|

|

市場調査レポート

商品コード

1752087

アジア太平洋のデータセンターコロケーション市場:用途別、ビジネスモデル別、国別 - 分析と予測(2025年~2034年)Asia-Pacific Data Center Colocation Market: Focus on Application, Product, and Country - Analysis and Forecast, 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| アジア太平洋のデータセンターコロケーション市場:用途別、ビジネスモデル別、国別 - 分析と予測(2025年~2034年) |

|

出版日: 2025年06月19日

発行: BIS Research

ページ情報: 英文 59 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のデータセンターコロケーションの市場規模は、2024年に202億3,000万米ドルとなりました。

同市場は、2025年から2034年にかけて12.16%のCAGRで拡大し、2034年には708億8,000万米ドルに達すると予測されています。費用対効果が高く、拡張性があり、安全なITインフラに対する需要の高まりが、アジア太平洋におけるデータセンターコロケーション市場の急拡大を後押ししています。クラウド・コンピューティング、ハイブリッドITアーキテクチャ、デジタルトランスフォーメーション・プロジェクトを採用する企業が増える中、コロケーション・サービスは、高性能で耐障害性に優れ、エネルギー効率の高い運用を保証しながら、インフラ管理の負荷を軽減するために不可欠となっています。分散型で低遅延のデータセンター・ネットワークに対する需要は、この地域全体のエッジ・コンピューティングの成長によって牽引されています。さらに、コロケーション・プロバイダーは、持続可能性が最優先事項となった結果、環境に配慮したアーキテクチャ、冷却システムの改善、再生可能エネルギー源への投資を進めています。コロケーションは、これらの要因に加え、厳格なデータローカライゼーション法、アップタイムと運用効率に対する企業の要求の高まりにより、アジア太平洋の変化するデジタルインフラの重要な構成要素として位置づけられています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025年~2034年 |

| 2025年の評価 | 252億3,000万米ドル |

| 2034年の予測 | 708億8,000万米ドル |

| CAGR | 12.16% |

市場イントロダクション

アジア太平洋のデータセンターコロケーション市場は、企業やサービスプロバイダーがコスト削減と業務の効率化を追求する中で急成長しています。コロケーション施設は、自社でデータホールを建設・維持する心配がなく、広帯域幅の接続性、信頼性の高いセキュリティ対策、冗長電源など、専門家が管理する環境を利用できます。エンタープライズグレードのインフラを必要としながらも、個人プロジェクトに投資する資金がない中小企業(SMB)は、この動向の影響を最も受けています。

eコマース、オンラインギャンブル、ストリーミングメディア、フィンテックなどのデジタルサービスの急速な台頭により、地理的に分散されたホスティングサイトへの需要が高まっています。その結果、ジャカルタ、クアラルンプール、ムンバイ、ホーチミンのような新興市場とともに、シンガポールや東京のような確立された中心地も開発されつつあります。現地のオペレーターも国際的なハイパースケーラーも、ファイバーネットワークの改善、不動産コストの削減、有利な政府補助金により、これらの二次市場が魅力的な選択肢であると感じています。

コロケーション事業者は、従来のワークロードのサポートに加え、マネージドセキュリティ、ディザスタリカバリ、クラウドプロバイダーとのクロスコネクト接続といった付加価値サービスを急速に取り入れています。将来的には、モジュール式の「"build-as-you-grow"」設計やAIを活用した監視ツールによって、運用効率や拡張性が向上すると予想されます。電力供給やコンプライアンスにまだ問題があるとしても、継続的なインフラ投資と戦略的提携により、アジア太平洋のコロケーション市場は今後5年間で長期的な拡大が見込まれます。

市場セグメンテーション

セグメンテーション1:用途別

- ITおよび電気通信

- 銀行・金融サービス・保険(BFSI)

- 政府・公共部門

- ヘルスケア

- 製造業

- 小売業

- その他

セグメンテーション2:ビジネスモデル別

- 小売

- 卸売

セグメント3:地域別

- アジア太平洋:中国、日本、オーストラリア、インド、韓国、その他

アジア太平洋のデータセンターコロケーション市場動向と促進要因・課題

動向

- ハイパースケーラーや企業が従来のハブを超えて拡大する中、Tier 2/3市場への分散化。

- 高密度コンピュートとAIに最適化された施設に対する需要の高まり別AI対応インフラの急増。

- 海底接続の強化により、地域間のデータフローとコロケーションの導入が促進。

- 再生可能エネルギーの統合、効率的な冷却、グリーン認証別持続可能な運用へのシフト。

促進要因

- クラウドの急速な普及とデジタルトランスフォーメーションにより、スケーラブルなコロケーション・ソリューションへの需要が高まっています。

- 活況を呈するeコマースと活気ある新興企業エコシステムが、地域密着型のデータセンター・ニーズを促進しています。

- 政府の支援とデータ主権政策が、地域のコロケーション投資を促進しています。

- AWS、Microsoft Azure、Google Cloudなど別ハイパースケーラへの大規模な投資が、新興のアジア太平洋地域に進出しています。

課題

- 新興国市場の用地が限られているため、開発者は成熟していない場所を探さざるを得ません。

- 電力とエネルギーの制約により、増加するデータセンターの負荷に対応するための送電網の整備に苦慮しています。

- アジア太平洋全域で規制やコンプライアンス要件が多様化しており、立地選定や承認が複雑化しています。

- 投資収益率に影響する資本コストと運用コスト(土地、人件費、資材、電力、冷却)の上昇。

製品/イノベーション戦略:アジア太平洋のデータセンターコロケーション市場は、多様な用途、ビジネスモデル、事業者のタイプに基づいてセグメント化されており、幅広い使用事例に関する洞察が得られます。主な用途には、IT・通信、銀行、金融サービス、保険(BFSI)、政府機関、ヘルスケア、製造、小売などが含まれ、それぞれが拡張性、安全性、信頼性の高いコロケーションサービスの恩恵を受けています。市場はまた、柔軟なソリューションを必要とする中小企業向けのリテール・コロケーションと、大量のデータを必要とする大企業向けのホールセール・コロケーションを区別しています。さらに、事業者は、広範なネットワークカバレッジと堅牢なインフラを提供する世界型と、特定の市場の需要に合わせた地域密着型のサービスを提供する地域型に分類されます。エネルギー効率の高い冷却、自動化、強化されたセキュリティ機能など、絶え間ない技術的進歩が市場の成長を促進すると予想され、業界各社は急速に進化するこの分野で提供サービスを拡大し、市場での地位を強化する大きな機会を得ることができます。

成長/マーケティング戦略:アジア太平洋のデータセンターコロケーション市場は急速なペースで成長しています。同市場は既存および新興の市場参入企業に大きな機会を提供しています。このセグメントで取り上げている戦略には、M&A、製品投入、提携・協力、事業拡大、投資などがあります。企業が市場での地位を維持・強化するために好む戦略には、主に製品開発が含まれます。

目次

エグゼクティブサマリー

第1章 市場

- コロケーションデータセンター市場の動向:現状と将来への影響評価

- データセンターの容量:現状と将来

- データセンターの電力消費シナリオ

- 空室率と吸収(地域別)

- 注目すべき主要市場

- その他の産業動向

- 研究開発レビュー

- 特許出願動向(企業別)

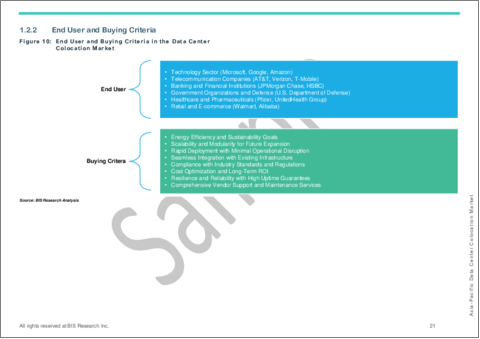

- エンドユーザーと購入基準

- 市場力学の概要

- 市場促進要因

- 市場抑制要因

- 市場機会

第2章 地域

- 地域のサマリー

- アジア太平洋

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 製品

- アジア太平洋(国別)

第3章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

第4章 調査手法

List of Figures

- Figure 1: Asia-Pacific Data Center Colocation Market, $Billion, 2024, 2027, and 2034

- Figure 2: Asia-Pacific Data Center Colocation Market (by Application), $Billion, 2023, 2027, and 2034

- Figure 3: Asia-Pacific Data Center Colocation Market (by Business Model), $Billion, 2023, 2027, and 2034

- Figure 4: Key Events

- Figure 5: Estimated Increase in Data Center Capacity, 2023 and 2030, in GW

- Figure 6: HPC Cluster Developments in the Data Center Market

- Figure 7: Share of Total 5G Mobile Connections (by Region) 2023 and 2030

- Figure 8: Increasing Rack Power Density Across Key Data Center Segments

- Figure 9: Comparison of Different Rack Densities in Data Centers

- Figure 10: Patent Analysis (by Company), January 2021-January 2025

- Figure 11: End User and Buying Criteria in the Data Center Colocation Market

- Figure 12: North America and Europe: Leading Hubs for Data Center Investments

- Figure 13: Estimated Data Creation, Zettabytes or Billions of Terabytes

- Figure 14: Estimated Increase in IoT Adoption in 2023

- Figure 15: Estimated Data Centers Energy Consumption (by Country), 2022

- Figure 16: China Data Center Colocation Market, $Billion, 2023-2034

- Figure 17: Japan Data Center Colocation Market, $Billion, 2023-2034

- Figure 18: Australia Data Center Colocation Market, $Billion, 2023-2034

- Figure 19: India Data Center Colocation Market, $Billion, 2023-2034

- Figure 20: South Korea Data Center Colocation Market, $Billion, 2023-2034

- Figure 21: Rest-of-Asia-Pacific Data Center Colocation Market, $Billion, 2023-2034

- Figure 22: Data Triangulation

- Figure 23: Top-Down and Bottom-Up Approach

- Figure 24: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Competitive Landscape Snapshot of Key Players

- Table 4: Trends Overview

- Table 5: Annual Vacancy Rates, Percentage, by Region, 2019-2023

- Table 6: Annual Net Absorption Estimation (by Region), MW, 2019-2023

- Table 7: Outlook of Data Center Colocation Market (by Location)

- Table 8: Recent Investments and Developments in Data Center Liquid Cooling Innovations

- Table 9: Data Center Colocation Market (by Region), $Billion, 2023-2034

- Table 10: Asia-Pacific Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 11: Asia-Pacific Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 12: China Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 13: China Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 14: Japan Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 15: Japan Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 16: Australia Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 17: Australia Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 18: India Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 19: India Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 20: South Korea Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 21: South Korea Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 22: Rest-of-Asia-Pacific Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 23: Rest-of-Asia-Pacific Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 24: Market Share,2023

This report can be delivered in 2 working days.

Introduction to Asia-Pacific Data Center Colocation Market

The Asia-Pacific data center colocation market was valued at $20.23 billion in 2024 and is projected to grow at a CAGR of 12.16% from 2025 to 2034, reaching $70.88 billion by 2034. The increasing demand for cost-effective, scalable, and secure IT infrastructure is driving the rapid expansion of the data centre colocation market in Asia-Pacific. As more companies embrace cloud computing, hybrid IT architectures, and digital transformation projects, colocation services have become crucial for offloading infrastructure management while guaranteeing high-performance, resilient, and energy-efficient operations. The demand for dispersed, low-latency data centre networks is being driven by the growth of edge computing throughout the region. Furthermore, colocation providers are investing in eco-friendly building architecture, improved cooling systems, and renewable energy sources as a result of sustainability becoming a top priority. Colocation is positioned as a key component of APAC's changing digital infrastructure landscape because to these factors, as well as strict data localisation laws and growing enterprise demands for uptime and operational effectiveness.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2034 |

| 2025 Evaluation | $25.23 Billion |

| 2034 Forecast | $70.88 Billion |

| CAGR | 12.16% |

Market Introduction

The market for data centre colocation in Asia Pacific has grown rapidly as businesses and service providers seek to reduce costs and streamline operations. Without having to worry about creating and maintaining their own data halls, colocation facilities give businesses the chance to take advantage of professionally managed settings with high-bandwidth connectivity, reliable security measures, and redundant power supply. Small and medium-sized enterprises (SMBs) who need enterprise-grade infrastructure but lack the funds to invest in private projects are most affected by this trend.

The demand for geographically diversified hosting sites has increased due to the rapid rise of digital services such as e-commerce, online gambling, streaming media, and fintech. As a result, established centres like Singapore and Tokyo are developing alongside new markets like Jakarta, Kuala Lumpur, Mumbai, and Ho Chi Minh City. Both local operators and international hyperscalers find these secondary markets to be appealing options due to their improved fibre networks, reduced real estate costs, and advantageous government subsidies.

Colocation operators are rapidly incorporating value-added services like managed security, disaster recovery, and cross-connect fabric connectivity to cloud providers in addition to supporting traditional workloads. In the future, it is anticipated that modular """"build-as-you-grow"""" designs and AI-driven monitoring tools would improve operational efficiency and scalability. Even if there are still issues with power availability and compliance, continued infrastructure expenditures and strategic alliances set up APAC's colocation market for long-term expansion over the following five years.

Market Segmentation

Segmentation 1: by Application

- IT and Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Healthcare

- Manufacturing

- Retail

- Others

Segmentation 2: by Business Model

- Retail

- Wholesale

Segmentation 3: by Region

- Asia-Pacific: China, Japan, Australia, India, South Korea, and Rest-of-Asia-Pacific

APAC Data Center Colocation Market Trends, Drivers and Challenges

Trends

- Decentralization to Tier 2/3 markets as hyperscalers and enterprises expand beyond traditional hubs.

- Surge in AI-ready infrastructure with growing demand for high-density compute and AI-optimized facilities.

- Enhanced submarine connectivity boosting inter-regional data flow and colocation adoption.

- Shift toward sustainable operations through renewable energy integration, efficient cooling, and green certifications.

Drivers

- Rapid cloud adoption and digital transformation increasing demand for scalable colocation solutions.

- Booming e-commerce and a vibrant startup ecosystem driving localized data center needs.

- Government support and data-sovereignty policies encouraging local colocation investments.

- Significant hyperscaler investments from AWS, Microsoft Azure, Google Cloud, and others expanding into emerging APAC regions.

Challenges

- Limited land availability in prime markets, forcing developers to seek less-mature locations.

- Power and energy constraints, with grids struggling to support increasing data center loads.

- Diverse regulatory and compliance requirements across APAC complicating site selection and approvals.

- Rising capital and operational costs (land, labor, materials, power, cooling) affecting return-on-investment.

How can this report add value to an organization?

Product/Innovation Strategy: The APAC data center colocation market is segmented based on diverse applications, business models, and operator types, providing insights into its broad range of use cases. Key applications include IT and telecom, banking, financial services, insurance (BFSI), government, healthcare, manufacturing, retail, and others, each benefiting from scalable, secure, and reliable colocation services. The market also distinguishes between retail colocation, which caters to smaller businesses requiring flexible solutions, and wholesale colocation, designed for large-scale enterprises with high-volume data needs. Additionally, operators are categorized as global, offering extensive network coverage and robust infrastructure, or regional, providing localized services tailored to specific market demands. Continuous technological advancements, such as energy-efficient cooling, automation, and enhanced security features, are expected to drive the market's growth, providing substantial opportunities for industry players to expand their offerings and strengthen their market position in this rapidly evolving sector.

Growth/Marketing Strategy: The APAC data center colocation market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include product development.

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Colocation Data Center Market Trends: Current and Future Impact Assessment

- 1.1.1 Data Center Capacities: Current and Future

- 1.1.1.1 Retrofitting and Brownfield Projects

- 1.1.1.2 Green Field Projects and New Installation

- 1.1.2 Data Center Power Consumption Scenario

- 1.1.3 Vacancy Rates and Absorption (by Region)

- 1.1.4 Key Markets to Focus on

- 1.1.5 Other Industrial Trends

- 1.1.5.1 HPC Cluster Developments

- 1.1.5.2 Blockchain Initiatives

- 1.1.5.3 Super Computing

- 1.1.5.4 5G and 6G Developments

- 1.1.5.5 Impact of Server/Rack Density

- 1.1.1 Data Center Capacities: Current and Future

- 1.2 Research and Development Review

- 1.2.1 Patent Filing Trend (by Company)

- 1.2.2 End User and Buying Criteria

- 1.3 Market Dynamics Overview

- 1.3.1 Market Drivers

- 1.3.1.1 Increasing Data Center Spending

- 1.3.1.2 Growing Integration of AI and Cloud Computing

- 1.3.1.3 Sustainability and Environmental Pressures

- 1.3.2 Market Restraints

- 1.3.2.1 Power and Energy Constraints

- 1.3.2.2 Data Security and Compliance Challenges

- 1.3.3 Market Opportunities

- 1.3.3.1 Growing Demand for Different Business Models

- 1.3.3.2 Growth in AI Workloads

- 1.3.1 Market Drivers

2 Regions

- 2.1 Regional Summary

- 2.2 Asia-Pacific

- 2.2.1 Regional Overview

- 2.2.2 Driving Factors for Market Growth

- 2.2.3 Factors Challenging the Market

- 2.2.4 Application

- 2.2.5 Product

- 2.2.6 Asia-Pacific (by Country)

- 2.2.6.1 China

- 2.2.6.1.1 Application

- 2.2.6.1.2 Product

- 2.2.6.2 Japan

- 2.2.6.2.1 Application

- 2.2.6.2.2 Product

- 2.2.6.3 Australia

- 2.2.6.3.1 Application

- 2.2.6.3.2 Product

- 2.2.6.4 India

- 2.2.6.4.1 Application

- 2.2.6.4.2 Product

- 2.2.6.5 South Korea

- 2.2.6.5.1 Application

- 2.2.6.5.2 Product

- 2.2.6.6 Rest-of-Asia-Pacific

- 2.2.6.6.1 Application

- 2.2.6.6.2 Product

- 2.2.6.1 China

3 Markets - Competitive Benchmarking and Company Profiles

- 3.1 Next Frontiers

- 3.2 Geographic Assessment

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast