|

|

市場調査レポート

商品コード

1753878

良性乳腺症と早期乳がん市場- 世界と地域別分析:分析と予測、2025年~2035年Benign Breast Disease and Early Breast Cancer Market - A Global and Regional Analysis: Analysis and Forecast, 2025-2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 良性乳腺症と早期乳がん市場- 世界と地域別分析:分析と予測、2025年~2035年 |

|

出版日: 2025年06月23日

発行: BIS Research

ページ情報: 英文 100 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

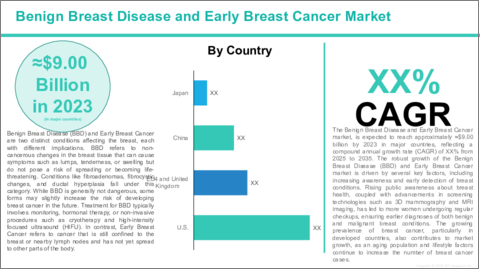

良性乳腺症(BBD)と早期乳がんは、乳房に影響を及ぼす2つの異なる病態であり、それぞれに特徴や治療アプローチがあります。

良性乳腺症は、線維嚢胞性変化、線維腺腫、乳管過形成などの非がん性疾患を指し、特に生殖年齢の女性によく見られます。

これらの疾患は乳房のしこりや圧痛として現れることが多く、一般的に生命を脅かすものではありませんが、後に乳がんを発症するリスクをわずかに高めるものもあります。良性乳腺症の治療は一般的に非侵襲的で、凍結療法や高密度焦点式超音波療法(HIFU)などの方法で症状の管理や良性腫瘍の除去に重点を置きます。

一方、早期乳がんとは、体の他の部分に転移がなく乳房組織に限局したがんを指し、多くの場合ステージ0、1、2で発見されます。早期乳がんは予後が著しく良好であり、手術、放射線、HER2阻害剤やCDK4/6阻害剤などの標的治療などの治療により、再発のリスクを大幅に減らすことができます。どちらの疾患も、早期介入が効果的な治療と患者の転帰改善の鍵となるため、定期的な検診による早期発見の重要性を強調しています。

良性乳腺症および早期乳がん市場の主な促進要因の1つは、乳房の健康に対する世界の意識の高まりと早期発見の重視の高まりです。乳がん啓発月間などの啓発キャンペーンが世界的に浸透するにつれて、より多くの女性が定期的な検診を優先するようになり、良性・悪性両方の乳房疾患を早期に発見するのに役立っています。早期発見は、早期乳がんの予後を改善するだけでなく、より積極的な治療の必要性を減らし、より良い転帰と副作用の減少につながります。早期発見の利点に対する意識の高まりは、3Dマンモグラフィ、MRI、遺伝子検査などのスクリーニング技術の進歩と相まって、革新的な診断ツールや治療に対する需要を煽っています。このような早期診断と予防医療への注目の高まりが、良性乳腺疾患と早期乳がん分野の大幅な市場成長を促しています。

良性乳房疾患および早期乳がん市場の成長にもかかわらず、いくつかの課題がその可能性を完全に阻害し続けています。良性乳房疾患および早期乳がん市場における主な課題の1つは、高度な治療と診断技術のコストが高いことです。

遺伝子検査、3Dマンモグラフィ、MRI画像診断などの革新的な診断ツールや、標的治療、免疫療法などの先進的な治療法の開発・導入には、法外な費用がかかります。このため、特に新興市場の患者は、こうした救命技術や治療を利用することが難しくなっています。さらに、高額な費用はヘルスケアシステムに負担をかけ、特に十分なサービスを受けていない人々にとっては、医療への不平等なアクセスにつながる可能性があります。コストの壁は、早期発見率や治療成績を向上させる可能性のあるこれらの先進的ソリューションの普及を制限しています。その結果、市場の潜在力を最大限に引き出し、高度な治療と診断を必要とするすべての患者が利用できるようにするためには、コスト関連の課題に対処することが極めて重要です。

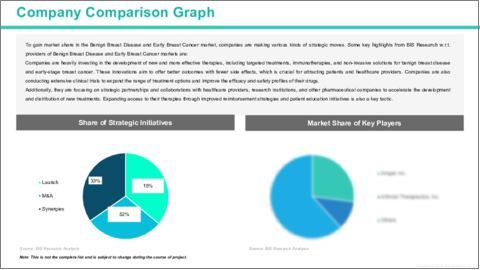

世界の良性乳房疾患と早期乳がん市場は競争が激しく、複数の主要企業が技術革新と市場成長を牽引しています。Novartis AG、Pfizer Inc.、Eli Lilly and Companyなどの主要企業は、良性乳腺疾患と早期乳がんの両方に対する画期的な治療法や治療法の開発で最先端を走っています。

Novartis AGは、HR陽性、HER2陰性の早期乳がんをターゲットとするKisqaliなどのCDK4/6阻害薬や、より個別化されたがん治療のためのKymriahなどのHER2標的治療薬のポートフォリオで大きな進歩を遂げています。Pfizer Inc.は、HR陽性、HER2陰性の早期乳がんに使用されるCDK4/6阻害剤であるイブランスと、転移性乳がんのHER2標的治療薬であるツキサで市場をリードしており、より早期のステージへの拡大が進められています。Eli Lilly and Companyは、HR陽性、HER2陰性の早期乳がんにおいてCDK4/6経路を標的とするVerzenioやIbranceなどの治療や、新たな治療オプションの継続的な調査により、その地位を強化しています。

これらの企業は、標的治療、遺伝子検査、個別化医療の進歩を活用し、乳がんや良性乳房疾患に対してより効果的で侵襲の少ない治療を提供しています。革新的研究と最先端技術への注力は、市場の展望を形成し続け、新たな治療法の開拓と患者の転帰の改善を推進しています。

良性乳腺疾患と早期乳がん市場のセグメンテーション

セグメンテーション1:地域別

- 北米

- 欧州

- アジア太平洋

世界の良性乳房疾患および早期乳がん市場は、診断、治療、患者ケアの状況を再構築するいくつかの重要な新興動向に見舞われています。良性乳房疾患および早期乳がん市場における最も重要な動向の1つは、個別化医療および精密医療の採用が増加していることです。この動向は、ゲノム・プロファイリングとバイオマーカー検査の進歩によってもたらされ、医療提供者は患者と腫瘍の両方の遺伝子構成に基づいて治療を調整することができます。例えば、早期乳がんの治療に標的療法や免疫療法が用いられるようになってきており、従来の化学療法に比べて副作用が少なく、より効果的な治療が提供されています。個別化治療は良性乳腺症にも適用されており、ホルモン療法や、凍結療法や高密度焦点式超音波(HIFU)などの非侵襲的処置が、個々の状態に基づいてカスタマイズされ、治療成績の向上や不必要な介入を最小限に抑えています。より個別化された治療へのシフトは、治療効果を大幅に改善し、患者の満足度を高め、ヘルスケアシステム全体の負担を軽減しています。

当レポートでは、世界の良性乳腺症と早期乳がん市場について調査し、市場の概要とともに、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 世界の良性乳腺症と早期乳がん市場:業界展望

- イントロダクション

- 市場動向

- 規制の枠組み

- 疫学分析

- 臨床試験分析

- 市場力学

- 影響分析

- 市場の促進要因

- 市場の課題

- 市場の機会

第2章 世界の良性乳腺症と早期乳がん市場(地域別)、2023年~2035年

- 北米

- 欧州

- アジア太平洋

第3章 世界の良性乳腺症と早期乳がん市場:競合情勢と企業プロファイル

- 主要戦略と開発

- 合併と買収

- 相乗効果のある活動

- 事業拡大と資金調達

- 製品の発売と承認

- その他の活動

- 企業プロファイル

- F. Hoffmann-La Roche AG

- Novartis AG

- AbbVie Inc. (Genmab A/S)

- Eli Lilly and Company

- AstraZeneca

- Pfizer Inc.

第4章 調査手法

List of Figures

- Figure: Global Benign Breast Disease and Early Breast Cancer Market (by Region), $Billion, 2024 and 2035

- Figure: Global Benign Breast Disease and Early Breast Cancer Market Key Trends, Analysis

List of Tables

- Table: Global Benign Breast Disease and Early Breast Cancer Market Dynamics, Impact Analysis

- Table: Global Benign Breast Disease and Early Breast Cancer Market (by Region), $Billion, 2024-2035

Global Benign Breast Disease and Early Breast Cancer Market, Analysis and Forecast: 2025-2035

Benign Breast Disease (BBD) and Early Breast Cancer are two distinct conditions that affect the breast, each with its own set of characteristics and treatment approaches. Benign Breast Disease refers to non-cancerous conditions such as fibrocystic changes, fibroadenomas, and ductal hyperplasia, which are common, especially in women of reproductive age.

These conditions often present as lumps or tenderness in the breasts and, while generally not life-threatening, some may slightly increase the risk of developing breast cancer later. Treatment for Benign Breast Disease is typically non-invasive, focusing on managing symptoms or removing benign growths through methods such as cryotherapy or high-intensity focused ultrasound (HIFU).

In contrast, Early Breast Cancer refers to cancer that is confined to the breast tissue without spread to other parts of the body, often detected in Stage 0, 1, or 2. Early breast cancer has a significantly better prognosis, and with treatments such as surgery, radiation, and targeted therapies such as HER2 inhibitors and CDK4/6 inhibitors, the risk of recurrence can be greatly reduced. Both conditions highlight the critical importance of early detection through regular screenings, as early intervention is key to effective treatment and improved patient outcomes.

One of the key drivers of the Benign Breast Disease and Early Breast Cancer market is the increasing global awareness of breast health and the growing emphasis on early detection. As public awareness campaigns, such as Breast Cancer Awareness Month, gain traction worldwide, more women are prioritizing regular screenings, which helps identify both benign and malignant breast conditions at earlier stages. Early detection not only improves the prognosis for early breast cancer but also reduces the need for more aggressive treatments, leading to better outcomes and fewer side effects. The rising awareness of the benefits of early detection, coupled with advancements in screening technologies such as 3D mammography, MRI, and genetic testing, is fuelling the demand for innovative diagnostic tools and treatments. This growing focus on early diagnosis and preventive care is driving significant market growth in the Benign Breast Disease and Early Breast Cancer sectors.

Despite the growth of the Benign Breast Disease and Early Breast Cancer market, several challenges continue to impede its full potential. One of the primary challenges in the Benign Breast Disease and Early Breast Cancer market is the high cost of advanced treatments and diagnostic technologies.

The development and deployment of innovative diagnostic tools, such as genetic testing, 3D mammography, and MRI imaging, as well as advanced therapies such as targeted treatments and immunotherapies, can be prohibitively expensive. This makes it difficult for patients, especially in emerging markets, to access these life-saving technologies and treatments. Additionally, the high cost can strain healthcare systems and lead to unequal access to care, particularly for underserved populations. The cost barrier limits the widespread adoption of these advanced solutions, which could otherwise improve early detection rates and treatment outcomes. As a result, addressing cost-related challenges is crucial for unlocking the full potential of the market and ensuring that advanced treatments and diagnostics are accessible to all patients in need.

The global Benign Breast Disease and Early Breast Cancer market is highly competitive, with several key players driving innovation and market growth. Leading companies such as Novartis AG, Pfizer Inc., and Eli Lilly and Company are at the forefront of developing groundbreaking treatments and therapies for both benign breast conditions and early-stage breast cancer.

Novartis AG has made significant strides with its portfolio of CDK4/6 inhibitors such as Kisqali, which targets HR-positive, HER2-negative early breast cancer, and HER2-targeted therapies such as Kymriah for more personalized cancer treatments. Pfizer Inc. leads the market with Ibrance, a CDK4/6 inhibitor used for HR-positive, HER2-negative early breast cancer, as well as Tukysa, a HER2-targeted therapy for metastatic breast cancer, which is being expanded for earlier stages. Eli Lilly and Company has strengthened its position with treatments such as Verzenio and Ibrance, both of which target the CDK4/6 pathway in HR-positive, HER2-negative early breast cancer, as well as ongoing research into new therapeutic options.

These companies are leveraging advancements in targeted therapies, genetic testing, and personalized medicine to provide more effective, less invasive treatments for breast cancer and benign breast conditions. Their focus on innovative research and cutting-edge technologies continues to shape the landscape of the market, driving both the development of new therapies and the improvement of patient outcomes.

Benign Breast Disease and Early Breast Cancer Market Segmentation:

Segmentation 1: by Region

- North America

- Europe

- Asia-Pacific

The global Benign Breast Disease and Early Breast Cancer market is experiencing several key emerging trends that are reshaping the landscape of diagnosis, treatment, and patient care. One of the most significant trends in the Benign Breast Disease and Early Breast Cancer market is the increasing adoption of personalized and precision medicine. This trend is driven by advancements in genomic profiling and biomarker testing, which allow healthcare providers to tailor treatments based on the genetic makeup of both the patient and the tumour. For example, targeted therapies and immunotherapies are being increasingly used to treat early breast cancer, offering more effective treatment with fewer side effects compared to traditional chemotherapy. Personalized treatments are also being applied in Benign Breast Disease, where hormonal therapies and non-invasive procedures such as cryotherapy and high-intensity focused ultrasound (HIFU) are customized based on individual conditions, improving outcomes and minimizing unnecessary interventions. This shift towards more individualized care is significantly improving the effectiveness of treatments, enhancing patient satisfaction, and reducing the overall burden on the healthcare system.

Table of Contents

Executive Summary

Scope and Definition

Market/Product Definition

Inclusion and Exclusion

Key Questions Answered

Analysis and Forecast Note

1. Global Benign Breast Disease and Early Breast Cancer Market: Industry Outlook

- 1.1 Introduction

- 1.2 Market Trends

- 1.3 Regulatory Framework

- 1.4 Epidemiology Analysis

- 1.5 Clinical Trial Analysis

- 1.6 Market Dynamics

- 1.6.1 Impact Analysis

- 1.6.2 Market Drivers

- 1.6.3 Market Challenges

- 1.6.4 Market Opportunities

2. Global Benign Breast Disease and Early Breast Cancer Market (Region), ($Billion), 2023-2035

- 2.1 North America

- 2.1.1 Key Findings

- 2.1.2 Market Dynamics

- 2.1.3 Market Sizing and Forecast

- 2.1.3.1 North America Benign Breast Disease and Early Breast Cancer Market, by Country

- 2.1.3.1.1 U.S.

- 2.1.3.1 North America Benign Breast Disease and Early Breast Cancer Market, by Country

- 2.2 Europe

- 2.2.1 Key Findings

- 2.2.2 Market Dynamics

- 2.2.3 Market Sizing and Forecast

- 2.2.3.1 Europe Benign Breast Disease and Early Breast Cancer Market, by Country

- 2.2.3.1.1 Germany

- 2.2.3.1.2 U.K.

- 2.2.3.1.3 France

- 2.2.3.1.4 Italy

- 2.2.3.1 Europe Benign Breast Disease and Early Breast Cancer Market, by Country

- 2.3 Asia Pacific

- 2.3.1 Key Findings

- 2.3.2 Market Dynamics

- 2.3.3 Market Sizing and Forecast

- 2.3.3.1 Asia Pacific Benign Breast Disease and Early Breast Cancer Market, by Country

- 2.3.3.1.1 China

- 2.3.3.1.2 Japan

- 2.3.3.1 Asia Pacific Benign Breast Disease and Early Breast Cancer Market, by Country

3. Global Benign Breast Disease and Early Breast Cancer Market: Competitive Landscape and Company Profiles

- 3.1 Key Strategies and Development

- 3.1.1 Mergers and Acquisitions

- 3.1.2 Synergistic Activities

- 3.1.3 Business Expansions and Funding

- 3.1.4 Product Launches and Approvals

- 3.1.5 Other Activities

- 3.2 Company Profiles

- 3.2.1 F. Hoffmann-La Roche AG

- 3.2.1.1 Overview

- 3.2.1.2 Top Products / Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End-Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.1 Novartis AG

- 3.2.1.1 Overview

- 3.2.1.2 Top Products / Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End-Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.2 AbbVie Inc. (Genmab A/S)

- 3.2.2.1 Overview

- 3.2.2.2 Top Products / Product Portfolio

- 3.2.2.3 Top Competitors

- 3.2.2.4 Target Customers/End-Users

- 3.2.2.5 Key Personnel

- 3.2.2.6 Analyst View

- 3.2.3 Eli Lilly and Company

- 3.2.3.1 Overview

- 3.2.3.2 Top Products / Product Portfolio

- 3.2.3.3 Top Competitors

- 3.2.3.4 Target Customers/End-Users

- 3.2.3.5 Key Personnel

- 3.2.3.6 Analyst View

- 3.2.4 AstraZeneca

- 3.2.4.1 Overview

- 3.2.4.2 Top Products / Product Portfolio

- 3.2.4.3 Top Competitors

- 3.2.4.4 Target Customers/End-Users

- 3.2.4.5 Key Personnel

- 3.2.4.6 Analyst View

- 3.2.5 Pfizer Inc.

- 3.2.5.1 Overview

- 3.2.5.2 Top Products / Product Portfolio

- 3.2.5.3 Top Competitors

- 3.2.5.4 Target Customers/End-Users

- 3.2.5.5 Key Personnel

- 3.2.5.6 Analyst View

- 3.2.1 F. Hoffmann-La Roche AG