - 2032 (USD Million)

- TABLE 42 BFSI market, 2018 - 2023 (USD Million)

- TABLE 43 BFSI market, 2024 - 2032 (USD Million)

- TABLE 44 Government market, 2018 - 2023 (USD Million)

- TABLE 45 Government market, 2024 - 2032 (USD Million)

- TABLE 46 Energy market, 2018 - 2023 (USD Million)

- TABLE 47 Energy market, 2024 - 2032 (USD Million)

- TABLE 48 Manufacturing market, 2018 - 2023 (USD Million)

- TABLE 49 Manufacturing market, 2024 - 2032 (USD Million)

- TABLE 50 Others market, 2018 - 2023 (USD Million)

- TABLE 51 Others market, 2024 - 2032 (USD Million)

- TABLE 52 North America data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 53 North America data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 54 North America data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 55 North America data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 56 North America data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 57 North America data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 58 North America data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 59 North America data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 60 North America data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 61 North America data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 62 U.S. data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 63 U.S. data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 64 U.S. data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 65 U.S. data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 66 U.S. data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 67 U.S. data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 68 U.S. data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 69 U.S. data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 70 U.S. data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 71 U.S. data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 72 Canada data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 73 Canada data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 74 Canada data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 75 Canada data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 76 Canada data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 77 Canada data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 78 Canada data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 79 Canada data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 80 Canada data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 81 Canada data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 82 Mexico data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 83 Mexico data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 84 Mexico data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 85 Mexico data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 86 Mexico data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 87 Mexico data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 88 Mexico data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 89 Mexico data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 90 Mexico data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 91 Mexico data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 92 Europe data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 93 Europe data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 94 Europe data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 95 Europe data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 96 Europe data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 97 Europe data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 98 Europe data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 99 Europe data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 100 Europe data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 101 Europe data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 102 UK data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 103 UK data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 104 UK data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 105 UK data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 106 UK data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 107 UK data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 108 UK data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 109 UK data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 110 UK data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 111 UK data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 112 Germany data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 113 Germany data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 114 Germany data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 115 Germany data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 116 Germany data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 117 Germany data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 118 Germany data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 119 Germany data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 120 Germany data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 121 Germany data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 122 France data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 123 France data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 124 France data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 125 France data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 126 France data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 127 France data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 128 France data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 129 France data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 130 France data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 131 France data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 132 Italy data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 133 Italy data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 134 Italy data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 135 Italy data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 136 Italy data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 137 Italy data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 138 Italy data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 139 Italy data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 140 Italy data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 141 Italy data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 142 Spain data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 143 Spain data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 144 Spain data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 145 Spain data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 146 Sapin data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 147 Spain data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 148 Spain data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 149 Spain data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 150 Spain data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 151 Spain data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 152 Poland data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 153 Poland data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 154 Poland data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 155 Poland data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 156 Sapin data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 157 Poland data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 158 Poland data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 159 Poland data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 160 Poland data center accelerator market, by End-use, 2018 - 2023 (USD Million)

- TABLE 161 Poland data center accelerator market, by End-use, 2024 - 2032 (USD Million)

- TABLE 162 Benelux data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 163 Benelux data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 164 Benelux data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 165 Benelux data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 166 Benelux data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 167 Benelux data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 168 Benelux data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 169 Benelux data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 170 Benelux data center accelerator market, by End-use, 2018 - 2023 (USD Million)

- TABLE 171 Benelux data center accelerator market, by End-use, 2024 - 2032 (USD Million)

- TABLE 172 Nordics data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 173 Nordics data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 174 Nordics data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 175 Nordics data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 176 Sapin data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 177 Nordics data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 178 Nordics data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 179 Nordics data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 180 Nordics data center accelerator market, by End-use, 2018 - 2023 (USD Million)

- TABLE 181 Nordics data center accelerator market, by End-use, 2024 - 2032 (USD Million)

- TABLE 182 Asia Pacific data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 183 Asia Pacific data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 184 Asia Pacific data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 185 Asia Pacific data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 186 Asia Pacific data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 187 Asia Pacific data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 188 Asia Pacific data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 189 Asia Pacific data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 190 Asia Pacific data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 191 Asia Pacific data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 192 China data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 193 China data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 194 China data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 195 China data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 196 China data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 197 China data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 198 China data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 199 China data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 200 China data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 201 China data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 202 India data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 203 India data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 204 India data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 205 India data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 206 India data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 207 India data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 208 India data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 209 India data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 210 India data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 211 India data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 212 Japan data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 213 Japan data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 214 Japan data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 215 Japan data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 216 Japan data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 217 Japan data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 218 Japan data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 219 Japan data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 220 Japan data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 221 Japan data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 222 Australia data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 223 Australia data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 224 Australia data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 225 Australia data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 226 Australia data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 227 Australia data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 228 Australia data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 229 Australia data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 230 Australia data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 231 Australia data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 232 South Korea data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 233 South Korea data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 234 South Korea data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 235 South Korea data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 236 South Korea data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 237 South Korea data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 238 South Korea data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 239 South Korea data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 240 South Korea data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 241 South Korea data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 242 Singapore data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 243 Singapore data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 244 Singapore data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 245 Singapore data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 246 Singapore data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 247 Singapore data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 248 Singapore data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 249 Singapore data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 250 Singapore data center accelerator market, by End-use, 2018 - 2023 (USD Million)

- TABLE 251 Singapore data center accelerator market, by End-use, 2024 - 2032 (USD Million)

- TABLE 252 Latin America data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 253 Latin America data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 254 Latin America data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 255 Latin America data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 256 Latin America data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 257 Latin America data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 258 Latin America data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 259 Latin America data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 260 Latin America data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 261 Latin America data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 262 Brazil data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 263 Brazil data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 264 Brazil data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 265 Brazil data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 266 Brazil data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 267 Brazil data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 268 Brazil data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 269 Brazil data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 270 Brazil data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 271 Brazil data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 272 Argentina data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 273 Argentina data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 274 Argentina data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 275 Argentina data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 276 Argentina data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 277 Argentina data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 278 Argentina data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 279 Argentina data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 280 Argentina data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 281 Argentina data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 282 Chile data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 283 Chile data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 284 Chile data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 285 Chile data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 286 Chile data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 287 Chile data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 288 Chile data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 289 Chile data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 290 Chile data center accelerator market, by End-use, 2018 - 2023 (USD Million)

- TABLE 291 Chile data center accelerator market, by End-use, 2024 - 2032 (USD Million)

- TABLE 292 MEA data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 293 MEA data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 294 MEA data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 295 MEA data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 296 MEA data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 297 MEA data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 298 MEA data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 299 MEA data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 300 MEA data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 301 MEA data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 302 GCC data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 303 GCC data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 304 GCC data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 305 GCC data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 306 GCC data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 307 GCC data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 308 GCC data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 309 GCC data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 310 GCC data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 311 GCC data center accelerator market, by end-use, 2024 - 2032 (USD Million)

- TABLE 312 South Africa data center accelerator market, 2018 - 2023 (USD Million)

- TABLE 313 South Africa data center accelerator market, 2024 - 2032 (USD Million)

- TABLE 314 South Africa data center accelerator market, by processor type, 2018 - 2023 (USD Million)

- TABLE 315 South Africa data center accelerator market, by processor type, 2024 - 2032 (USD Million)

- TABLE 316 South Africa data center accelerator market, by type, 2018 - 2023 (USD Million)

- TABLE 317 South Africa data center accelerator market, by type, 2024 - 2032 (USD Million)

- TABLE 318 South Africa data center accelerator market, by application, 2018 - 2023 (USD Million)

- TABLE 319 South Africa data center accelerator market, by application, 2024 - 2032 (USD Million)

- TABLE 320 South Africa data center accelerator market, by end-use, 2018 - 2023 (USD Million)

- TABLE 321 South Africa data center accelerator market, by end-use, 2024 - 2032 (USD Million)

Charts & Figures

- FIG 1 GMI's report coverage in the global data center accelerator market

- FIG 2 Industry segmentation

- FIG 3 Forecast calculation

- FIG 4 Profile break-up of primary respondents

- FIG 5 Data center accelerator market 360 degree synopsis, 2018 - 2032

- FIG 6 Industry ecosystem analysis

- FIG 7 Profit margin analysis

- FIG 8 Growth potential analysis

- FIG 9 Porter's analysis

- FIG 10 PESTEL analysis

- FIG 11 Competitive analysis of major market players, 2023

- FIG 12 Competitive positioning matrix

- FIG 13 Strategic outlook matrix

- FIG 14 Data center accelerator market, by processor type, 2023 & 2032

- FIG 15 Data center accelerator market, by type, 2023 & 2032

- FIG 16 Data center accelerator market, by application, 2023 & 2032

- FIG 17 Data center accelerator market, by end-use, 2023 & 2032

- FIG 18 SWOT Analysis, Achronix Semiconductor

- FIG 19 SWOT Analysis, Advanced Micro Devices, Inc

- FIG 20 SWOT Analysis, Advantech Co., Ltd.

- FIG 21 SWOT Analysis, Dell Inc.

- FIG 22 SWOT Analysis, GYRFALCON TECHNOLOGY INC.

- FIG 23 SWOT Analysis, Huawei Technologies Co. Ltd.

- FIG 24 SWOT Analysis, IBM Corporation

- FIG 25 SWOT Analysis, Intel Corporation

- FIG 26 SWOT Analysis, Lattice Semiconductor

- FIG 27 SWOT Analysis, Lenovo Ltd.

- FIG 28 SWOT Analysis, Marvell Technology Inc.

- FIG 29 SWOT Analysis, Microchip Technology Inc.

- FIG 30 SWOT Analysis, Micron Technology, Inc.

- FIG 31 SWOT Analysis, NEC Corporation

- FIG 32 SWOT Analysis, NVIDIA Corporation

- FIG 33 SWOT Analysis, Qualcomm Incorporated

- FIG 34 SWOT Analysis, Skyworks Solutions Inc.

- FIG 35 SWOT Analysis, Synopsys Inc

- FIG 36 SWOT Analysis, Western Digital Corporation

- FIG 37 SWOT Analysis, Xilinx Inc.

The global data center accelerator market is anticipated to grow at a CAGR of 25% between 2024-2032, driven by a surge in demand for efficient data processing, along with incorporation of artificial intelligence (AI) and machine learning (ML) applications.

According to According to a recent NielsenIQ study, 78% of US consumers prioritize a sustainable lifestyle. Accelerators designed with a focus on energy-efficient processing are gaining traction as organizations seek to reduce their carbon footprint and operational costs. This trend aligns with the growing awareness of the environmental impact of data centers, prompting businesses to invest in accelerators that offer high performance while minimizing energy consumption. Moreover, the escalating demand for high-performance computing (HPC) applications across industries such as finance, healthcare, and research has also contributed to market growth.

The overall data center accelerator industry is classified based on processor type, type, application, end-use, and region.

The GPU segment is set to grow significantly during the study period, driven by the increasing adoption of GPUs in data centers to accelerate a diverse range of applications. Graphics Processing Units (GPUs) have evolved beyond their traditional role in rendering graphics to become indispensable for parallel processing tasks. Moreover, the parallel architecture of GPUs makes them well-suited for handling the parallelized workloads of modern applications, including AI and ML algorithms.

The cloud accelerator segment is poised to expand significantly through 2032, as cloud adoption continues to be a strategic imperative for organizations seeking digital transformation. Cloud accelerators are vital in enhancing the performance and efficiency of cloud-based applications, enabling businesses to harness the benefits of scalability and flexibility.

Asia Pacific data center accelerator market is expected to grow rapidly through 2032, owing to a burgeoning technological adoption, rapid urbanization, and a growing digital economy. Countries like China, India, and Japan are adding to industry revenue, with increasing investments in data center infrastructure and the adoption of advanced technologies. Moreover, the demand for data-intensive applications and services is propelling the need for data center accelerators in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Data center accelerator market 360 degree synopsis, 2018 - 2032

- 2.2 Business trends

- 2.2.1 Total Addressable Market (TAM), 2024 - 2032

- 2.3 Regional trends

- 2.4 Processor type trends

- 2.5 Type trends

- 2.6 Application trends

- 2.7 End-use trends

Chapter 3 Data Center Accelerator Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Impact on data center infrastructure

- 3.4.1 Changing server architecture and workloads

- 3.4.2 Need for specialized cooling and power solutions

- 3.4.3 Impact on data center operations and management

- 3.5 Key news and initiatives

- 3.5.1 Partnership/Collaboration

- 3.5.2 Merger/Acquisition

- 3.5.3 Investment

- 3.5.4 Product launch & innovation

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing usage of online services globally

- 3.7.1.2 Increasing demand for advanced technologies worldwide across various industries

- 3.7.1.3 Growing demand for high-performance computing across North America and europe

- 3.7.1.4 Increasing establishment of hyperscale data centers in Europe and asia pacific

- 3.7.1.5 Wide adoption of cloud computing and IoT in Asia Pacific

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Requirement of specialized infrastructure

- 3.7.2.2 Rising costs of raw materials and skilled labor

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

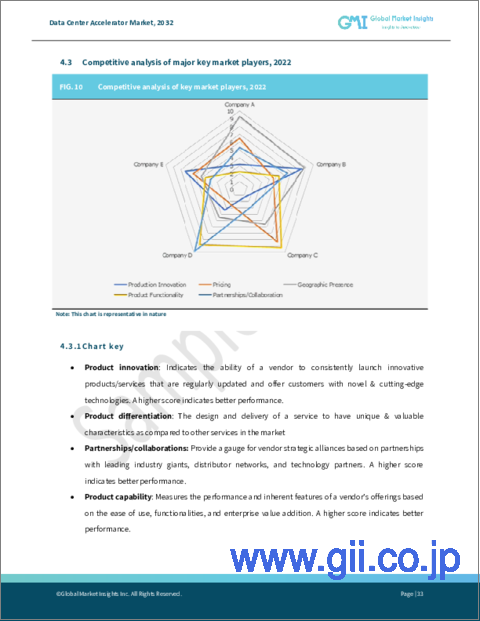

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share, 2023

- 4.3 Competitive analysis of major market players, 2023

- 4.3.1 Advanced Micro Devices, Inc.

- 4.3.2 Dell Inc.

- 4.3.3 Intel Corporation

- 4.3.4 Marvell Technology Inc.

- 4.3.5 NVIDIA Corporation

- 4.3.6 Qualcomm Incorporated

- 4.3.7 Synopsys Inc.

- 4.4 Competitive positioning matrix, 2023

- 4.5 Strategic outlook matrix, 2023

Chapter 5 Data Center Accelerator Market Estimates & Forecast, By Processor type (Revenue)

- 5.1 Key trends, by processor type

- 5.2 Central Processing Unit (CPU)

- 5.3 Graphical Processing Unit (GPU)

- 5.4 Field Programmable Gate Array (FPGA)

- 5.5 Application Specific Integrated Circuit (ASIC)

Chapter 6 Data Center Accelerator Market Estimates & Forecast, By Type (Revenue)

- 6.1 Key trends, by type

- 6.2 HPC accelerator

- 6.3 Cloud accelerator

Chapter 7 Data Center Accelerator Market Estimates & Forecast, By Application (Revenue)

- 7.1 Key trends, by application

- 7.2 Deep learning training

- 7.3 Public cloud interface

- 7.4 Enterprise interface

Chapter 8 Data Center Accelerator Market Estimates & Forecast, By End-use (Revenue)

- 8.1 Key trends, by end-use

- 8.2 IT & Telecom

- 8.3 Healthcare

- 8.4 BFSI

- 8.5 Government

- 8.6 Energy

- 8.7 Manufacturing

- 8.8 Others

Chapter 9 Data Center Accelerator Market Estimates & Forecast, By Region (Revenue)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Benelux

- 9.3.8 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Chile

- 9.6 MEA

- 9.6.1 GCC

- 9.6.2 South Africa

Chapter 10 Company Profiles

- 10.1 Achronix Semiconductor

- 10.2 Advanced Micro Devices, Inc

- 10.3 Advantech Co., Ltd.

- 10.4 Dell Inc.

- 10.5 GYRFALCON TECHNOLOGY INC.

- 10.6 Huawei Technologies Co. Ltd.

- 10.7 IBM Corporation

- 10.8 Intel Corporation

- 10.9 Lattice Semiconductor

- 10.10 Lenovo Ltd.

- 10.11 Marvell Technology Inc.

- 10.12 Microchip Technology Inc.

- 10.13 Micron Technology, Inc.

- 10.14 NEC Corporation

- 10.15 NVIDIA Corporation

- 10.16 Qualcomm Incorporated

- 10.17 Skyworks Solutions Inc.

- 10.18 Synopsys Inc

- 10.19 Western Digital Corporation

- 10.20 Xilinx Inc